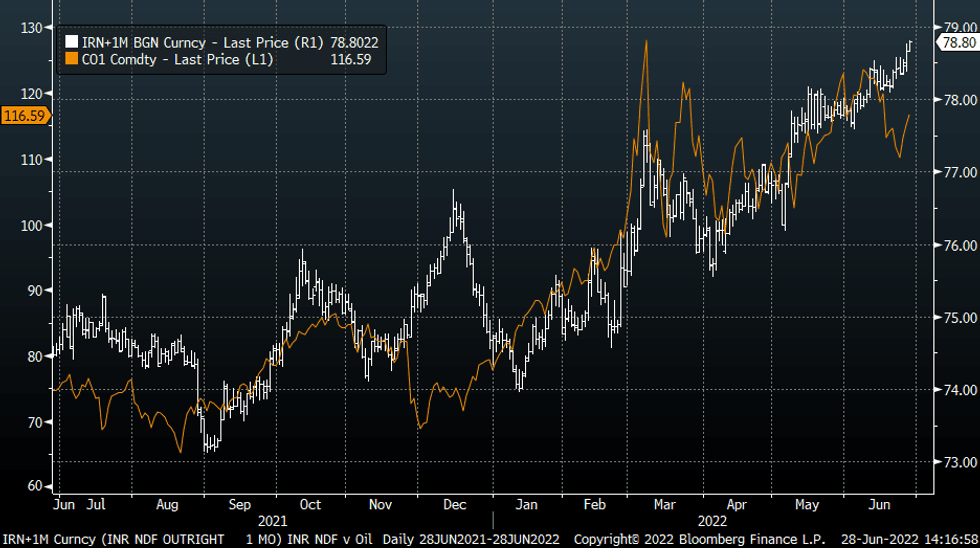

INR: USD/INR To Fresh Record Highs

Spot USD/INR is pushing higher, up +0.35% versus yesterday's close. This puts us above 78.60, which is fresh record highs for the pair. The 1-month NDF has also pushed to 78.84, also a fresh high.

- The +$8/bbl gains in Brent crude from last week's lows is clearly weighing. The chart below plots the 1 month USD/INR NDF against Brent crude prices.

- The recent pull back in oil prices saw only limited USD/INR downside, which hints to firm underlying USD demand. As we have noted in recent weeks the RBI has clearly been curbing the rate of rupee depreciation.

- Fresh record lows in the currency will draw the RBI's attention, so we are mindful of intervention risks, but again this appears to be aimed at the rate of depreciation rather than the underlying trend.

- India equities are also weaker in early trade (-0.50%), while onshore bond yields are also higher. More so at the back end though. 10yr at +3bps to 7.44%. We are still below recent highs of just above 7.60%.

Fig 1: USD/INR 1 Month NDF & Brent Crude

Source: MNI - Market News/ Bloomberg

Source: MNI - Market News/ Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late Risk Appetite Gathers Momentum

Midweek risk-on tone gathered momentum into Fri's close: Tsys steady/mixed with long end firmer but near second half lows while stocks continued to extend rally.

- SPX eminis were up near 5% for the week as risk appetite improved following Wed's May FOMC minutes release that showed a flexible Fed and no discussion of larger rate hikes ESM2 +105.25 (2.47%) at 4161.0.

- Bonds receded off early session highs post data, Apr core PCE at 4.9% YoY but headline of 6.3% YoY slightly higher than expected and fastest of last three months.

- Aside from PCE, Apr Advance Goods Trade Balance shows deficit of $105.9B vs. $114.9B expected; Wholesale Inventories +2.1% MoM vs. +2.0% exp.

- General quiet ahead Monday, May 30 Memorial Day national holiday. Cash FI markets closed while Globex opens at normal time Sunday evening at 1800ET through Monday at 1300ET. Globex reopens at 1800ET Monday evening.

- Tuesday focus: FHFA House Price Index MoM (2.1%, 2.0%); QoQ (3.3%, --); MNI Chicago PMI (56.4, 54.8); Conf. Board Consumer Confidence (107.3, 103.5); May-31 1030 Dallas Fed Manf. Activity (1.1, 1.5)

USDCAD TECHS: Fresh Bear Cycle Low

- RES 4: 1.3091 High Nov 24 2020

- RES 3: 1.3077 High May 16 and the bull trigger

- RES 2: 1.2982 High May 16

- RES 1: 1.2896 High May 18

- PRICE: 1.2742 @ 15:47 BST May 27

- SUP 1: 1.2728 Low May 27

- SUP 2: 1.2714 Low May 5 and a key support

- SUP 3: 1.2568 Low Apr 22

- SUP 4: 1.2459 Low Apr 21

USDCAD traded lower Friday and has breached support at 1.2765, May 24 low. This also means that the pair is below its 50-day EMA. An extension lower would open the next key short-term support at 1.2714, May 5 low. The latest bear leg is still considered corrective and the broader trend outlook is bullish. Initial resistance is at 1.2896, May 18 high. A break would signal a potential bullish reversal.

GLOBAL: Fiscal Tightening And Yield Curves

An excerpt from this month's MNI's Macro Deep Dive focusing on structural drivers from fiscal policy (full note here: https://marketnews.com/mni-macro-deep-dive-may-2022).

- Fiscal policy is clearly just a single factor behind yield curves yet the countries that have the flattest curves also happen to be those expected to see the largest cumulative tightening over 2022 and 2023.

- Tightening here is the annual change in the cyclically adjusted primary balance taken from the IMF's Fiscal Monitor published Apr-2022.

- Of the G10, the UK and Australia could be more prone to further flattening.

- That’s not to say the impact of tighter fiscal policy can’t be felt further on growth expectations though, with only the Czech curve already inverted and with scope for others to follow suit if recession fears do mount.