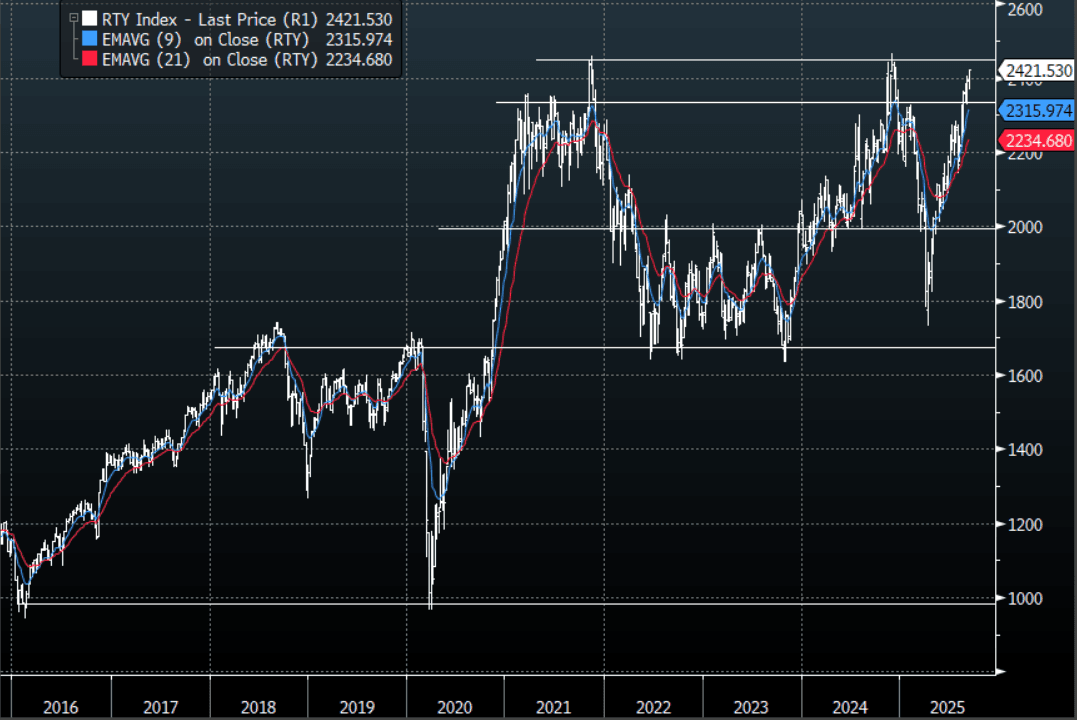

US STOCKS: Russell 2000 - Accelerates Higher After CPI, Eyes All-Time Highs

The Russell 2000 overnight range was 2379.990 - 2321.530, closing +1.83%. The Russell 2000 accelerated higher on the inflation data as the market got more comfortable pricing a new potential rate cutting cycle. This scenario could see some further rotation back into small caps which should benefit the most from a cutting cycle. The market will be laser focused on the all-time highs just above 2450, a break of which could trigger another wave of short covering from leveraged funds.

- Bloomberg - “Small Caps Catch a Bid as Fed Rate Cuts Promise More Upside. The Russell 2000 index is up the most in three weeks as traders wager that weakness in the labor market will fast-track interest-rate cuts from the Fed. History shows that small-cap stocks have rallied most after large rate reductions.”

- Andreas Steno Larsen on X: “We are making new highs more or less across the board. China, Japan, US etc. So much for the September doomers.”

- Bloomberg - “Small-Cap Revenue Recovery Still on Shaky Ground After 2Q Beat. The Russell 2000 easily beat a low second-quarter bar set by consensus that trimmed expectations based on tariff fears, but looking ahead, small-cap aggregate revenue is expected to close the gap with larger brethren.”

- CFTC data shows leveraged funds only slightly pared back their shorts last week to -76948( previously -78059). This has been cut back from a high of around -117000 at the beginning of August, new all-time highs might be the final nail in the proverbial coffin.

Fig 1: Russell 2000 Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

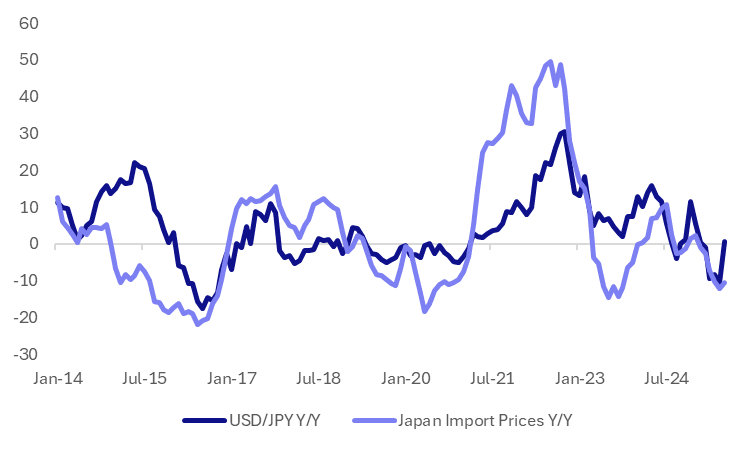

JAPAN DATA: Import Prices Up For First Month Since Jan, Y/Y Still Negative

For July, export and import prices both rose in m/m terms. Export prices were up 1.6%, while import prices were up 2.4%m/m. For import prices this was the first m/m rise since January of this year. In y/y terms, both export and import prices were still in negative territory, but up from the June levels. Export prices were -5.4%y/y, while imports were -10.4%.

- The chart below plots y/y changes in USD/JPY versus import prices y/y. To end July USD/JPY was up a touch in y/y terms. If current spot levels prevail, (currently around 147.80), USD/JPY will remain positive in y/y terms to end September (note USD/JPY was 152.03 end Oct last year).

- This implies some upside to import price y/y momentum in the near term, albeit fairly modestly. If USD/JPY holds around current level to end September, we would be up +2.9% in y/y terms.

Fig 1: Japan Import Prices & USD/JPY, Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Dec-35 Supply Faces Lower Yield But Same Curve

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 4.25% 21 December 2035 bond. The line was last sold on 9 July 2025 for A$1200mn. Bidding is likely to be shaped by several key factors:

- The current outright yield is 5-10bps lower than the previous auction and approximately 50bps lower than the peak in late 2024.

- The 3/10 yield curve is around the same level as the previous auction but sits around 20bps below its recent high.

- On the negative side, the auction comes amid weaker sentiment toward longer-dated global bonds.

- However, the line is included in the XM basket.

- While some factors may limit the overall strength of bidding, there is an expectation of continued firm pricing at today's auction.

- Results are due at 0200 BST / 1100 AEST.

AUSSIE BONDS: AUCTION PREVIEW: ACGB Dec-35 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 4.25% 21 December 2035 bond. The line was last sold on 9 July 2025 for A$1200mn. The line was opened via syndication on 24 July 2024 for A$11.5bn.

- The last sale drew an average yield of 4.3442%, at a high yield of 4.3475% and was covered 2.6500x. There were 29 bidders, 16 of which were successful and 12 were allocated in full. The amount allotted at the highest yield as a percentage of the amount bid at that yield was 3.5%.

- This week's ACGB supply is at the top of the recent average weekly issuance of $1500-2200mn, with A$1000mn of the 2.75% 21 November 2029 bond due on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.