OIL PRODUCTS: Russian Fuel Shipments Fall to Lowest Since 2022 in Early Oct.

Oct-15 14:31

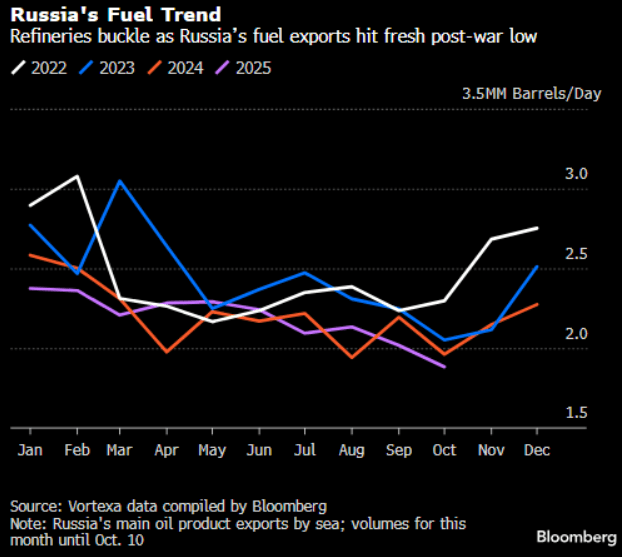

Total Russian seaborne refined fuel shipments fell to the lowest since at least the start of 2022 to an average of 1.88mb/d in the first 10 days of October, according to Vortexa data cited by Bloomberg.

- The fall reflects the impact of drone strike on Russia’s energy infrastructure. A slight rebound in diesel was set against a record low for naphtha shipments.

- Russia’s crude processing rates fell around 60kb/d w/w to average about 4.81mb/d across Oct. 2-8 as seasonal maintenance weighed in addition to the impacts of Ukrainian drone strikes.

- Diesel and gasoil exports in Oct. 1-10 rebounded 13% from September to about 850kb/d with higher Black Sea exports offsetting weak Primorsk flows.

- Naphtha shipments are down 43% to the lowest since Jan. 2022 at 198kb/d.

- Fuel oil fell 8% to the lowest in three months at 727kb/d. Refinery feedstocks exports, including vacuum gasoil, fell 38% to 44kb/d.

- Jet fuel exports more than doubled to 65kb/d while no gasoline shipments were observed.

Source: Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NORGES BANK: MNI Norges Bank Preview - Sep 2025: Another Close Call

Sep-15 14:30

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK

EXECUTIVE SUMMARY:

- At the start of the month, analyst and market expectations were fairly comfortably in favour of a 25bp Norges Bank cut on September 18th. However, domestic data released over the past two weeks have made the decision a much closer call.

- We currently lean against consensus in favour of a hold at 4.25% - a risk we thought markets were underappreciating even before the recent run of domestic data.

- If rates are held on Thursday, we expect soft guidance for a 25bp cut in December.

- Whatever the rate decision, the September MPR rate path is expected to be revised higher relative to June, pointing to a higher terminal rate landing zone than the 3.00-3.25% currently implied.

- Although market pricing still tilts in favour of a cut, price action over the past two weeks has clearly been in a hawkish direction. Recent moves, alongside the split analyst consensus, opens the door to a material knee-jerk reaction under any rate decision scenario on Thursday.

AUD: More FX Exchange traded upside Option

Sep-15 14:28

AUDUSD (7th Nov) 68.50c, bought for 0.25 in ~3.1k total (multiple clips).

GOLD: Last Tuesday's ATH Still Intact For Gold; Spot Up 0.35% Today

Sep-15 14:04

A fresh extension higher for gold prices has now faded, leaving spot up 0.35% on the session at $3,655/oz after peaking at $3,664 around 30 minutes ago.

- Initial resistance remains Tuesday’s all-time high of $3,674. Clearance of this level would expose round number resistance at $3,700.

- There hasn’t been an obvious headline driver for today’s modest gold rally. Instead, we suggest that positioning ahead of the Fed’s likely 25bp rate cut on Wednesday is factoring into price action, potentially alongside well-established Fed independence concerns following US President Trump’s latest calls for lower rates.

- A reminder that the US Senate will hold a cloture vote on Stephen Miran's Fed Board nomination at around 17:30 ET / 22:30 BST, with a full confirmation vote likely to take place at roughly 20:00 ET / 01:00 BST. Despite some reservations from institutionalist Senate Republicans, there is not expected to be any GOP opposition.

- Separately, we note that considerations around a physical gold trading tax in Thailand (due to domestic FX concerns) has not had a material impact on spot prices today.