US STOCKS: S&P(ESZ5)- Amazon & Apple Results Claw Back Some Of Yesterdays Losses

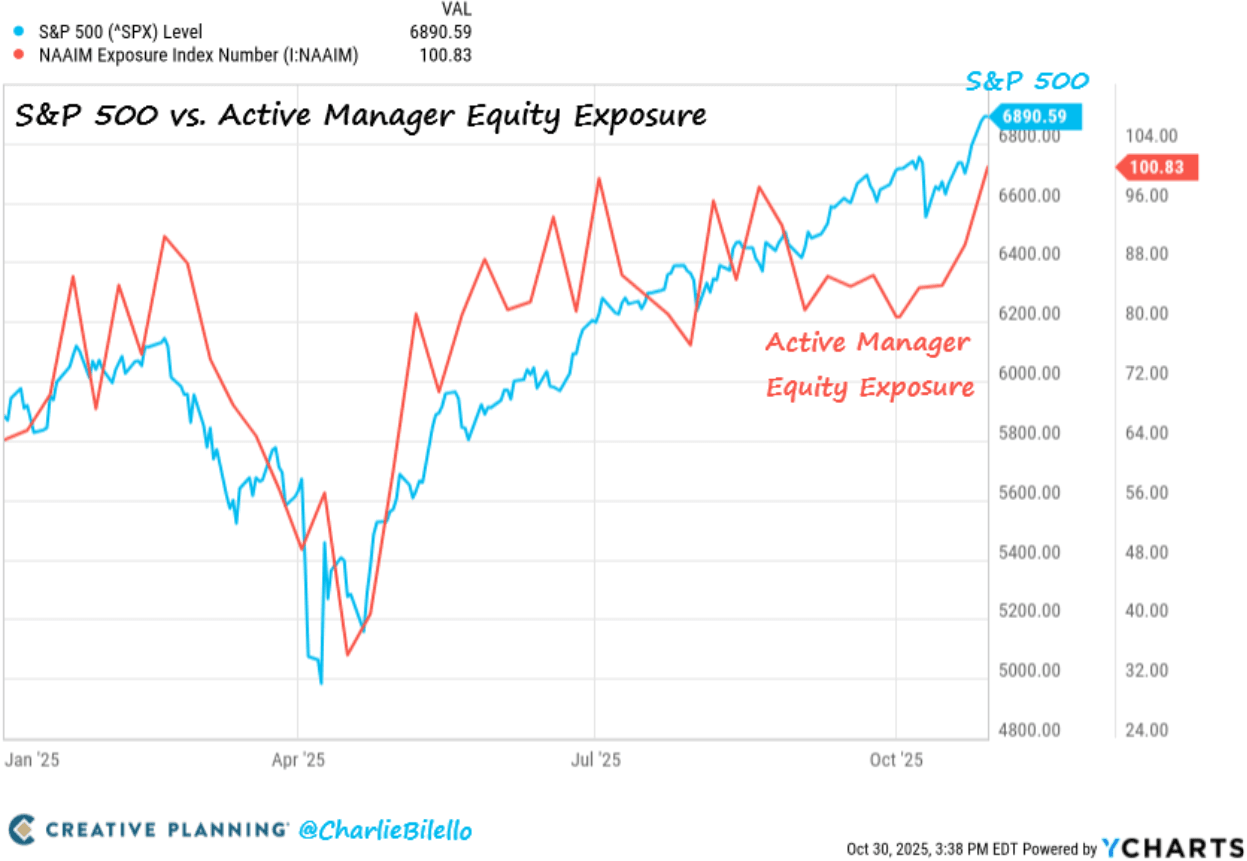

The S&P(ESZ5) overnight range was 6851.00 - 6932.75, SPX closed -0.99%, Asia is currently trading around 6899.00. The E-Mini’s bounced hard into the US close and have continued on to the Asian open on much better than expected results from both Amazon and Apple, E-minis(S&P) +0.65%, NQZ5 +1.15%. The stock market continues to defy all naysayers, and the results seen this morning will be used as justification for the bullish exuberance. The market is clearly in a powerful uptrend, though there are signs of some short-term exhaustion and most of the stubborn shorts have been forced back into the market as data shows active managers are back to 100% in the stock market.

- Charlie Bilello on X highlights how active managers have increased exposure since the lows seen in April: “Active managers reduced their equity exposure down to 35% back in April when the S&P 500 fell below 5,000. This week, their equity exposure jumped over 100% (leveraged long) with the S&P 500 at 6,900. This is their highest equity exposure since July 2024.” See Graph Below.

- Lance Roberts pointed out on X that JP Morgan sees history on the side of the bulls: "Yesterday was the fifth time that the Fed cut rates with the S&P 500 at all-time highs. All prior instances the S&P 500 was higher a year later with an average return of 20%. The worst one-year return was a 15% gain which occurred last year."

Fig 1: S&P 500 Vs Active Manager Exposure

Source: MNI - Market News/Creative Planning:@CharlieBilello

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: S&P - Grinds Back Toward Highs Overnight, Opens Lower In Asia

The S&P(ESZ5) overnight range was 6693.00 - 6743.50, SPX closed +0.41%, Asia is currently trading around 6716. The stock market continues to grind back towards its all-time highs brushing off concerns of an imminent US shutdown. This morning US futures have opened lower on our open as the shutdown looks to be executed, E-minis(S&P) -0.35%, NQZ5 -0.40%. The stock market continues to look way overdone but has brushed off every hurdle thrown at it including what was supposed to be its worst month of the year. The market is clearly still in an uptrend and dips continue to be supported for now, as we head into what is seasonally a positive period of the year. Discretionary Traders remain underweight and will be dragged back in to participate in the year end rally.

- Brian Sullivan on X: “It can be an uncomfortable thing because so many people and families are worried about their paychecks, but markets tend to go UP in government shutdowns. It's because shutdowns 1) don't involve all of the government and 2) tend to be short and 3) the economy actually tends to keep growing. Weird but true.”

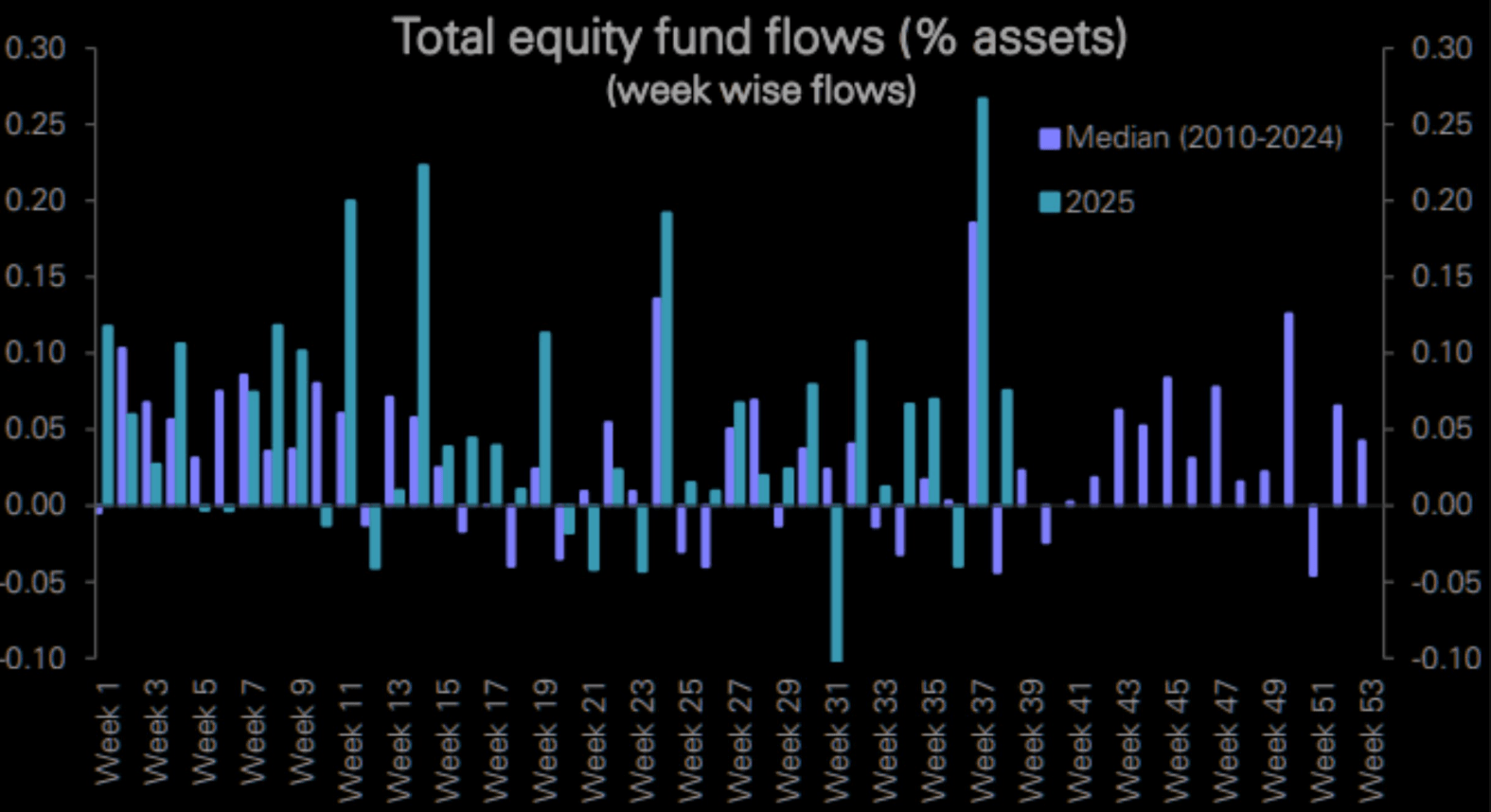

- Lance Roberts on X: “We are moving into the seasonally strong period of the year for equity fund flows.” See Graph Below.

- Bloomberg - “Sell Rest of World Replacing Sell US as Tariff Trade: The “sell America” theme that came to the fore when tariff turmoil was at its extremes in April has faded away. Now, the more likely investor response to President Donald Trump’s trade policies is to consider reducing non-US assets.”

- Daily Chartbook on X: "Our Sentiment Indicator, which measures US equity investor positioning, has rebounded to -0.6 this week from its low of -0.9 four weeks ago. None of the nine positioning measures in our indicator are in 'stretched' territory." - GS Morgan.

Fig 1: Weekly Equity Fund Flows

Source: MNI - Market News/@LanceRoberts

US TSYS: Cash Open

TYZ5 is trading 112-13+, down 0-02+ from its close.

- The US 2-year yield opens around 3.612%.

- The US 10-year yield opens around 4.158%, up 0.01 from its close.

- 10-Year yields remain subdued below 4.20% as the market prices in a US shutdown, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week and if not then the ADP starts to take on a lot more relevance.

- MNI FED: Vice Chair Jefferson: Softening Labor Market May Need Support. Fed Vice Chair Jefferson gave a speech early Tuesday morning that suggested a monetary policy outlook in line with that of most of the rest of the Fed leadership, including Chair Powell. As such we would guess he is among the 9 FOMC participants who anticipate making a further 2 25bp rate cuts by year-end to a median 3.6%, the same outlook that we think is shared by the core of the FOMC.

- MNI US DATA: JOLTS Reaffirms "Low Hiring, Low Firing" Labor Market Narrative. Job openings were relatively steady in August in the latest JOLTS report, totaling 7,227k (SA, vs 7,200k consensus) with July's slightly upwardly revised to 7,208k (from 7,181k). But secondary metrics suggested further loosening in labor market conditions, and while there was no marked deterioration in the month, overall the report bolstered the prevailing "low hiring, low firing" narrative.

- Data/Events: MBA Mortgage Applications, ADP Employment Change, S&P Global US Manufacturing PMI, ISM Manufacturing, Construction Spending

MNI: BOJ: MAJOR FIRM FY25 CAPEX PLANS ABOVE HISTORICAL AVERAGE

- BOJ: MAJOR FIRM FY25 CAPEX PLANS ABOVE HISTORICAL AVERAGE