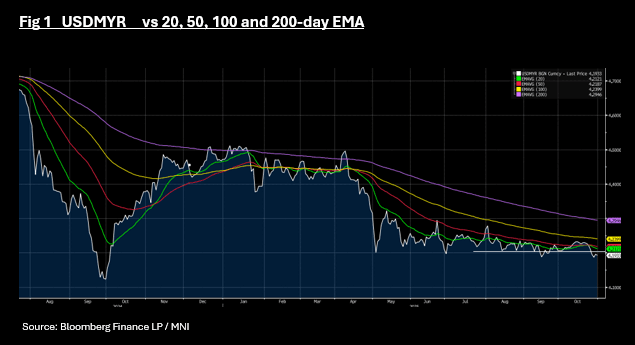

MYR: Ringgit Delivers Steady Gains, New Lows in Place

Oct-31 02:48

- Following various announcements from Korea this week, specifically a US China trade deal, USDMYR reached new lows for the year of 4.1875.

- Despite backing up a little from that low, the Ringgit has gained -0.70% for the week; consolidating below a key resistance level.

- The rally on Wednesday took USDMYR below 4.2040; a level it had tested and failed to hold below six times since August.

- It has little technical support below here, with September 2024 lows of 4.1235.

- Next week the BNM decides on rates and given the strength of the 3Q GDP release and other various data, markets are not pricing in any move from the Central Bank. This could be the catalyst for further gains for the Ringgit.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Holding Cheaper, Market Continues To Price Out RBA Cut

Oct-01 01:48

ACGBs (YM -4.0 & XM -5.5) remain weaker.

- S&P Global PMI Manufacturing Index falls to 51.4 from 53 in Aug.

- Cash US tsys are slightly cheaper in today's Asia-Pac session after yesterday's modest twist-steepener.

- Cash ACGBs are 4-7bps cheaper with the AU-US 10-year yield differential at +22bps.

- The latest ACGB Dec-34 supply achieved a weighted average yield that printed 0.40bp through prevailing mids (per Yieldbroker). However, the cover ratio decreased to 2.1033x, thelowest since its debut in 2023, from 3.1708x.

- The bills strip is -4 to -6 beyond the first contract.

- RBA-dated OIS pricing has firmed modestly across meetings following yesterday’s RBA Policy Decision. Pricing across meetings is 1-4bps firmer than yesterday’s pre-RBA levels. Notably, this post-RBA move leaves pricing some 10-19bps firmer than last Wednesday’s pre-CPI levels.

- A 25bp rate cut in October is given a 35% probability, with a cumulative 11bps of easing priced by year-end.

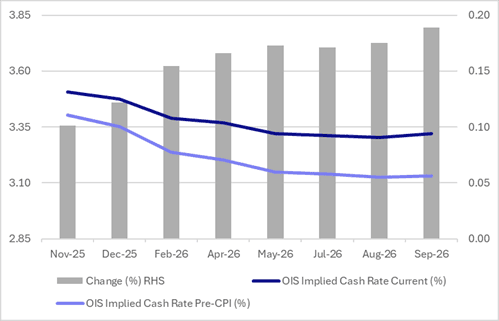

STIR: RBA Dated OIS’ Firming Since August CPI Extends After RBA Decision

Oct-01 01:34

RBA-dated OIS pricing has firmed modestly across meetings following yesterday’s RBA Policy Decision.

- At the time of writing, pricing across meetings was 1-4bps firmer than yesterday’s pre-RBA levels.

- Notably, this post-RBA move leaves pricing some 10-19bps firmer than last Wednesday’s pre-CPI levels.

- A 25bp rate cut in October is given a 35% probability, with a cumulative 11bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI

Source: Bloomberg Finance LP / MNI

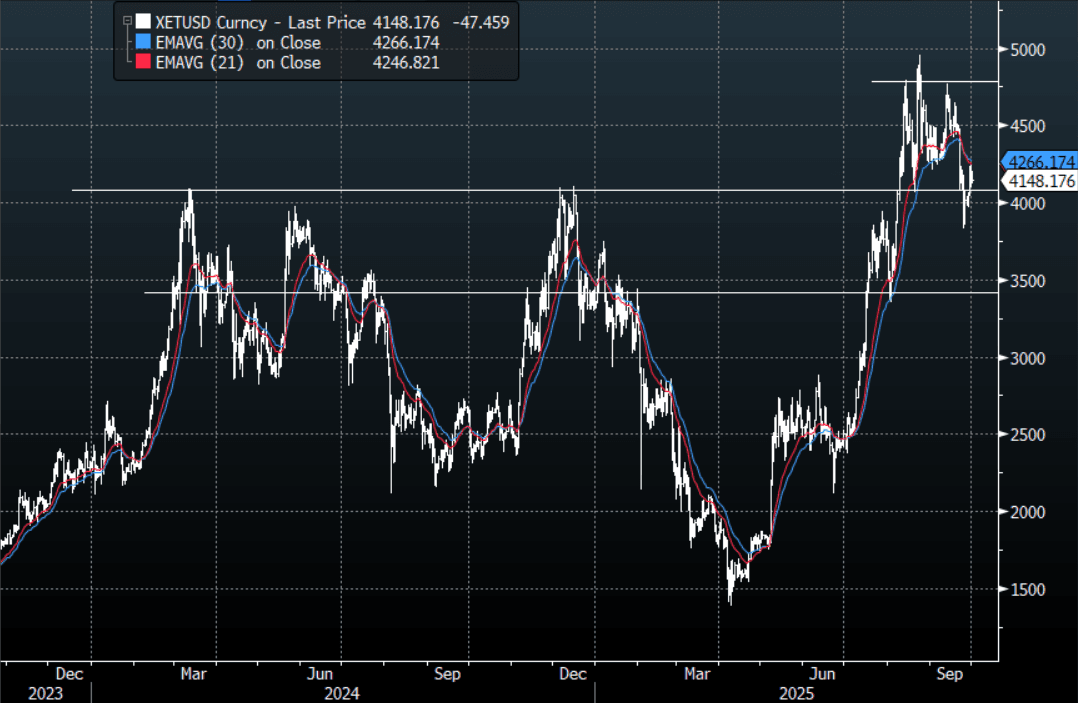

CRYPTO: Ethereum - Bounces, Technically $4300-$4500 To Be Faded First Up

Oct-01 01:24

Ethereum had a range overnight of $4093.19 - $4208.98, Asia is trading around $4152, -1.05%. Ethereum had a decent bounce after triggering stop losses sub $4000 last week. Having broken big support around $4100, technically rallies should now be faded initially. The first sell zone is now back towards the $4300/$4500 area.

- Menthor Q on X: "Crypto asset flows. "Digital asset investment products saw US$812m in outflows last week, though YTD inflows remain robust at US$39.6bn, close to last year’s record ... Bitcoin (-US$719m) and Ethereum (-US$409m) faced pressure, while Solana (+US$291m) attracted strong inflows.”

- Milk Road on X: “For a decade, crypto has moved in 2yr up / 2yr down cycles, pointing to a 2025 peak. But the data just shifted. PMI, liquidity, and analysts all say the cycle hasn’t ended, it’s been extended. The top now looks more like 2026… or later”

- “FTX will release $1.6B in stablecoins to creditors today. That’s $1.6B in fresh liquidity about to hit the crypto markets. Fresh powder is on the way.”

Fig 1: Ethereum spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P