USDCAD TECHS: Reversal Extends

Jan-23 15:18

* RES 4: 1.4023 76.4% retracement of the Nov 5 - Dec 26 bear leg * RES 3: 1.3977 High Dec 4 * RES 2:...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

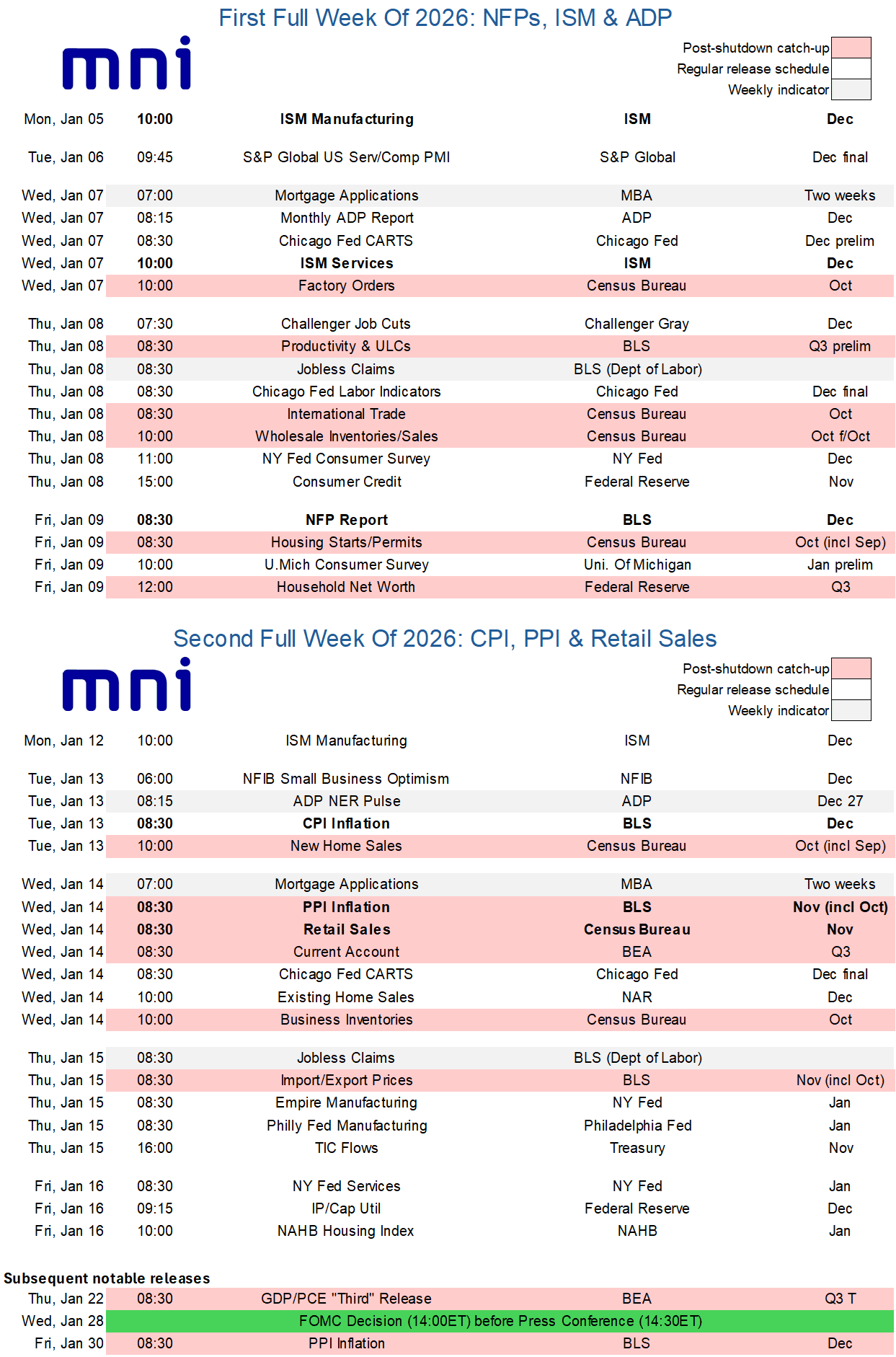

LOOK AHEAD: A Busy, and Key, First Half Of January For US Data

Dec-24 15:18

- The first two full weeks of the year see nonfarm payrolls and CPI reports for December with those two key reports back on their original schedules having been prioritized by the BLS.

- PPI and retail sales are also released but they’re still lagging and will only be for November (along with a full set of October details in the case for PPI). Note that PPI for December will then follow at the end of the month as the BLS continues to work on returning that report to its original schedule.

- Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7.

- These all build up to the FOMC meeting on Jan 27-28, which is currently seen with low odds of a fourth consecutive 25bp cut with just 3bp of cuts priced. The next cut is fully priced for the June meeting under a new Fed chair.

- Of the other main releases, we’re still waiting for new release dates for monthly PCE (Nov originally scheduled for Dec 19 and Dec for Jan 29), JOLTS (originally set for Jan 7) and the advance release for Q4 GDP (originally Jan 29).

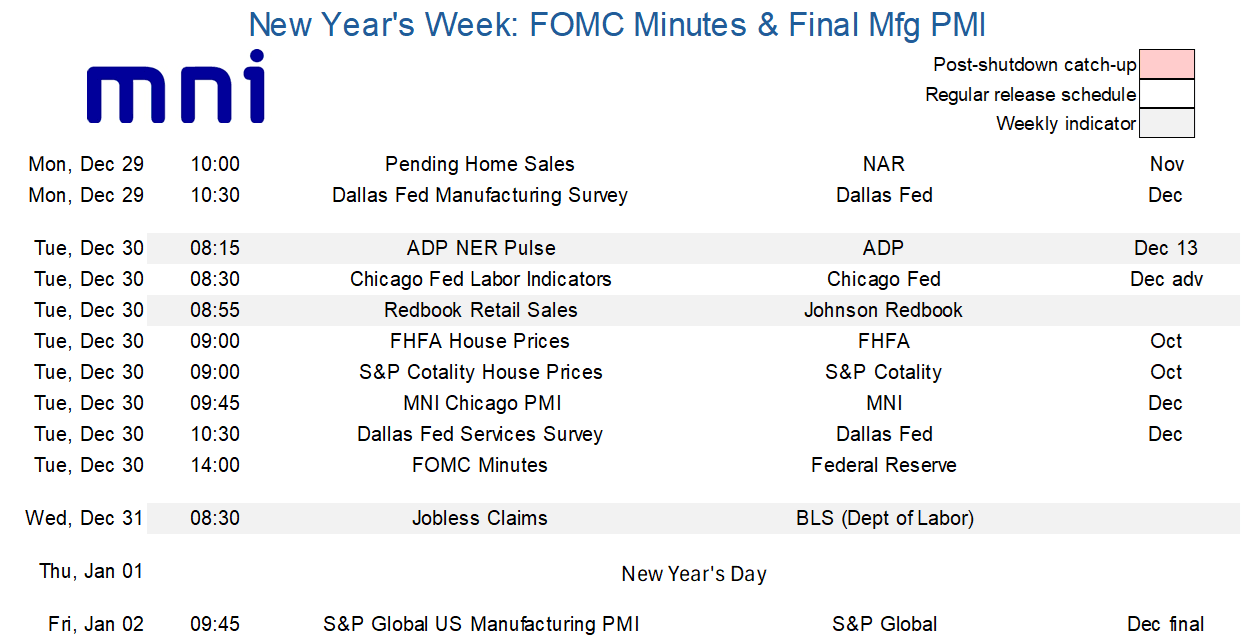

LOOK AHEAD: Highlights of Next Week’s US Data Schedule

Dec-24 15:15

- Weekly labor: the ADP NER Pulse (Tuesday) runs up to Dec 13 and so starts to directly overlap the reference period for the monthly report due the week after. Jobless claims (Wednesday) meanwhile are a day early again and aside from offering a latest look at the health of the labor market will also give a better indication of continuing claims in the payrolls reference period.

- The MNI Chicago PMI (Tuesday) offers an alternative look at manufacturing activity ahead of the ISM manufacturing survey the following week and should be watched after sliding 7.5 points to 36.3 in November with a particularly large drop in new orders.

- The final manufacturing PMI (Friday) rounds the week off after the flash release saw it at 51.8 after 52.2 for a five-month low. From the press release: “Production growth dipped to a three-month low as new

- orders fell for the first time since December 2024.”

- Away from data, the FOMC minutes from the Dec 9-10 meeting will be interesting (Tuesday). Powell delivered a not-so-hawkish 25bp cut but with signs of a still clearly divided committee whilst we watch for discussions around changes in administered rates.

- Powell on the perceived differences in the risks to the outlook on the FOMC: “"The risk is that tariff inflation just turns out to be more and more persistent... I think the other possibility is, less likely, and that is just that the labor market gets tight, or the economy gets tight. And you see, just traditional inflation. I don't see that as particularly likely, but ... again, all across the Committee, people see the picture pretty similarly, but see the risks quite differently. And some people do see the inflation risk. And I wouldn't dismiss that case. But you've got to make an assessment, and this is the assessment."

US TSYS/SUPPLY: Early 7Y Note Auction Preview

Dec-24 15:07

Tsy $44B 7Y Note auction (91282CPQ8) scheduled earlier than normal at 1130ET due to today's early Christmas eve close (1300ET). WI is currently running around 3.939%, 15.8bp cheap vs. last month's tail. Currently, Mar'26 10Y futures trade +1 at 112-10.5.

- November auction recap: Treasuries showed little reaction after the $44B 7Y note auction (91282CPM7) tailed: 3.781% high yield vs. WI of 3.777%; bid-to-cover steady at 2.46x.

- Peripheral stats: Indirect take-up slipped to 56.65% vs. 59.0% prior; Direct take-up rose to 30.27% vs. 27.8% prior; while Dealers took 13.07% vs. 13.1% prior.