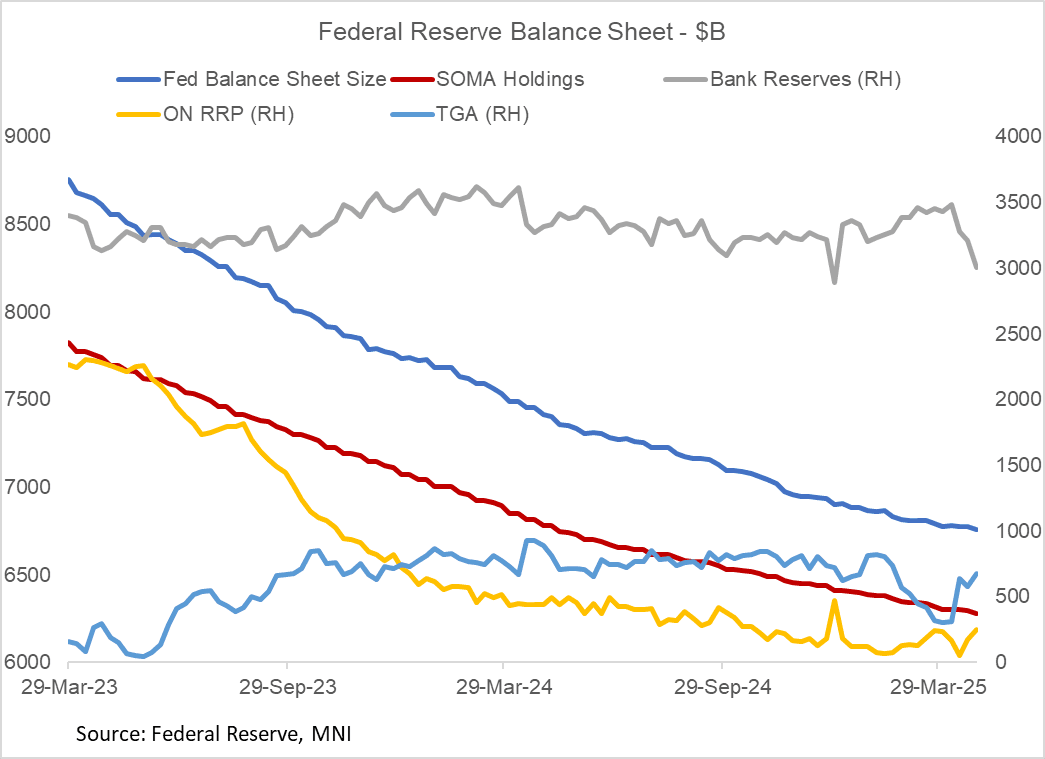

FED: Reserves Continued To Pull Back Amid Treasury Tax Collection (2/2)

Reserves continued their pullback in the latest week, dropping a further $209B to almost exactly $3T. That's the lowest level since the turn of the year, and one of the lowest in the last few years.

- Reserves have dropped $427B over the past month, as Treasury cash in the TGA has grown $376B (while reverse repo takeup has risen by $31B, with the ON RRP facility size growing by $79B in the latest week amid month-end dynamics).

- Reserves are looking a little on the low side for the Fed's comfort, but this is a fairly predictable drop and they should be near their lowest point in the near-term with the key tax collections of April at an end. As Treasury spends down cash as it waits for an end to the debt limit over the coming months, reserves should build back up, likely starting next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NZD: Firmer Thanks To Higher Equities, But Markets Await Tariff Announcement

NZD/USD tracks near 0.5700 in early Wednesday dealings. The Kiwi was up 0.40% for Tuesday's session, with most of the gains seen during US trade. The currency slightly lagged other commodity FX with AUD and CAD up 0.50-0.60% respectively. EUR finished down slightly, while USD indices were little changed. Aggregate FX moves weren't large as markets await the reciprocal tariff announcement in the afternoon US Wednesday time.

- For NZD/USD technicals, end March lows were just under 0.5650, while topside focus could rest at the 50-day EMA (near 0.5715) and the 100-day (just under 0.5760).

- Higher beta/commodity FX received some support in Tuesday trade amid a better global equity tone. The Euro Stoxx rose 1.37%, while the SPX gained 0.38%. US yields mostly stayed on the backfoot, the 10yr Tsy yield just under 4.17%. Recent lows in early March were at 4.10%. US data was mixed but mostly on the softer side relative to forecasts, with the headline ISM remaining sub 50.0.

- NZ-US 2yr swap spreads are holding just off recent highs, last near -47bps.

- Overnight we had the whole milk powder auction, which rose to $4062 from $4052. We remain elevated but just off Feb highs.

- Coming up shortly there is Feb building permits for NZ.

ASIA: Government Bond Issuance Today.

- MAS to Sell S$15.9 Bn 28-Day Bills

- MAS to Sell S$1.5 Bn 249-Day Bills

- MAS to Sell S$22.9 Bn 83-Day Bills

- Vietnam To Sell VND 0.5Tln 2030 Bonds; (TD2530008)

- Vietnam To Sell VND 0.5Tln 2055 Bonds; (TD2555052)

- Vietnam To Sell VND 0.5Tln 2040 Bonds; (TD2540037)

- Vietnam To Sell VND 12.5Tln 2035 Bonds; (TD2535026)

- Philippines To Sell PHP 30.0Bln 2030 Bonds (PH0000057218*)

- China to Sell 170 Bn Yuan 2027 Bonds

- China to Sell 170 Bn Yuan 2035 Bonds

- Bank of Korea to Sell KRW2tn 2-Year Bonds

- South Korea to Sell KRW2tn 63-Day Financial Bills

- India to Sell INR50bn 182-Day Bills

- India to Sell INR90bn 91-Day Bills

- India to Sell INR50bn 364-Day Bills

AUD: A$ Outperforms On Better Equity Sentiment & Disappointing US Data

Aussie outperformed on Tuesday along with other risk-sensitive currencies given better equity sentiment and also the fall in the US dollar following softer-than-expected US manufacturing ISM and job vacancy data. AUDUSD had been tracking around 0.6250 before the data and then jumped to 0.6283 afterwards. It is now up 0.5% to 0.6278. The USD index fell 0.1%.

- Tuesday’s appreciation of the AUD against the US dollar was consistent with intraday weakness being corrective. A clear break of 0.6187, 4 February low, is needed to reinstate the bear threat, whereas clearance of 0.6409, 21 February high, is needed to strengthen the bull cycle. Initial support is at 0.6219 and resistance at 0.6331.

- The euro underperformed leaving AUDEUR up 0.7% to 0.5817, close to the intraday high. AUDGBP is 0.5% higher at 0.4858.

- While the yen and kiwi were both stronger against the greenback, they fell versus the Aussie. AUDNZD is up 0.1% to 1.1014. The pair trended higher following the RBA decision to a peak of 1.1032 but then moderated to around 1.1010. AUDJPY is 0.2% higher at 93.89 after a low of 93.15 during European trading.

- Equities were stronger with the S&P up 0.4% and Euro stoxx +1.4%. Oil prices fell with Brent down 0.5% to $74.41/bbl. Copper was little changed and iron ore is higher at around $104/t.

- Building approvals for February are released today and forecast to fall 1.3% m/m after rising 6.3%.