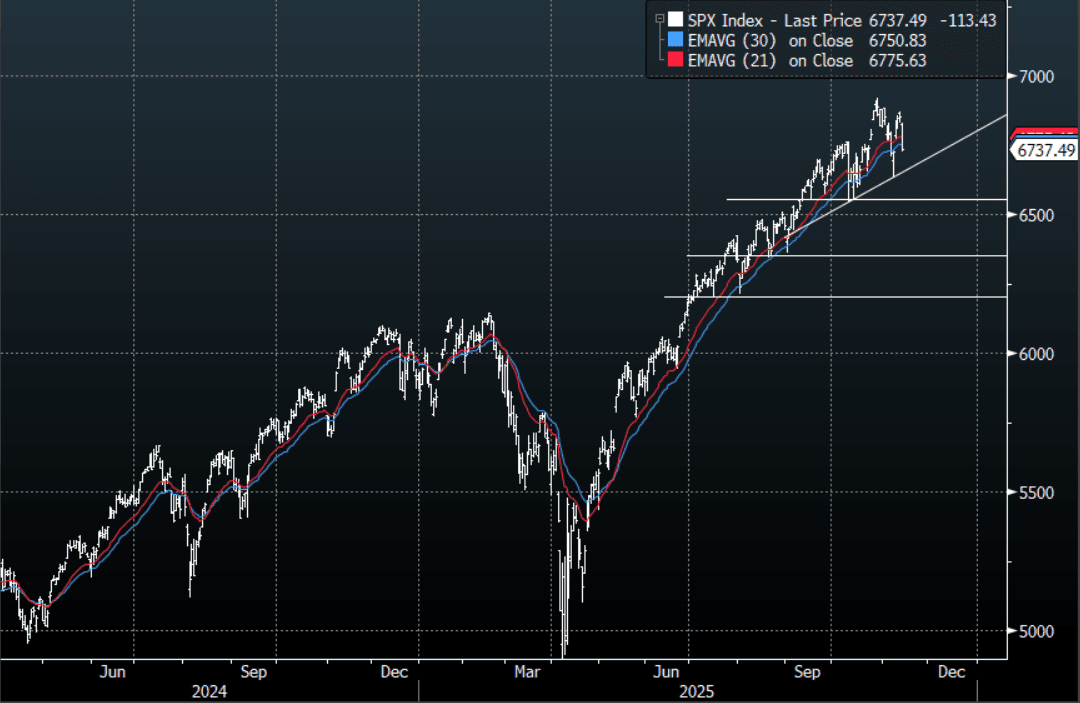

US STOCKS: S&P(ESZ5)-Fails Toward 6900 Collapses Lower, Putting In A Lower-High

The S&P(ESZ5) overnight range was 6746.00 - 6892.50, SPX closed -1.16%, Asia is currently trading around 6772.00. The S&P move higher again stalled overnight toward the 6900 area, then proceeded to turn lower and really accelerated through support during the N/Y session. The market has begun to contemplate what the US data when it eventually comes out might tell us, as a result the hopes of a December cut seem to be fading. The Crypto space again was a leading indicator for this move as a market positioned for a “year-end” rally is forced to pare back holdings. This morning stocks opened a little higher, E-minis(S&P) +0.20%, NQZ5 +0.20%. Technically the S&P has put in a lower high on the Daily chart and this could be signaling a deeper potential pullback.

- First support is around the 6725-6750 area, through here and the market will then be looking back toward the 6500-6625 support. On the Day would be looking to fade a bounce initially back toward 6820-6850 if we see it for a test back toward the overnight lows and beyond.

- Joseph Wang posted on X regarding the Feds changing views on cuts, "Strange so many Fed presidents are pushing back against a December cut. The bias in September was 3 cuts, and since then we have had limited official data with the shutdown itself a modest economic headwind."

Fig 1: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Steadies On US Reassurance & Silver Correction, At Overbought Levels

China’s comments on current trade issues with the US supported gold to another new record high at $4179.7/oz. It fell to $4090.67 soon after driven by a stronger US dollar and likely profit-taking as the metal is in overbought territory. Later on Wednesday it dipped again following comments from US trade representative Greer that staff-level talks with China were taking place increasing hopes of a solution. Gold ignored Fed Chair Powell’s indication of further easing due to the labour market as it has rate cuts already factored in.

- Easier liquidity in London for silver drove it down to $50.473 after a new high at $53.546. This also contributed to end gold’s Tuesday rally. Silver finished down 1.8% to $51.434 and is currently trading around $51.79. The white metal is still up over 10% in October and trend signals continue to be bullish with initial resistance at $52.00. Initial support is at $46.791, 20-day EMA.

- Silver is due to arrive in the UK in coming weeks as tight liquidity drove increased buying. The mismatch between physical and paper supply is expected to unwind with the risk that the small market size exaggerates a correction.

- Gold outperformed silver rising 0.8% to $4142.94 to be 7.4% higher this month. It is up on Wednesday to $4163.8. The bull cycle remains but the trend is overbought and a correction would allow this to start to unwind. Initial resistance is at $4179.7 followed by $4200.0 with initial support at $4006.5, 10 October low.

AUSSIE BONDS: Softer Futures, But Sep Highs Still Close, RBA's Hunter Speaks

Early Wednesday trade has Aussie bond futures down modestly, although we are still holding onto the bulk of recent gains seen this week. 3yr futures were last 96.50 (+2.5bps), while 10yr were at 95.73 (+2bps ). For 3yr recent Sep highs remain intact at 96.615, while for the 10yr the upside focus point is 95.78. Clearance of these levels would reinstate a bullish theme.

- Focus is on US-China tensions, which softened as Tuesday's session unfolded, with the USTR stating trade talks are on-going. Recall yesterday, risk off gripped markets as China announced shipping curbs/investigation.

- Whilst tomorrow the Sep Jobs data prints. We do hear from the RBA's Hunter later this morning, but the central bank is in data watch mode at this stage and still painting a cautious outlook (in terms of further cuts). A full 25bps cut is not priced in until Feb/Mar next year.

- ACGB cash yields sit around 2bps firmer across the benchmarks in the first part of Wednesday trade. The 3yr back to 3.48%, after finding support near 3.45%.

- The 3/10s curve is +77bps, slightly flatter. The AU-US 10yr spread has stabilized ahead of +20bps.

- Note today we also get the Westpac Leading index for Sep, while we also have a 2035 bond sale.

US TSYS: Yields Grind Lower as 10-Yr Eyes Key Resistance

TYZ5 traded up over night, reaching a high of 113-17+ before closing at 113-13+, a gain of +08. Futures have opened trading in the Asia trading day and is giving back some of those gains, down at 113-09+

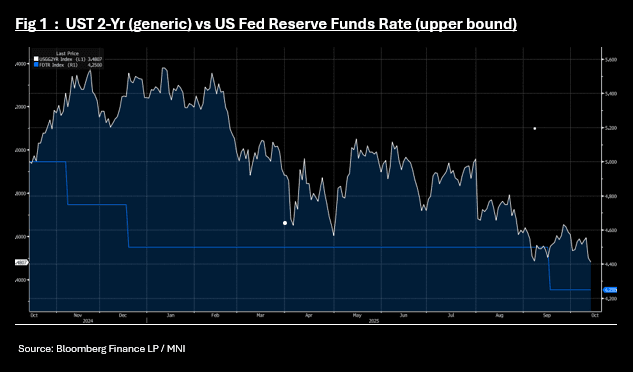

- The US 2-year yield had decent overnight rally down -2bps at 3.48% to reach 1-Yr lows. Looking at the MIPR function on BBG, the next rate cut is largely priced in and when looking for a catalyst for the 2-Yr to head lower, it is likely that it could come from the guidance post the October 30 meeting. See chart below of US 2-Yr vs Fed Funds Upper bound.

- The US 10-Yr closed at 4.034%, relatively unchanged. We observe that the trading range for the US 10-Yr of 4.20% - 4.00% has held over the last month and looking for catalysts that could break that range; we look ahead to the September CPI to be released October 2024.

- The US 30-Yr finished marginally higher in yield at 4.633% and appears to be stabilizing around these levels for now.

- We assess that back-to-back October / December cuts look to be supported by 7 of 12 2025 FOMC members, with all four regional presidents eyeing either one or no more cuts.

- The core of the Committee including all on the Board except for Barr will support cuts though as it stands, and we think the bar is fairly high for the holdouts to dissent.