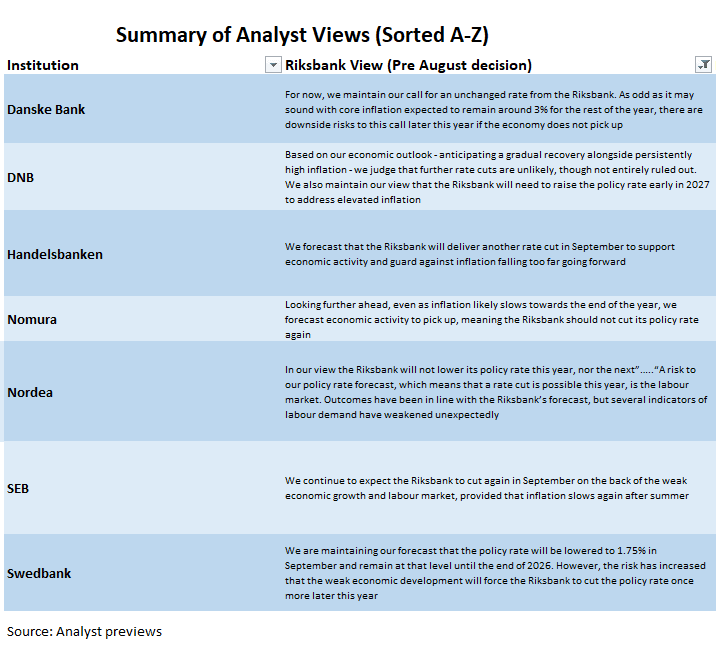

RIKSBANK: Riksbank Expected To Hold Next Week, Leaving Focus On Guidance

The Riksbank decision is due next Wednesday, with analysts and markets overwhelmingly favouring a hold at 2.00%. That will leave focus on the policy statement guidance, with no MPR/rate path due (only a concise Monetary Policy Update). After cutting rates in June, the Riksbank’s MPR rate path entailed “some probability of another cut this year”, because “the outlook for inflation and economic activity suggests some easing of monetary policy”.

- Heading into the August decision, the Board will need to weigh higher-than-expected spot inflation pressures against continued weakness in the labour market and activity data. The large upward inflation surprise in June, which was mostly consolidated in July, should guard against a surprise rate move.

- However, the Riksbank is sensitive to economic activity (particularly household consumption) and has demonstrated a willingness to lend support with monetary easing already this year. This dovish bias will likely be reaffirmed if the Board views the recent Summer inflation uptick as temporary.

- Based on the seven previews we have seen so far, most analysts expect the August policy statement to retain a similar dovish leaning to June, with the latest rate path signals likely to be confirmed. More pointed guidance towards a September cut would be a dovish surprise.

- However, four of the analyst previews we have seen expect no further cuts this cycle, while the remaining three expect a final 25bp cut in September.

- We will update these views, alongside MNI’s usual analysis, in our preview early next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

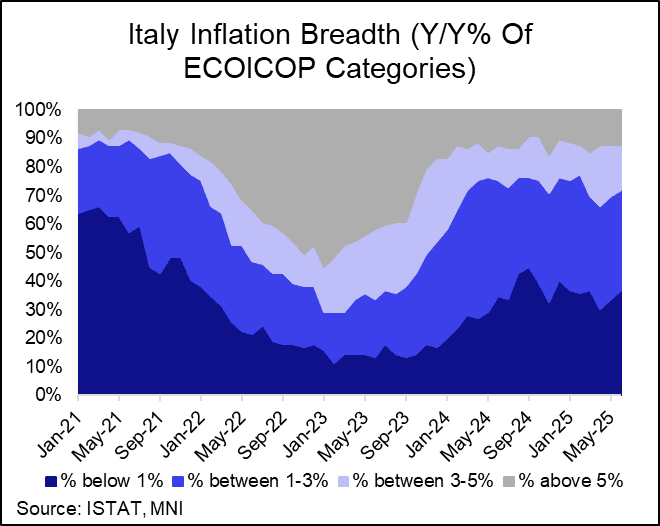

EUROPEAN INFLATION: Energy Drives Upward Revision To Italian June HICP

Italian final June HICP was revised up a tenth on a rounded basis to 1.8% Y/Y (vs 1.7% in May). Energy inflation was revised up three tenths to -2.1% Y/Y (vs -1.9% in May), while services was revised up a tenth to 3.0% Y/Y (vs 2.9% in May). This was mostly offset by a three tenth downward revision to processed food inflation to 2.8% Y/Y (vs 2.8% in May). Non-energy industrial goods was unrevised at 0.5% Y/Y (vs 0.4% in May), as was unprocessed foods at 4.5% Y/Y (vs 3.9% in May).

- Within services, there were accelerations in the restaurant and hotels, recreation and culture and transport services components.

- Package holidays rose 7.5% Y/Y (vs 6.3% prior), which was partially offset by a pullback in recreation and cultural services inflation (5.5% Y/Y vs 6.6% prior).

- Airfares inflation decelerated to 2.9% Y/Y (vs 4.6% prior). Although airfares rose 9% M/M on an NSA sequential basis in June, this was below last year’s reading and also some of the analyst expectations we had seen. As such, the rise in transport services was due to non-airfare (i.e. less volatile) components.

- Communication services were 0.5% Y/Y (vs 0.6% prior), while miscellaneous services were steady at 1.9% Y/Y. A pullback in insurance inflation was offset by a rise in personal care.

- Core goods inflation trends remain subdued – as is also seen in the broader Eurozone basket. In June, there was a small uptick in clothing and household appliance inflation, offset by a pullback in household textiles.

- The proportion of HICP sub-components with inflation rates between 1-3% Y/Y was steady at 35% (vs 36% prior).

FOREX: GBP Consolidating Most Recent Weakness, UK Labour Market Data Thursday

- This morning’s higher-than-expected UK CPI readings have been shrugged off by the pound, as markets await labour market data on Thursday and assess the ongoing fiscal concerns for the UK economy. GBPUSD’s post data advance was contained to a 20 pip rally to 1.3417 before then oscillating either side of 1.3400.

- Technical considerations are likely helping cable consolidate its most recent weakness. Following a clean break of the 50-day EMA, spot subsequently breached important trendline support (drawn from the Jan 13 low) below 1.3430 yesterday, which has helped cap the topside today. Developments strengthen a bearish threat, and the next immediate focus is on 1.3371, the Jun 23 low and a key short-term support. Below here, attention will be on 1.3335 and 1.3245, the May 20 & 19 lows respectively.

- In similar vein, a bullish condition in EURGBP remains intact and fresh 3-month highs this week maintain the price sequence of higher highs and higher lows, highlighting a dominant uptrend. Scope is seen for a climb towards key resistance at 0.8738, the Apr 11 high.

- Tomorrow’s labour market data takes on increased significance following BoE's Bailey flagging the MPC's potential responsiveness to further jobs declines in his interview with The Times this weekend. We previewed the data fully here: https://mni.marketnews.com/4eQADLZ

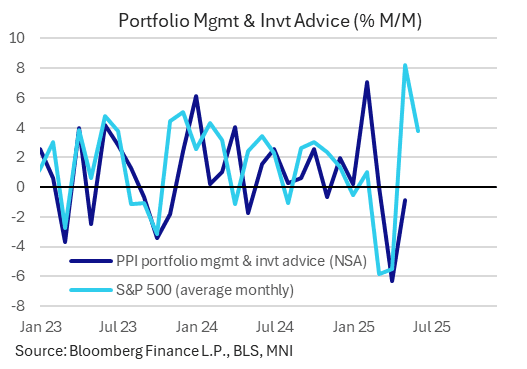

US OUTLOOK/OPINION: Solid Core PCE Estimates With PPI Portfolio Rebound Eyed

- Adding a few more names to yesterday’s round up of core PCE analyst estimates ahead of today’s PPI details, the average estimate still sits at 0.31% M/M in June after 0.18% M/M in May. This lifted from closer to 0.25% prior to CPI.

- Core PCE estimates for June: JPM 0.28, TDS 0.28%, Barclays 0.29%, GS 0.29%, Citi 0.32%, UBS 0.32%, BofA 0.34%, MS 0.35% and Nomura 0.35%.

- A reminder that there are many, mostly services-related, components that feed into core PCE from PPI, with medical care, airfares and in particular portfolio management & investment advice again receiving attention this month.

- Also expect continued growing focus on the broader core PPI categories for cost pressure implications.

- Portfolio management & investment advice: It fell -0.8% M/M in May following swings in recent months of -6.3% in Apr, a flat Mar and +7.1% in Feb on equity market volatility.

- Lags in the series suggest that strong increases in equity markets in May and early June should feed through into this month’s June report, and continue to boost it ahead judging by equity gains since June onwards.

- Citi eye a ~2.5% rebound in portfolio management fees (but note that it “should not be concerning to Fed officials after three sub-target monthly annualized readings”) whilst Nomura look for a 4.3% M/M increase in portfolio management & investment advice.

- Jefferies, explicitly talking about portfolio management, a large subset of portfolio management & investment advice which has seen -7.1% in Apr, flat Mar and +8.1% in Feb, expect it to “contribute significantly to PPI this time around” on the resulting increase in AUM with “markets rebounding to near-record highs in June”.

- Weighing 1.7% of core PCE, it dragged -0.01pp from M/M core PCE inflation in May after a heavy -0.11pp in April. A 3% M/M increase in June, meeting somewhere between the Citi and Nomura estimates, who are both a little above the median for core PCE, would add roughly 0.05pps to core PCE.