US TSYS: Richer In Asia

TYM3 deals at 116-18+ unchanged from Wednesday's settlement level, a touch off the top of the observed 0-08 range on volume of ~77k.

- Cash tsys sit 1.5-4bps richer across the major benchmarks, the curve has bull steepened.

- Tsys were marginally firmer in early dealing as Asia-Pac participants reacted to the softer than expected US data on Wednesday.

- Firmer than forecast Caixin services PMI saw the bid moderately extend. Lower WTI futures, down ~0.7%, and US Equity futures, e-minis sit ~0.3% softer, also added a level of support.

- Pockets of screen buyers in FV and TY saw tsys marginally extend gains late in the Asian session. There was no headline catalyst observed on the move.

- In Europe today Swiss unemployment and German Industrial Production headline. Further out we have initial jobless claims and Fedspeak from St Louis Fed President Bullard will cross.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

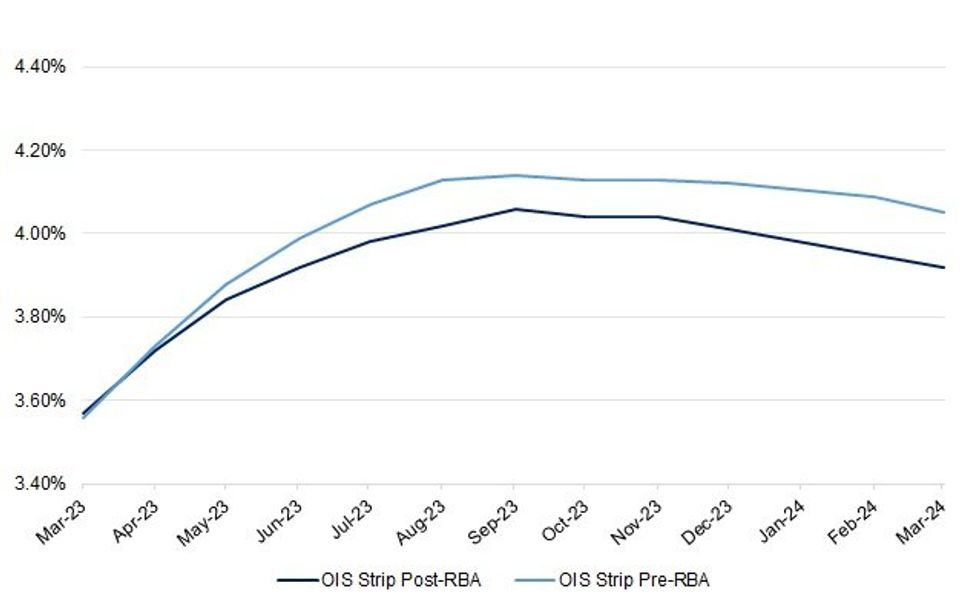

STIR: RBA-Dated OIS Settles Lower On Guidance Tweak, Further Aided By Inflation & Wage Rhetoric

| OIS Strip Post-RBA | OIS Strip Pre-RBA | Change (bp) | |

| Mar-23 | 3.57% | 3.56% | +1 |

| Apr-23 | 3.72% | 3.73% | -1 |

| May-23 | 3.84% | 3.88% | -4 |

| Jun-23 | 3.92% | 3.99% | -7 |

| Jul-23 | 3.98% | 4.07% | -9 |

| Aug-23 | 4.02% | 4.13% | -11 |

| Sep-23 | 4.06% | 4.14% | -8 |

| Oct-23 | 4.04% | 4.13% | -9 |

| Nov-23 | 4.04% | 4.13% | -9 |

| Dec-23 | 4.01% | 4.12% | -11 |

| Feb-24 | 3.95% | 4.09% | -14 |

| Mar-24 | 3.92% | 4.05% | -13 |

AUSSIE BONDS: Westpac Flesh Out The Post-RBA Landscape

Westpac write “the rates and bond markets were relatively quiet ahead of the RBA meeting, with price action largely consolidating the overnight changes. However, that all changed after the hike with the market focusing on the shift away from “increases” over the “months ahead” to merely the Board “expects that further tightening of monetary policy will be needed”.”

- “We suspect that most of these initial shifts have further to run given the significant shift in the Governor’s language and the view that the “monthly CPI indicator suggests that inflation has peaked in Australia.” There is a real sense that the Board is very close to pausing, perhaps even as early as next month. So, the concept of further hikes being a meeting-by-meeting proposition will remain central to the trading rhythm and risk reward assessment around future data releases. This will push the AU/U.S. 10-Year spread even further inverse, with the tactical level in which to re-enter narrowers now around -15bp. We also expect the curve (3/10-Year futures spread) to steepen back up to the 40bp level over coming weeks.”

US TSYS: Modest RBA-Related Bid Unwound, Tight Ranges Prevail

Tsys nudged richer in lieu of the latest RBA decision, albeit comfortably underperforming ACGBs, with the latter benefitting from the dovish feel to the RBA’s latest post-meeting statement, which was delivered alongside the widely expected 25bp rate hike. Tsys now operate shy of best levels, with the major cash benchmarks running flat to 1bp richer, while TYM3 is +0-04 at 111-03+, 0-02+ off the peak of its narrow 0-06 range.