US PREVIEW: Revisions In Focus For This Morning's GDP/Core PCE/Claims Data

Sep-25 11:40

In a busy 0830ET slot for data releases, revisions could be the most closely-eyed aspect:

- GDP/PCE: We get the third release for Q2 national accounts covering GDP and PCE amongst other components (GDP is seen unrevised at 3.3% Q/Q SAAR). Note as well that this release comes with the BEA's annual update, which rather than just altering the prior quarter will see changes going back to 1Q20. That should see greater focus on a third release than would usually be the case, including when it comes to the recent core PCE profile.

- Previous editions have led to fairly meaningful revisions in core PCE, with various factors being incorporated including new seasonal adjustments, and CPI / PPI historic series revisions. It's difficult to estimate what the revisions will be, and as such difficult to gauge consensus for the impact: Nomura writes that "Available data point to revisions of -5bp to +4bp in monthly core PCE inflation due to annual revisions, resulting in an upward revision of around 10bp to y-o-y core PCE inflation". In short, they write, the revisions "have the potential to materially change the monthly profile of core PCE".

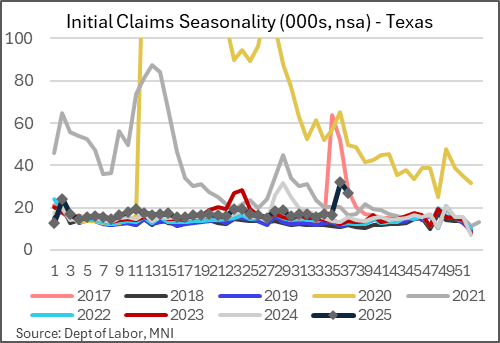

- Jobless Claims: Initial claims are seen at 233k in the Sep 20 week (up 2k) with continuing at 1,932k in the Sep 13 week (up 12k). It's hardly certain but we may get revisions to recent weekly claims data, specifically going back three weeks to Sept 1. That's due to the Texas claims spike which the local authorities have confirmed is the result of fraud. Recall it took 3 weeks after a similar fraud was reported by in Massachusetts that had affected figures in 2023 before we got (significant) revisions.

- Texas initial claims were most recently reported at 26.9k (-5.0k on the week) having spiked 15.3k to 31.95k (initially reported as 31.91k) the previous week compared to a recent trend in the 16-18k mark. Taking that prior trend as a counterfactual, it very crudely implies about 10-15k of impact from fraud.

- Other data at 0830ET includes August advance goods trade balance, alongside inventories and durable goods data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Gilt Bear Remain In The Driver's Seat

Aug-26 11:30

- In the FI space, Bund futures are unchanged and remain above their recent lows. A bear threat is present. The contract recently breached 128.84, the Jul 25 low. Note that 129.00 represents the base of a broad range. A clear range breakout would strengthen a bearish theme. This would open 128.40 initially, the Apr 9 low. Strength above the 50-day EMA of 129.80, is required to signal a reversal. Resistance at the 20-day EMA is at 129.51.

- A bear cycle in Gilt futures remains in play. Note that on the continuation chart, moving average studies are in a bear-mode position, highlighting a clear downtrend - for now. First support to watch is 90.31, the Aug 22 low. It has been pierced, a clear break would resume the bear leg and open the 90.00 handle. Initial resistance is at 91.24, the Aug 18 high.

EGB SYNDICATION: Austria New 7-Year RAGB: Allocations Out

Aug-26 11:19

- E3bln WNG (excl. E250mln issuer retention) of the new 7-year Sep-32 RAGB

- Spread set earlier at MS+30 (guidance was MS+33 area)

- Books closed in excess of EUR 19bn, including EUR 1.8bn JLM interest

- Format: Reg S, Bearer, 144A eligible, CAC

- Settlement: 02 September 2025 (T+5)

- Maturity: 20 September 2032 (7Y)

- Coupon: TBD, Fixed, Ann., ACT/ACT (Long 1st to 20 September 2026)

- ISIN: AT0000A3NY15

- Bookrunners: BofA / DB(DM/B&D) / Erste Group / HSBC / JPM / Raiffeisen Bank International

- DB=DM/B&D. HR 103% vs DBR 1.7 08/15/32

- Hedge deadline 13.40CET / 12.40UKT

From market source

ESM ISSUANCE: USD2bln WNG New 5-Year: Mandate

Aug-26 11:14

- USD2bln WNG of the new 5-year Sep-30 ESM-Bond

- IPT: MS + 42 bps area (equiv. to CT5 + ~7.3bp)

- Issuer: European Stability Mechanism (TICKER: ESM)

- Issuer Ratings: Aaa (stable) (Moody's) / AAA (stable) (S&P) / AAA (stable) (Fitch)/ AAA (stable) (Scope)

- Format: Registered Notes, Reg S (NSS) / 144A

- Ranking: Senior, Unsecured, Unsubordinated

- Settlement: 4 September 2025 (T+6 (TARGET) / T+5 (NY))

- Maturity Date: 4 September 2030 (5Y)

- Coupon: Fixed, Semi-annual, 30/360, Following, Unadjusted

- Bookrunners: CACIB(DM/B&D) / DB / JPM

- Timing: Taking IOIs today, expect to price tomorrow

From market source.

USD3bln of an ESM USD Bond will mature on September 10. That line was a 5-year issue also initially.