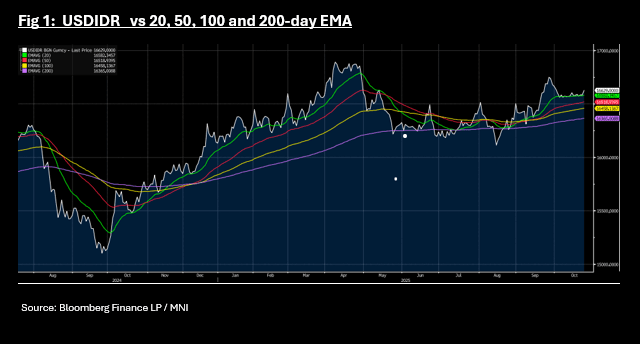

IDR: Rupiah Breaks Above 20-day EMA

Oct-24 01:52

- If the BI surprise hold this week was about stabilizing the Rupiah as many suggest, the Central Bank appears to be losing that battle as USDIDR falls by most this week today.

- Up by +44 to 16,629, the Rupias is weaker by -0.29% for the week, trading further away from a previously stated goal of 16,300 for the BI.

- The losses sees USDIDR move above the 20-day EMA of 16,582 that it had traded in line with for several weeks, looking for a catalyst for its next move. With the market forming a strong consensus for a cut, the BI would have been hoping that the hold would provide an opportunity for the Rupiah to strengthen.

- The Jakarta Composite has reacted more positively to the hold, up +1.50% today and +1.85% for the week, whilst bonds are modestly weaker with the 10-Yr +3bps for the week at 5.99%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bonds Slightly Mixed After Yesterday's Holiday

Sep-24 01:49

In Tokyo morning trade, JGB futures are stronger, +4 compared to settlement levels, after yesterday’s holiday.

- Japan's preliminary S&P PMIs for September were below the August outcomes. Manufacturing printed at 48.4, versus 49.7 in August. The services print was 53.0, against a 53.1 prior. The composite fell to 51.1 versus 52.0 in August.

- The manufacturing print is back to lows from March of this year. We did get close to 47.0 for the index in Q1 of 2024. The detail showed output down to 47.3 from 49.8 in August. New orders were also down in the month. The US manufacturing PMI fell for Sep as well, although it remains at much higher outright levels (52.0).

- On the services side for Japan, we remain at elevated levels. There remains a decent wedge between the manufacturing and services PMIs.

- Cash US tsys are little changed in today’s Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 1.3bp lower (20-year) to 0.7bp higher (40-year). The benchmark 10-year yield is 0.8bp lower at 1.646% versus the cycle high of 1.670%.

- Swap rates are flat to 2bps lower.

AUSSIE BONDS: Cheaper After CPI Beat

Sep-24 01:41

ACGBs (YM -4.5 & XM -2.0) are slightly weaker after the August CPI data beat estimates.

- Headline CPI rose 3.0% y/y (estimate +2.9%) in August versus +2.8% in July. The estimate range was +2.4% to +3.3% across 22 economists. Trimmed mean CPI rose 2.6% y/y versus +2.7% in July.

- (ABS) “The 3.0 per cent annual CPI inflation to August was up from 2.8 per cent to July, making this the highest annual inflation rate since July 2024. The largest contributors to annual inflation were Housing (+4.5 per cent), Food and non-alcoholic beverages (+3.0 per cent), and Alcohol and tobacco (+6.0 per cent).

- When prices for some items change significantly, measures of underlying inflation (like the annual trimmed mean and CPI excluding volatile items and holiday travel) can give more insights into how inflation is trending. CPI excluding volatile items and holiday travel rose 3.4 per cent in the 12 months to August, compared to a 3.2 per cent rise in the 12 months to July."

- Cash US tsys are little changed in today’s Asia-Pac session.

- Cash ACGBs are 2-4bps cheaper after the data, with a flatter curve and the AU-US 10-year yield differential at +17bps.

- The bills strip is -4 to -5 across contracts.

- RBA-dated OIS pricing is firmer across meetings after the data. A 25bp rate cut in September is given a 2% probability, with a cumulative 22bps of easing priced by year-end (based on an effective cash rate of 3.60%).

AUD: Reaction To CPI

Sep-24 01:37

The AUD went into the Unemployment print trading around 0.6590(-0.05%) and the SPI was trading around 8820.0(-0.60%). “AUSTRALIA AUG. CONSUMER PRICES RISE 3.0% Y/Y; EST. 2.9%, AUSTRALIA AUG. TRIMMED MEAN CPI RISES 2.6% Y/Y.” The AUD has bounced a little in reaction to this print.

- AUD/USD - 0.6605, +0.10%

- AUD/NZD - 1.1280, +0.15%

- EUR/AUD - 1.7865, -0.25%

- AUD/JPY - 97.60, +0.20%

- SPI(XPU5) - 8810, -0.80%

- OIS 2 bps firmer for 2026 meetings, YM 1-2 bps cheaper, XM 1-2 bps cheaper