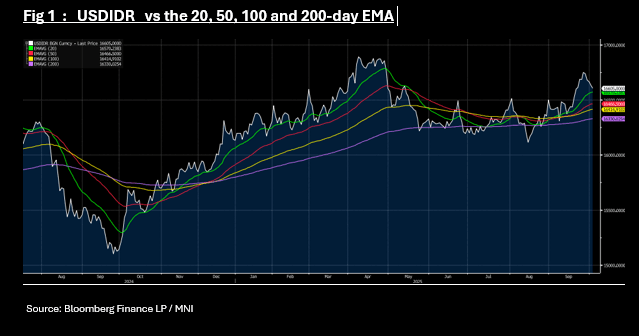

IDR: Rupiah Banks Gains Again in Morning Trade

- The Rupiah has had modest gains again today, similar to yesterday.

- At 16,609 it has gained -0.16% as it continues to edge lower from last week's wides of 16,750.

- The gains in recent days sees USDIDR approach the 20-day EMA of 16,570. It has not been able to hold below the 20-day EMA for a sustained period for more than a month.

- USDIDR 1 month ATM Vol has moved lower to 6.74, from 6.81 yesterday.

- The Jakarta Composite is up +0.35% today, taking it back to flat over the last 5-days of trading whilst bonds yields are bond yields are lower across the curve, with the short end the best performer.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSTRALIA: Local Banks Q2 GDP Forecasts Below Consensus

Q2 GDP prints on Wednesday and Bloomberg consensus is forecasting a 0.5% q/q increase bringing annual growth to 1.6% from Q1’s 1.3%, in line with the RBA’s August projection. However, almost all estimates were provided before this week’s inventory, net export and public demand data. Inventories were close to consensus and net exports were in line.

- Q2 data show only a 0.1pp contribution to growth from net exports and nothing from public demand as government consumption’s 0.2pp was offset by the 0.2pp drop in public investment. The 0.1% q/q rise in inventories is likely to mean it had a neutral effect on growth.

- Real household consumption rose 0.7% q/q after 0.5%, which may drive a small increase in private consumption growth from Q1’s 0.4% q/q.

- Private capex volumes posted a modest 0.2% q/q in Q2 and so are unlikely to contribute to growth.

- Consensus estimates range from +0.3% q/q to +0.7% q/q and 1.4%-1.9% y/y. ANZ revised down its forecast by 0.2pp to 0.4% q/q following Q2 data. The other local banks are also expecting GDP to be below consensus with NAB forecasting +0.3% q/q & 1.4% y/y and CBA and Westpac both at 0.4% q/q & 1.5% y/y.

JGBS: Futures Bounce Post 10yr Auction, But Limited Follow Through

JGB futures have risen in the aftermath of the strong 10yr JGB auction result. We were last 137.48, +.18 versus settlement levels. Post lunchtime break highs were at 137.62, which was just short of earlier Sep highs (137.66), so recent ranges are still holding. The Sep contract opened at 137.32. JGBs are outperforming US Tsy futures, which remain weaker, but are up from session lows.

- The 10yr auction saw a bid to cover ratio of 3.92, versus 3.06 at the prior auction (note the 12-month moving average of the bid to cover ratio is 3.17, per BBG). The tail of the auction was 0.06, versus the 0.14 from the prior outcome.

- Market sentiment was somewhat bearish heading into the auction result, given last week's poor 2yr auction outcome and a slightly heavier US Tsy futures backdrop.

- Still, it may not be a turning point for futures. Earlier headlines crossed: "JAPAN PM ISHIBA MAKING ARRANGEMENT TO INSTRUCT MINISTERS AS EARLY AS THIS WEEK TO COMPILE ECONOMIC MEASURES TO ADDRESS INFLATION, TRUMP TARIFFS, SANKEI NEWSPAPER SAYS - [RTRS]"

- Hence pressure is likely to remain on the government to provide fiscal support.

- Earlier we heard from BoJ Deputy Governor Himino, who struck a balanced tone. He said Tuesday the Bank would raise its policy rate to adjust the degree of monetary accommodation if its baseline scenario for economic activity and prices materialises, though he gave no guidance on timing or pace.

- In the cash JGB yield space, the belly part of the curve is weaker in yield terms, with the 7 and 10yr yield tenors off over 2bps. This puts the 10yr back close to 1.60%. 20-40yr yield tenors are still holding higher in yield terms. The 2/30s JGB curve is 2bps steeper to +234bps.

BONDS: NZGBS: 2/10s Curve To Steepest Level Since April

NZGB yields have seen a steeper bias through Tuesday trade. 10 to 30yr yield tenors are up a little over 4bps, while the 2yr is up less than 1bps. This leaves the 2/10s curve close to +143bps, which is highs back to April of this year. This looks to the playing some catch up with US moves, with the 2/10s Tsy curve just off late August highs.

- The outright 2yr yield remains sub 3.00%, while the 10yr yield is around 4.40%. The 2yr swap rate has risen around 2bps to be near 2.76% in latest dealings.

- US Tsy yields have re-opened, with yields pushing higher across the curve, albeit with gains in the 1-1.5bps region at this stage.

- In terms of data, NZ saw the largest improvement in the merchandise terms of trade in Q2 since Q1 2024. It rose 4.1% q/q, the sixth consecutive quarterly increase, to be up 12.2% y/y after 10.3% y/y in Q1. While domestic demand remains soft, this rise in the terms of trade will be providing some welcome support to growth.

- Via BBG: " The data inflow has improved at the margin over the past fortnight signaling better times ahead, but current economic activity is soft, the Treasury Dept. says in its Fortnightly Economic Update published Tuesday in Wellington."

- Tomorrow, the data calendar sees ANZ commodity prices for August.