US STOCKS: Russell Index - Builds On Gains, Eyes The Years High Above 2540

The Russell 2000 overnight range was 2468.65 - 2512.13, closing +1.91%. The Russell 2000 has exploded off the 2300 support area and is up over 9% from those lows seen on the 20th October. With the labour data showing signs of slowing and Hassett looking like being appointed as Fed chair the market is getting excited about rate cuts and this is fueling small caps. The way small caps and the Dow Transports are trading certainly improves the breadth of this move and implies some rotation out of the larger tech stocks into the broader market. I have been wary of stocks up here but this price action is pretty bullish. For the moment the “Santa-Rally” everyone had been positioned for prior the washout looks to be materialising, and while the price remains above the 2300 pivotal support it looks like dips will be supported as focus turns toward the year's highs just above 2540.

- (Bloomberg) - Small caps have started their pre-Fed rally on expectations that more policy easing will solidify the sector’s earnings outlook at a time of economic uncertainty. {NSN T6PFTAKGIFRE <GO>}

- Sean D. Emory on X, “Forward 12-month net income estimates are rising across the board…and drum roll please...small caps are actually leading.”

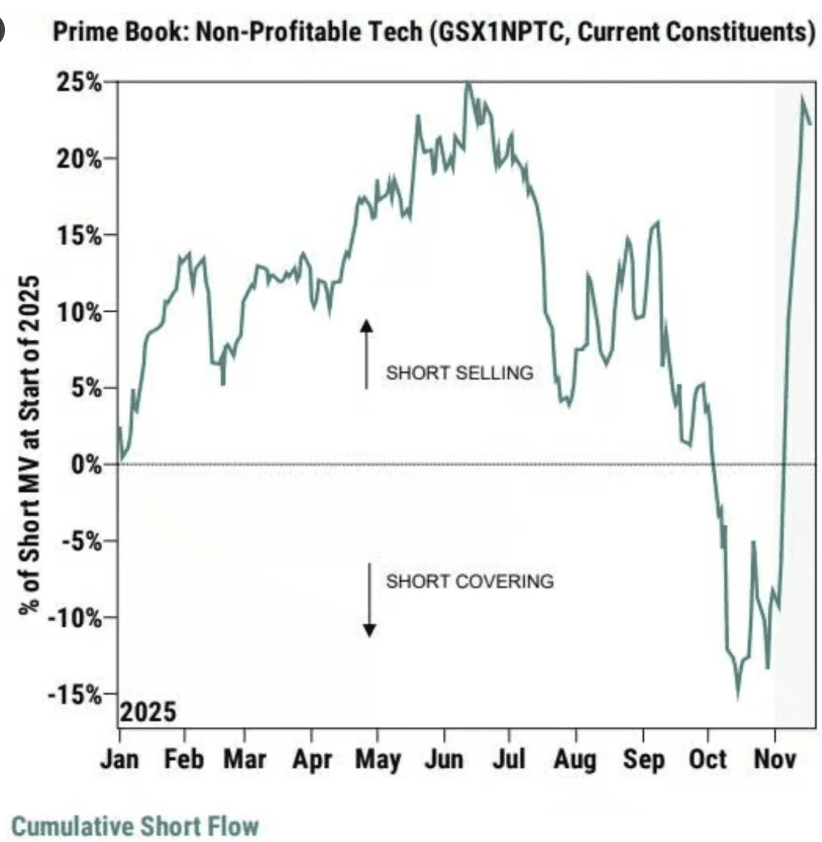

- Andreas Steno Larsen on X: “We are very close to a new complete wash out of shorts in small/mid caps now. Extreme short positioning -> rates lower -> squeeze time. Could be a violent Santa rally this one.” See Graph Below.

- The Russell 2000 Index Average True Range(ATR) for the last 10 Trading days: 41 Points

Fig 1: Cumulative Short Flow

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: Significantly Weaker Jobs Data Could Increase Easing Expectations

Q3 jobs and wages data are released Wednesday and with spare capacity an important driver of monetary easing, will be monitored closely as there has been excess supply in the labour market. Monthly data in the quarter signal there was a stabilization but employment is likely to have remained soft. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ’s August projections. A 25bp cut on 26 November is generally expected but if the labour data print significantly weaker, then expectations of 50bp may increase.

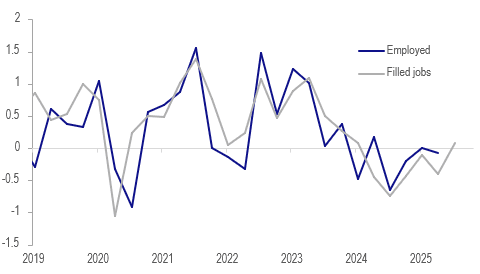

- Q3 filled jobs, vacancy and survey data all point to a stabilisation in NZ’s labour market. Average filled jobs rose 0.1% q/q after falling 0.4% in Q2.

NZ filled jobs vs employment q/q%

Source: MNI - Market News/Statistics NZ/LSEG

- In its August projections, the RBNZ forecast flat Q3 employment growth leaving the annual rate down 0.3%. It also expected private wage growth to moderate to 0.4% q/q from Q2’s 0.6%.

- Bloomberg consensus is forecasting employment to rise only 0.1% q/q and still be down 0.2% y/y with expectations in a fairly narrow range of -0.1% to +0.3% q/q. ASB, Kiwibank and Westpac are below consensus but in line with the RBNZ projecting flat jobs growth in Q3, while BNZ is at +0.1% q/q and ANZ +0.2% q/q.

- Forecasts for the unemployment rate are between 5.2% and 5.4% with ANZ, BNZ, Kiwibank and Westpac all expecting 5.3% but ASB is steady at 5.2%.

- Soft labour demand is likely weighing on private wage growth which is forecast to rise around 0.4% q/q after 0.6%. ASB, BNZ and Kiwibank are all in line with consensus, while ANZ and Westpac expect 0.5%.

USD: BBDXY - Grinds Higher, Testing Long-Term Resistance

The BBDXY range overnight was 1219.82 - 1222.54, Asia is currently trading around 1222, +0.10%. The USD continues to build on its recent gains eking out new highs every day. The 1220-30 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made on the Daily chart through October. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

Fig 1: BBDXY Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

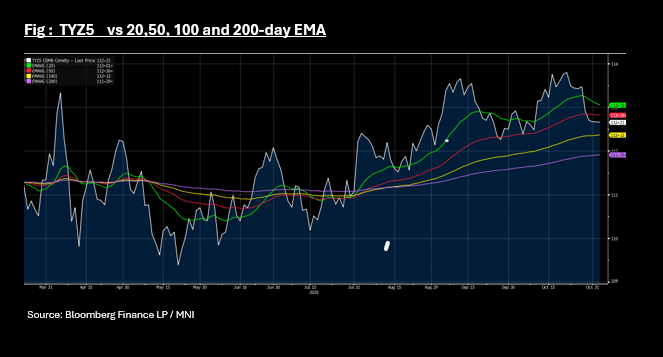

US TSYS: Slow Start as TYZ5 at Mid-Point of Key Tech Levels

A quiet start to the day for both futures and cash following a weak overnight which saw yields up to +3bps across the curve. TYZ5 opened at 112-21+ and hasn't moved with very low volumes. TYZ5 is at the mid-point of the 50-day EMA of 112-26+ and the 100-day EMA of 112-12 seeking a catalyst for the next move. The funding announcement expected this week could be the catalyst with growing expectations that a heavy skew to bills will be announced, providing support to longer bonds.

Cash is quiet at the open also inching lower in yield after last night's rise.

- The 2-Yr is marginally lower at 3.607%.

- The 5-Yr is at 3.72%

- The 10-Yr is steady at 4.11%

- The 30-Yr is -0.5bps lower at 4.68%