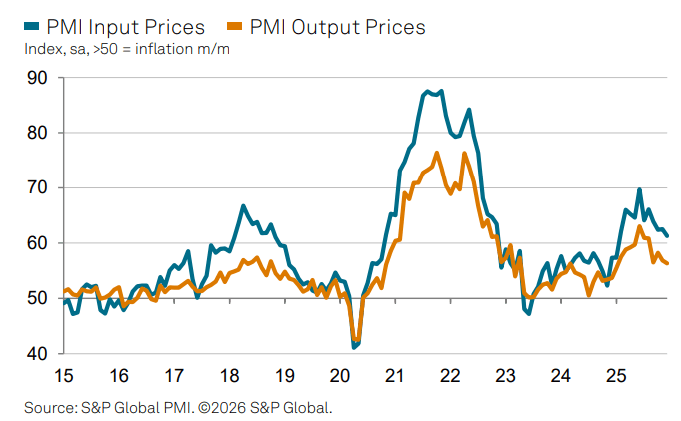

US DATA: Rise In Manufacturing PMI Activity (And Prices) Moderated At Year-End

The final December S&P Global Manufacturing PMI was unchanged from the flash reading of 51.8, confirming a 5-month low for the index (52.2 Nov). In turn, the details of the report confirmed the flash data in portraying a broad-based softening amid overall growth in manufacturing (S&P Global describes it as "a sustained, albeit slower, improvement in US manufacturing sector operating conditions") with inflation remaining elevated but diminishing from the acute pressures seen earlier in the year. Notably, job creation was portrayed as solid amid optimism over conditions in 2026.

Some highlights from the report:

- On activity: "Weaker growth emanated from a contraction in new order intakes....Exports were also a source of demand weakness, falling for the seventh successive month....A reduction in demand led to weaker output gains in December, the softest in three months...production increased sufficiently for firms to continued adding to their stocks of finished goods for the fifth month in a row...Work outstanding declined for the fourth month in a row during December, partly due to an expansion in labor capacity."

- On employment: "firms reported that employment growth was sustained into the end of 2025, with job creation reaching the most pronounced since August...firms filled vacancies in anticipation of a stronger 2026."

- On inflation: "Tariffs continued to push up input prices during December, with vendors reportedly raising charges. Although input cost inflation weakened since November to an 11-month low, it remained historically elevated. Similarly, manufacturers also recorded their least pronounced uplift in charges since the start of 2025, but inflation was again comfortably above trend."

- On the outlook: "manufacturing firms held a positive outlook regarding the year ahead for sales and production" though "the degree of confidence eased since November amid a lack of new work to replace existing orders and the ongoing uncertainty over tariffs and trade policy."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-S&P Global Services/Composite PMI React

- Little reaction in Treasuries after modest decline in S&P Global Services/Composite PMI data.

- Near early morning highs, TYH6 trades 113-03.5 (+7) vs. 113-07 high, still south of initial technical resistance at 113-11/22+ High Dec 1 / High Nov 25.

- Curves mildly steeper: 2s10s +.155 at 57.596, 5s30s +1.570 at 110.437.

- Next up: SM Services data at 1000ET.

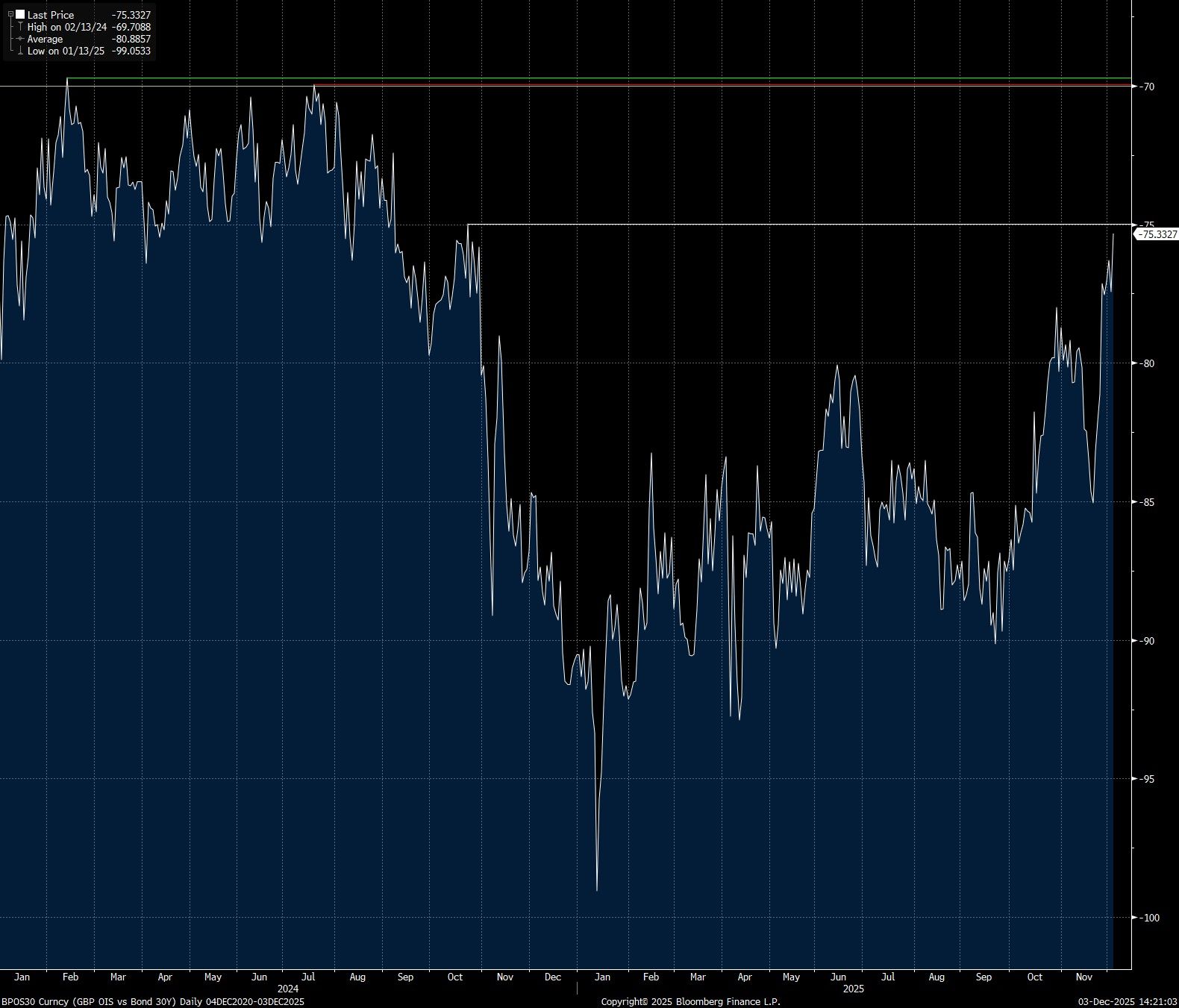

SWAPS: Long End Gilts Continue To Outperform Swaps

Long end UK swap spreads have widened further this week, even with 30-Year gilt yields little changed since the market close that followed the Budget.

- This points to a consistent post-Budget reduction in UK fiscal risk premium, with the 30-Year swap spread nearing the October ‘24 closing high (-74.99bp).

- While medium-term fiscal risks remain evident (with a particular focus on the backloaded nature of the fiscal tightening outlined in the Budget) the market has welcomed the (questionable) increase in fiscal headroom and ongoing WAM reduction in issuance, promoting swap spread widening.

- 30-Year swap spreads have rallied by ~10bp since the November 20 close, a break of the aforementioned October ’24 high would switch focus to the clustered resistance area at -70bp/-69.96bp and -69.71bp.

- It seems that a fresh gilt-negative catalyst is a pre-requisite for any fresh spread narrowing at this point e.g. slower-than-envisaged UK growth, political unrest or fresh questions surrounding the UK fiscal outlook.

Fig. 1: UK 30-Year Swap Spread (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

MNI: US NOV FINAL SERV PMI 54.1 (55.0 FLASH, 54.8 OCT)

- MNI: US NOV FINAL SERV PMI 54.1 (55.0 FLASH, 54.8 OCT)

- US NOV FINAL COMP PMI 54.2 (54.8 FLASH, 54.6 OCT)