US TSYS: Risk-Off Sees Strong UST Rally, 10-Yr Breaks Below Key Resistance

- Treasuries saw session highs with TYZ5 113-24 - highest since September on weak day for equities though with the S&P down -0.63%, the move in yields seems overdone. TYZ5 is opening in the Asia trading day at 113-24

- There was no specific headline or significant block related trades to cite for the move (though large dec 10Yr call spread sale went through), with some desks pointing to overreaction of story on two regional banks getting hit (Zions and Western Alliance Bancorp) on fraud disclosures. First look is that amounts are small relative to balance sheet of the banks.

- The Dallas Fed's Weekly Economic Index (WEI) jumped to its strongest in 7 weeks in the week ending Oct 11, at 2.51% vs 2.45% prior which is roughly consistent with Q/Q SAAR GDP growth of 3%. Philly Fed Business outlook cratered to -12.8 (from 23.2) and NY Fed Services Business Activity continued its contraction down -23.6 in October from -19.4 in September.

- Fed Funds implied rates have pared broad risk-off moves but still hold a sizeable slide on the day (Dec 25 rate 4.5bp lower on the day, Jun 26 rate 7bp lower). Cumulative cuts from 4.10% effective: 25bp Oct, 51.5bp Dec, 66bp Jan, 79.5bp Mar, 87.5bp Apr and 102bp Jun.

- US 2-Yr fell sharply to 3.42% a decline of -7bps

- US 5-Yr declined -7bps to 3.54%

- US 10-Yr lower by 3.97%, finally breaking the 4.00%-4.20% range it has traded of late. The move in the 10-Yr today seems outsized relative to the data and fall in equities, and the move tonight to see whether the 10-Yr can hold below 4.00% is key.

- US 30-Yr fell -4bps to 4.58%, back to April levels when the trade war was ramping up.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNH At Fresh Lows For 2025, But Lags Broader Dollar Weakness

USD/CNH tracks near 7.1050 in early Wednesday dealings. CNH rose 0.20% for Tuesday's session, as USD indices lost ground, the DXY down around 0.65%, while the BBDYX index fell by 0.50%. Dollar weakness continues in the lead up to the Fed meeting outcome, with better than expected US retail sales data on Tuesday not aiding dollar sentiment. EUR/USD got to fresh cycle highs of 1.1878, with CNH lagging broader dollar weakness. Spot USD/CNY finished up yesterday at 7.1144, while the CNY CFETS basket tracker fell by a further 0.20% to 96.335.

- For USD/CNH technicals, downside focus will rest on a test under 7.1000. Early Nov lows from last year came in at 7.0869. Key EMA resistance points continue to track lower, the 50-day now around 7.1560. EUR/CNH sits near 8.4300 in early Wednesday dealings, with early July highs at 8.4643 not too far away. CNH/JPY was last around 20.6130, lower, but still within Sep ranges.

- US-CH 2yr yield differentials are close to +207bps, around fresh cycle lows since early 2024. In the equity space, local onshore markets were mixed yesterday, but the Golden Dragon Index rose 1.8% in Tuesday US trade.

- Per our onshore China policy team: Beijing will pursue a 19-point action plan aimed at boosting service consumption across five key areas, the Ministry of Commerce said on Tuesday. According to the ministry, officials will cultivate platforms to stimulate service consumption and expand fiscal and financial support.

- US Tsy Secretary Bessent stated further talks will be held in Germany between US and China ahead of the Nov 10 reciprocal tariff deadline.

OIL: US Crude Inventory Drawdown Last Week

Bloomberg reported a large US inventory drawdown of 3.4mn barrels with 400k at key hub Cushing last week, according to people familiar with the API data. Gasoline stocks fell 700k but distillate rose 1.9mn. The official EIA data is out on Wednesday.

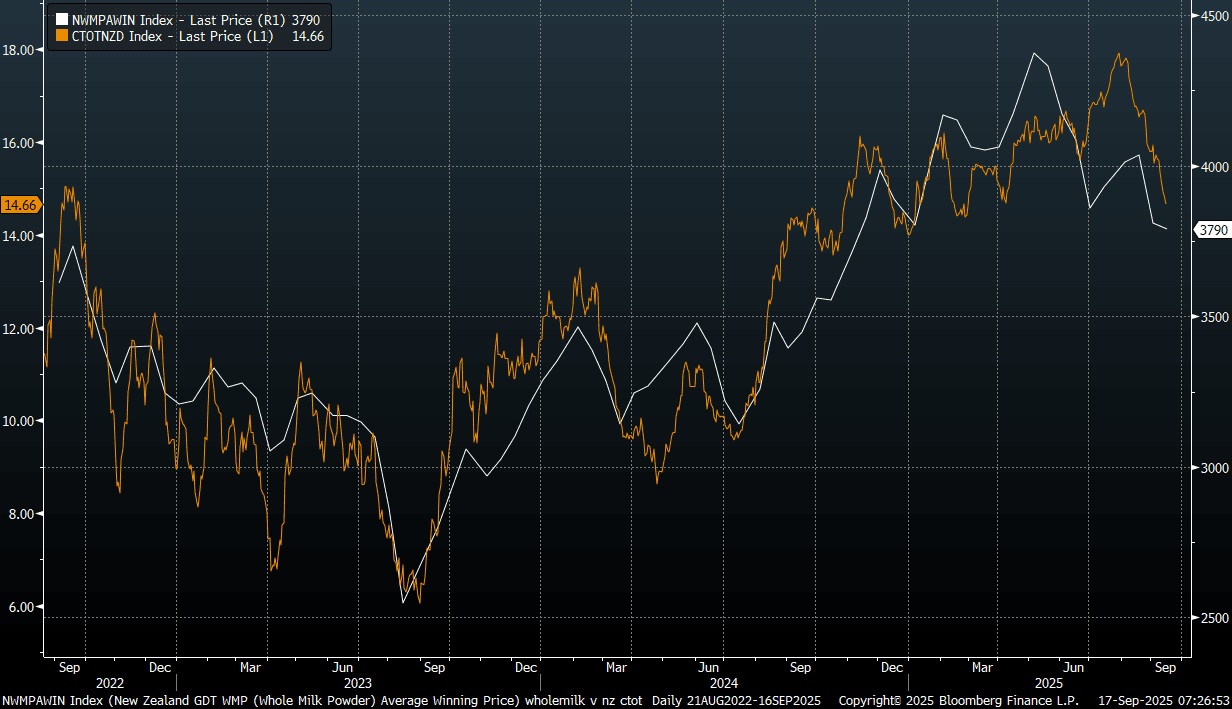

NEW ZEALAND: Whole Milk Price Auction Moderates Further

Overnight the fortnightly Global Dairy Trade auction saw the whole milk auction price dip a little further. We were off 0.8% versus the prior auction result. The chart below plots this series against the Citi terms of trade proxy for NZ.

- We are now comfortably off 2025 highs for whole milk prices (off 13.35% from May highs, and back to around flat for the year), with the terms of trade proxy down as well. We remain above longer term averages though.

- Today we get a broader update on NZ's external position with the Q2 current account, while tomorrow delivers Q2 GDP.

Fig 1: GDT Whole Milk Auction Price And Citi NZ ToT

Source: Citi/Bloomberg Finance L.P./MNI