SCANDIS: Risk To Next Thursday’s Central Bank Decisions Bullish For NOKSEK

May-02 11:55

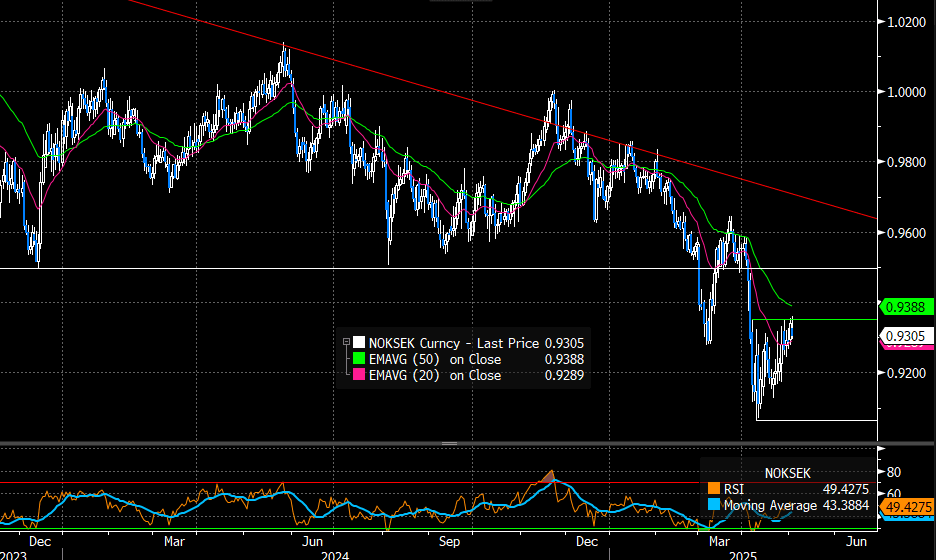

We currently view the risks to next Thursday’s Norges and Riksbank decisions as bullish for NOKSEK. The cross is down 0.4% on the session - with the SEK benefitting more from the constructive risk backdrop and weaker USD – but has consolidated above the 20-day EMA this week. Should this EMA hold, it will support an extension of the corrective rally from the April 9 low of 0.9065, with 0.9353 (April 7 high) and 0.9392 (50-day EMA) the next topside levels to watch.

- The Riksbank is expected to keep rates on hold at 2.25% on Thursday. Although the May decision does not include an updated set of macroeconomic forecasts and rate path projection, we still think there is scope to open the door to another rate cut later this year, conditional on downside growth risks materialising.

- Meanwhile, we do not think there is enough to support a dovish Norges Bank guidance tilt. CPI-ATE inflation remains above 3% and there are not yet signs of deteriorating labour market conditions.

- We expect that current Norges guidance stating “the policy rate will most likely be reduced in the course of 2025” will remain in the policy statement, which may temper expectations for a June cut. Markets currently price a ~70% implied probability of such a move, which feels too dovish at this stage.

Figure 1: NOKSEK Since 2024

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN INFLATION: MNI Eurozone Inflation Insight – March 2025

Apr-02 11:53

- While Eurozone headline HICP met expectations in March’s flash estimate, at 2.2% Y/Y, the more dovish cohort of the ECB is likely to be encouraged by the continued moderation in the year-over-year services inflation rate seen this time; its slowdown to 3.4% marks its joint slowest pace since January 2022.

- However, data including the seasonal-adjusted measures from the ECB indicate that the current pace in the category remains elevated. That could underpin the governing council’s level of weariness level after a potential April cut, which markets view as the base case for the ECB for now.

- The market reaction to the flash inflation round was mixed across key countries, with notable deviations from consensus in different countries. France surprised with a negative 0.2pp deviation (as it did last time), recording a 0.9% Y/Y headline rate, and was followed by Spain coming in at 2.5% with a -0.3pp deviation. Germany also surprised consensus to the downside, by 0.1pp at 2.3% Y/Y, but both the Netherlands and Italy came in firmer than expected (+0.1pp at 3.4% and +0.3pp at 2.1pp, respectively).

OPTIONS: Vol Markets Identify CAD, EUR, MXN, PLN and HUF as Exposed to Tariffs

Apr-02 11:43

- Currency options markets have identified CAD, EUR, MXN, PLN and HUF as being the most exposed to tariff risk headed into Trump's Rose Garden appearance later today. Trump is scheduled to begin his tariff announcement from 1600ET/2100BST - but it remains unclear how the details will be released, reinforcing the likelihood of intraday vol through the US cash equity close.

- We anticipate Trump will opt for a broad country-by-country approach, targeting those that maintain the largest goods trade surpluses with the US. While blanket tariffs or a tiered system remain viable options, this would leave countries including, but not limited to, the EU, China, Mexico, Canada, Japan and South Korea particularly sensitive.

- As a result, CAD overnight implied vols are posting the largest risk premium across G10, pushing implied to 18 points for the third time this year, rivalling the pre-Fentanyl tariff vol events in February and March. This blows out the break-even on an overnight USD/CAD straddle to ~100pips, well over double the YTD average, implying significant two-way risk into Thursday's NY cut.

- Those looking to play USD/CAD downside as part of a tariff-relief play eye breaking even on an ATM 3m USD/CAD put with spot below approx. 1.4075 at expiry (or 1.4125 should an up-and-out barrier be added at the February highs).

OUTLOOK: Price Signal Summary - Gilts Approach A Short-Term Trendline Resistance

Apr-02 11:25

- In the FI space, Bund futures are trading at their recent highs. The latest recovery is considered corrective, however, the breach of the 20-day EMA and a print above resistance at 129.41, the Jan 14 low, strengthens a bullish theme and opens the 130.00 handle and 130.26, the 61.8% retracement of the Feb 28 - Mar 11 bear leg. Key short-term support to watch lies at 127.74, the Mar 25 low. Clearance of this level would highlight a reversal. Initial support lies at 128.47, the Mar 28 low.

- The short-term trend outlook in Gilt futures remains bearish, however, recent gains highlight a corrective cycle and this signals scope for a stronger recovery near-term. An extension would open 92.42, a trendline resistance drawn from the Mar 4 high. Clearance of this level would strengthen the short-term bull cycle. Key support and the bear trigger has been defined at 90.55, the Mar 27 low. First support lies at 91.59, the Mar 31 low.