EMERGING MARKETS: Romania: IMF Consultation Concluded – Neutral

(ROMANI; Baa3neg/BBB-neg/BBB-neg)

• The IMF stressed the importance of following through on the fiscal consolidation enacted July 2025. The fiscal deficit was 9.3% in 2024 but the tax reforms and budget cuts were expected to reduce that to about 6% by next year, according to Moody’s. The IMF noted its eventual expectation of a 3% fiscal deficit in a few years.

• Mounting debt/GDP that was projected to hit 70% was revised to a more acceptable 65% by Moody’s which could preserve investment grade ratings. That has been reflected in spreads with ROMANI 35s last quoted at T+200, in from a wide of T+340bp set back in May.

• The IMF expected inflation to remain elevated at about 7% through next year and economic growth to be sluggish, with GDP projected to be 1% in 2025 and 1.4% in 2026. They suggested advancing structural reforms to make efficient use of EU funds and to support growth.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

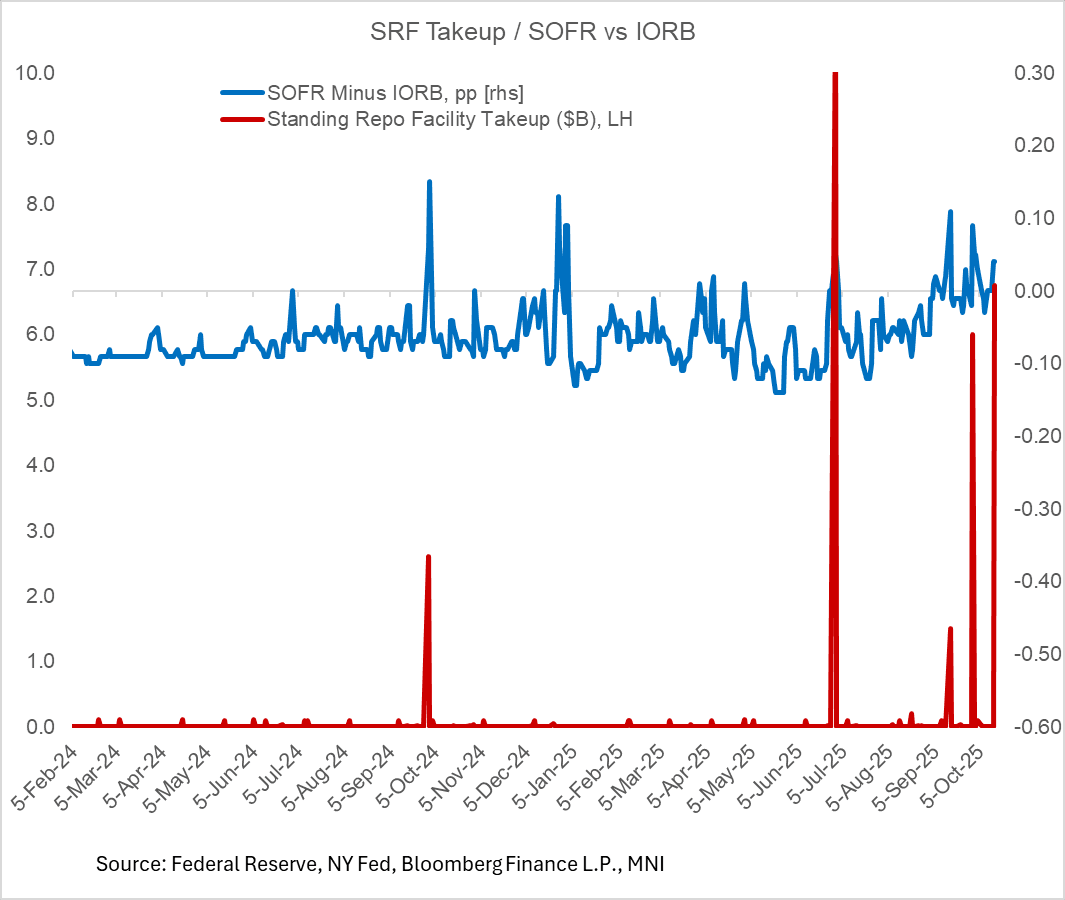

US TSYS/OVERNIGHT REPO: Fed Standing Repo Takeup Jump Part Of Wider Pressure

The Fed's Standing Repo Facility (SRF) saw its highest takeup this morning since the quarter-/month-end date of June 30.

- The $6.8B usage of the facility comes as SOFR printed 4bp above IORB (4.19% vs 4.15%) yesterday, with a variety of other indicators suggesting mounting funding market pressures. It compares with the $6.0B takeup at the last month-/quarter end date of September, and is the 2rd-highest takeup (after June 30) since Q2 2020. (The SRF was made permanent in 2021).

- Even so this rise should be put into perspective; takeup was many times larger in 2019 during a previous episode of funding pressures that led to the Fed restarting asset purchases. And per the September meeting minutes, "a few participants noted that the SRF would help keep the federal funds rate within its target range and ensure that temporary pressures in money markets would not disrupt the ongoing reduction in Federal Reserve securities holdings to the level needed to implement monetary policy efficiently and effectively in the Committee’s ample-reserves regime"

- Even so, there's a variety of factors contributing to the rise in takeup. Based on various measures we (and the Fed) look at, some funding market pressure has been building up for a few weeks now as reserves fell below $3T - the pressures are still on the light side but enough to get the Fed thinking about slowing runoff (as evidenced by Chair Powell's speech Tuesday in which he suggested QT could end in the coming months).

- Today's pressures may be related to a tax date and decently large coupon settlements (just under $40B, sandwiched between $52B in bills combined over Tuesday and Thursday) removing reserves from the system.

- SOFR was 4.19% Tuesday so it wouldn't be surprising if it weren't far below the 4.25% SRF rate today, making it a closer-than-usual tradeoff.

BONDS: EGBs-GILTS CASH CLOSE: OATs' Continued Gains Buoys Broader Space

European curves continued to bull flatten Wednesday, with French outperformance continuing.

- Longer-end yields gapped lower on the open and continued lower for most of the session, buoyed by comments after Tuesday's cash close by Fed Chair Powell pointing to a possible end to QT in coming months, as well as a perception of easing French political risks.

- In a light session for data (including some final national-level Eurozone September inflation readings), Euro area industrial production shrank less than expected in August but all four of the largest countries saw declines.

- On the day, Gilts twist flattened with Bunds bull flattening. UK 2s10s had their flattest close since early July; for Germany, March.

- Periphery/semi-core EGB spreads closed tighter, led by Italy and France.

- Thursday's scheduled highlight is UK monthly activity data, while we get multiple central bank speakers including BOE's Mann and Greene, and ECB''s Wunsch, Kocher, Lane, and Lagarde. On the French political front we also get no-confidence motions on the government.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 1.3bps at 1.922%, 5-Yr is down 3.6bps at 2.166%, 10-Yr is down 3.9bps at 2.571%, and 30-Yr is down 4.6bps at 3.146%.

- UK: The 2-Yr yield is up 0.1bps at 3.902%, 5-Yr is down 3.7bps at 4.001%, 10-Yr is down 4.7bps at 4.543%, and 30-Yr is down 5.1bps at 5.343%.

- Italian BTP spread up 2.6bps at 80.9bps / French OAT down 2.3bps at 77.5bps

US TSYS: Late SOFR/Treasury Option Roundup: Two Way Calls as Underlying Retreats

SOFR and Treasury option flow leaned towards calls on two-way trade on net after underlying futures retreated. Projected rate cut pricing largely steady vs. late Tuesday levels (*): Oct'25 at -24.5bp (-24.5bp), Dec'25 at -48.4bp (-48.4bp), Jan'26 at -61.5bp (-61.2bp), Mar'26 at -74.4bp (-74.1bp).

- SOFR Options:

- 5,000 3QX5 96.75 calls vs. 3QF6 96.75/97.75 call spds, 4.5 net cr conditional curve steepener

- +15,000 SFRZ5 96.00 puts cab

- +6,000 SFRZ5 96.00 puts, .25 ref 96.375

- -10,000 SFRH6 96.50/96.68/96.87/97.06 call condors, 4.75 ref 96.605

- +2,500 0QZ5 97.50/98.00/98.50 call flys, 2.0

- +2,500 SFRM6 97.00/98.00/99.00 call flys, 11.25

- -5,000 0QZ5 96.50/96.75 2x1 put spds, 1.5

- 3,300 SFRM6 98.00/98.12 call spds, 0.5 ref 96.84

- 4,500 SFRX5 97.00 calls, cab ref 96.365 ref 96.365 to -.37

- +2,000 SFRF6 97.00/97.50 2x1 put spds, 0.5

- +8,000 SFRZ5 96.25/96.43 2x1 put spds, 5.5 ref 96.37

- +1,250 SFRX5 96.18/96.37/96.56 iron flys, 6.5 ref 96.375

- Treasury Options:

- 5,750 TYG6 111 puts, 26 ref 113-04

- Block, 5,000 TYZ5 115/TYG6 116 call spds on 2:3 ratio, 44 net vs. 113-08

- 10,000 TYZ5 114.5 calls, 22 ref 113-15, total volume over 23,500

- over 9,000 TYX5 114.5 calls, 4 ref 104-14 to -14.5, total volume over 12,600

- 5,000 TYX5 113/113.5/114 2x1x1 call trees, 45 ref 113-14

- -40,000 TYZ5 113.5/115 call spreads, 30 vs. 113-16/0.29%

- 3,000 USZ5 120/122 call spds

- +5,500 TYZ5 111/112 put spds vs. 116 calls, even net

- +3,000 TYX5 115/116 1x2 call spds, 0.0

- +2,000 TYZ5 114.5/115.5 call spds, 13 ref 113-15

- +2,000 TYZ5 114.5/115 call spds, 8 ref 113-15.5

- +2,000 TYX5 111.5/112/112.5/113 put condors, 6.0

- over 8,000 TYX5 114 calls, 10

- 2,000 FVZ5 108.5 puts, 5 ref 109-24.75 to -25

- 2,000 USZ5 110/114 2x1 put spds, 10 vs. 118-07/0.06%

- +4,000 TYZ5 111/112 put spds, 9