US STOCKS: S&P(ESU5) - Moves Quickly To 6600 On Benign Inflation Data

The S&P(ESU5) overnight range was 6535.50 - 6600.00, SPX closed +0.85%, Asia is currently trading around 6592. The S&P made new all-time highs again, ignoring any concerns for growth as inflation came in as expected. This morning US futures have opened pretty muted, E-minis -0.01%, NQU5 -0.01%. The stock market continues to look overdone and is in what is supposed to be a difficult seasonal period, but it remains in an uptrend and there does not look to be any imminent signs of a correction yet as it continues to grind higher, dragging an underweight institutional market back in. Evidence Retail is beginning to take some profit as Wall street is forced back in, who is the smart money now ?

- Bloomberg - US stocks climbed on Thursday, posting fresh records amid hopes that an in-line inflation report will push the Federal Reserve to cut interest rates next week. Traders expect stocks to brush off weaker jobs data to end the year higher, with investors remaining optimistic despite warning signs within the S&P 500.”

- Otavio Costa on X: "Classic stagflationary behavior: Gold stocks have crushed every sector of the S&P 500 this year."

- Lance Roberts on X: "Yesterday, Goldman posted the following chart showing that the AI leaders basket, +10%, had its 2nd best day in the past 5 years. Apparently, the AI trade isn't dead yet.”

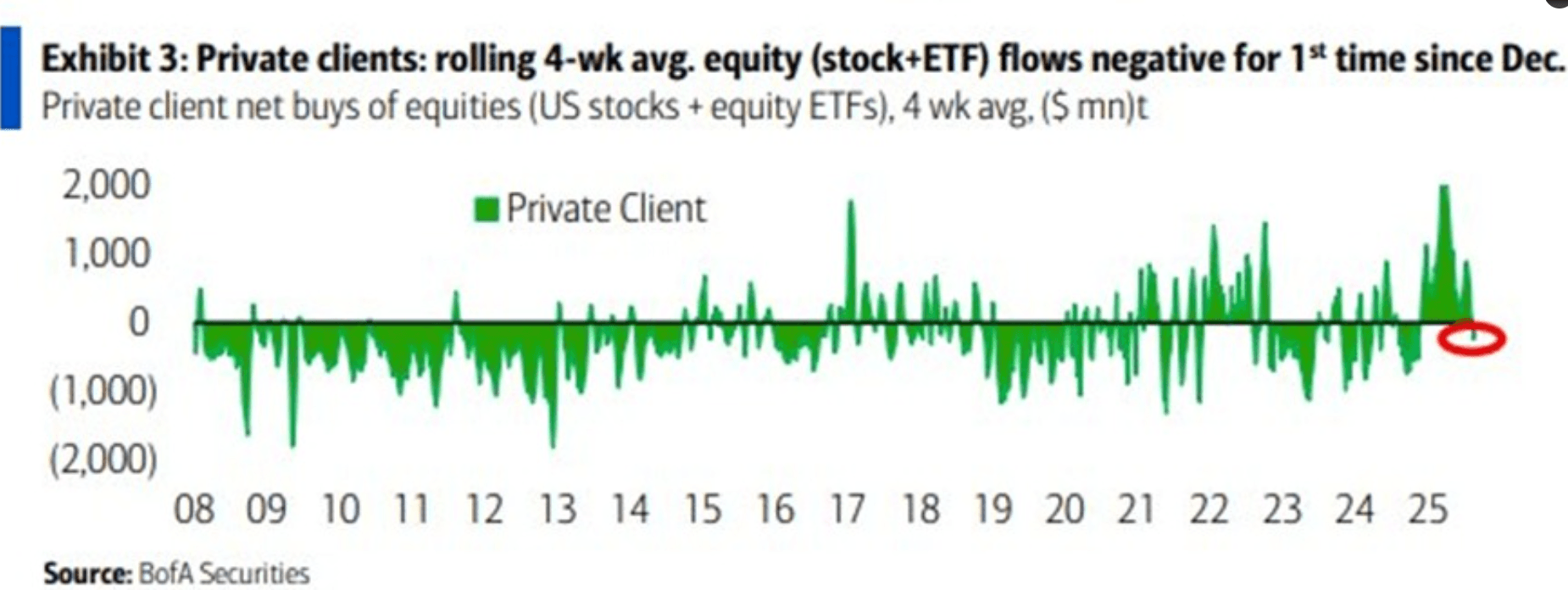

- The Kobeissi Letter on X: “Individual investors are cashing-in: Retail investors sold $700 million of US equities last week, in their 2nd weekly sale over the last 3 weeks. This comes after nearly 36 straight weeks of buying. At the same time, institutional investors bought +$1.1 billion, posting their 6th-straight weekly purchase, the longest streak since the 2022 bear market. Before this streak, they had sold -$19.0 billion over 12 weeks. Wall Street is buying while Main Street is selling.” See Graph Below.

Fig 1: Private Client Rolling Equity Flows

Source: MNI - Market News/@KobeissiLetter/BofA

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Dec-35 Supply Faces Lower Yield But Same Curve

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 4.25% 21 December 2035 bond. The line was last sold on 9 July 2025 for A$1200mn. Bidding is likely to be shaped by several key factors:

- The current outright yield is 5-10bps lower than the previous auction and approximately 50bps lower than the peak in late 2024.

- The 3/10 yield curve is around the same level as the previous auction but sits around 20bps below its recent high.

- On the negative side, the auction comes amid weaker sentiment toward longer-dated global bonds.

- However, the line is included in the XM basket.

- While some factors may limit the overall strength of bidding, there is an expectation of continued firm pricing at today's auction.

- Results are due at 0200 BST / 1100 AEST.

AUSSIE BONDS: AUCTION PREVIEW: ACGB Dec-35 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 4.25% 21 December 2035 bond. The line was last sold on 9 July 2025 for A$1200mn. The line was opened via syndication on 24 July 2024 for A$11.5bn.

- The last sale drew an average yield of 4.3442%, at a high yield of 4.3475% and was covered 2.6500x. There were 29 bidders, 16 of which were successful and 12 were allocated in full. The amount allotted at the highest yield as a percentage of the amount bid at that yield was 3.5%.

- This week's ACGB supply is at the top of the recent average weekly issuance of $1500-2200mn, with A$1000mn of the 2.75% 21 November 2029 bond due on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.

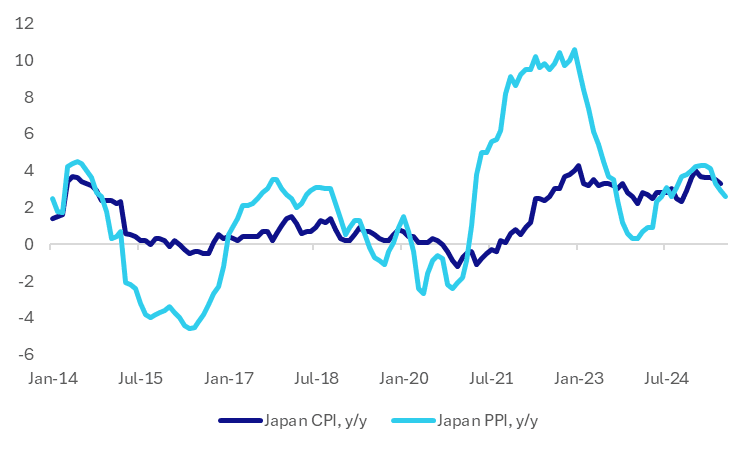

JAPAN DATA: July PPI In Line, Suggests Further Moderation In Headline Y/Y CPI

Japan's July PPI was close to expectations. The m/m outcome printed at +0.2%, in line with expectations, while the June outcome was revised to 0.1%m/m (originally reported as -0.2%). In y/y terms we printed at 2.6%, versus 2.5% forecast and 2.9% prior.

- The chart below plots the headline PPI y/y, versus the National CPI, also in y/y terms. At face value it implies some further softening in y/y CPI momentum for July. Note that this print comes out on August 22nd.

- In terms of the detail, manufacturing was up 0.2%, while some commodities, most notably petroleum, coal, rose for the first time in a number of months (+1.8%).

- The data is unlikely to shift near term BoJ thinking around wait and see mode from a policy standpoint.

Fig 1: Japan PPI & CPI, Y/Y

Source: Bloomberg Finance L.P./MNI