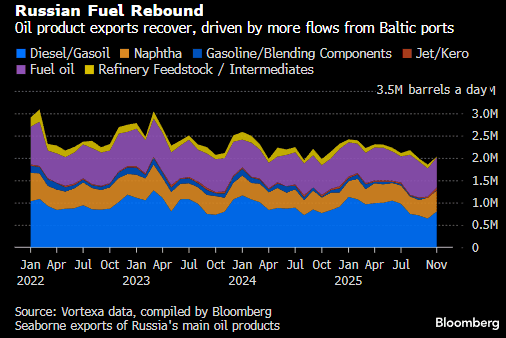

OIL PRODUCTS: Russia Fuel Shiptments Rebound From October Lows

Dec-05 13:15

Total Russian refined product exports rebounded about 10%, from a low the previous month, to a three month high of 2.03mb/d in November, according to Vortexa data cited by Bloomberg.

- A recover in Baltic shipments offset weaker exports from the Black Sea impacted by Ukrainian drone attacks. Overall fuel exports remain pressured by damage to refineries and export infrastructure as well as from tighter western sanctions.

- Diesel and gasoil exports rose 25% on the month to a four month high of 802kb/d as Baltic port shipments rose 73%, primarily driven by Primorsk. Exports to Turkey and Africa remain strong.

- Naphtha shipments rose to 468kb/d, and with 10kb/d of gasoline or blending component exports. Fuel oil rose 6% to 677kb/d while refinery feedstocks exports, including vacuum gasoil, fell to 17kb/d.

Source: Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

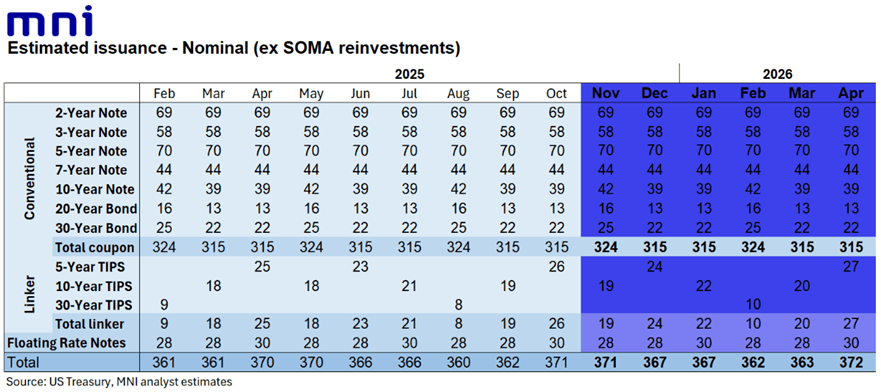

US TSYS/SUPPLY: No Change To Coupon Size Guidance, But Bills Eyed in Refunding

Nov-05 13:11

A few areas to watch in today's 0830 Refunding announcement - MNI's full preview is here

- Guidance: We do not expect Treasury’s guidance on coupon issuance to change in this Refunding round ("Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.")

- Coupon sizes for upcoming quarter (Nov-Jan): As seen in table below. The Refunding itself will be $58B in new 3Ys, $42B in new 10Y, and $25B in new 30Y for next week.

- Buybacks: After being in some focus in August's Refunding, we don’t expect any changes to buyback program parameters this time, following the last round’s amendments that included higher-frequency operations/increasing the size of long-end buybacks. There are some risks that buyback sizes could be slightly increased, or that Treasury announces that the list of eligible counterparties will be expanded.

- Bill guidance: This will be of some interest given that borrowing expectations for the coming quarter were at the lower end of the expected range - one thing to watch will be if Treasury guides to reducing bill auction sizes soon having increased them significantly in late September/early October, helping push the TGA cash pile to the $1T mark. Last time that guidance read: "Treasury anticipates further marginal increases in short-dated Treasury bill auction sizes in the coming days and then maintaining sizes at or near those levels through the end of September. Additional increases to Treasury bill auction sizes are anticipated in October. Treasury will carefully monitor market conditions and adjust its bill issuance plans as appropriate. "

STIR: Repo Reference Rates

Nov-05 13:05

- Secured Overnight Financing Rate (SOFR): 4.00% (-0.13), volume: $3.147T

- Broad General Collateral Rate (BGCR): 3.98% (-0.11), volume: $1.183T

- Tri-Party General Collateral Rate (TCR): 3.98% (-0.11), volume: $1.156T

- (rate, volume levels reflect prior session)

PIPELINE: Corporate Bond Roundup: KEPCO, Santos Finance on Tap

Nov-05 13:03

- Date $MM Issuer (Priced *, Launch #)

- 11/05 $Benchmark KEPCO 3Y SOFR+62, 5Y +47

- 11/05 $Benchmark Santos Finance 10Y +195a

- $5.7B Priced Tuesday