OIL PRODUCTS: Russian Oil Product Shipments Fall Amid Refinery Outages

Sep-19 13:44

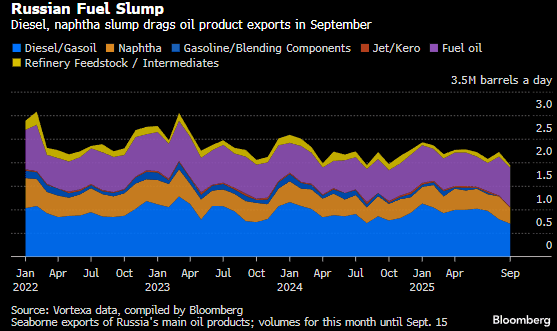

Russian oil product exports are about 300kb/d below the preceding three Septembers according to initial Vortexa data cited by Bloomberg.

- Total refined product exports are the lowest since early 2022 at 1.94mb/d in the first 15 days of September, in a sign of the impact of the recent ramp up in Ukrainian drone strikes.

- Russia’s oil refineries processed an average 4.97mb/d in the first 10 days of September and more than 70kb/d below levels in late-August., Bloomberg reported.

- Officials are considering extending the gasoline export ban through October and have urged producers to divert some diesel volumes to the domestic market.

- Diesel and gasoil exports fell 12% from August to 699kb/d driven by a drop in supply to Brazil and Africa.

- Naphtha shipments fell 30% from the August high to the yearly low at 342kb/d.

- Fuel oil edged up to the highest since April 2023 at 835kb/d driven by flows to India. Refinery feedstocks exports, including vacuum gasoil, fell to 53kb/d.

- Jet fuel exports were less than 10kb/d and no gasoline shipments were observed.

Source: Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN INFLATION: Analysts Stick To Previous ECB Calls After July Final HICP

Aug-20 13:40

Analysts aren't unanimous but on balance view the final July HICP release as favourable in terms of the ongoing disinflation process in the Eurozone. They stick to their previous calls on the ECB rates path ahead. Some highlights:

- Commerzbank: "Volatile service prices distorted the core rate slightly downward [...] As this effect is unlikely to be lasting, we are adjusting the core rate upwards accordingly. Without these volatile components, the core rate would therefore have been 0.24% in July (seasonally adjusted month-on-month rate). [...] Even with a slightly weaker core rate, year-on-year inflation is likely to remain above the ECB's forecast in the coming months. We therefore consider further interest rate cuts by the ECB to be unlikely."

- Goldman Sachs: "Looking through the Easter-related distortions to services inflation, our summary indicator of sequential underlying inflation has been broadly stable over the past few months, but ticked down in July by 5bp to 0.18%mom. The change in our sequential summary measure reflects a sequential deceleration across most of the metrics we track"

- JP Morgan: "Our inclination is to view today’s report as constructive: we do need a run of soft monthly core price gains but see a good chance of this. The firmer currency, possible China deflation effects and, crucially, the moderation in wage growth argue in this direction [...] If core goods inflation sees payback in August, Euro area core inflation could slip to 2.1%oya and remain at that level in September. If correct, it would undershoot the ECB staff forecast of 2.3%oya for 3Q25. We then see it slipping below 2%oya early next year. [...] We continue to expect a further ease but have delayed this recently to October. This does, however, require the ECB to take more seriously the easing bias already in the staff projections."

EURIBOR OPTIONS: Put Condor Buyer

Aug-20 13:37

ERH6 97.9375/97.8125/97.6875/97.5625p condor, bought for half in 7.5k.

EQUITIES: US Cash Opening Calls

Aug-20 13:26

SPX: 6,408.4 (-0.0%); DJIA: 44,953 (+0.1%/+31pts); NDX: 23,338.8 (-0.2%).