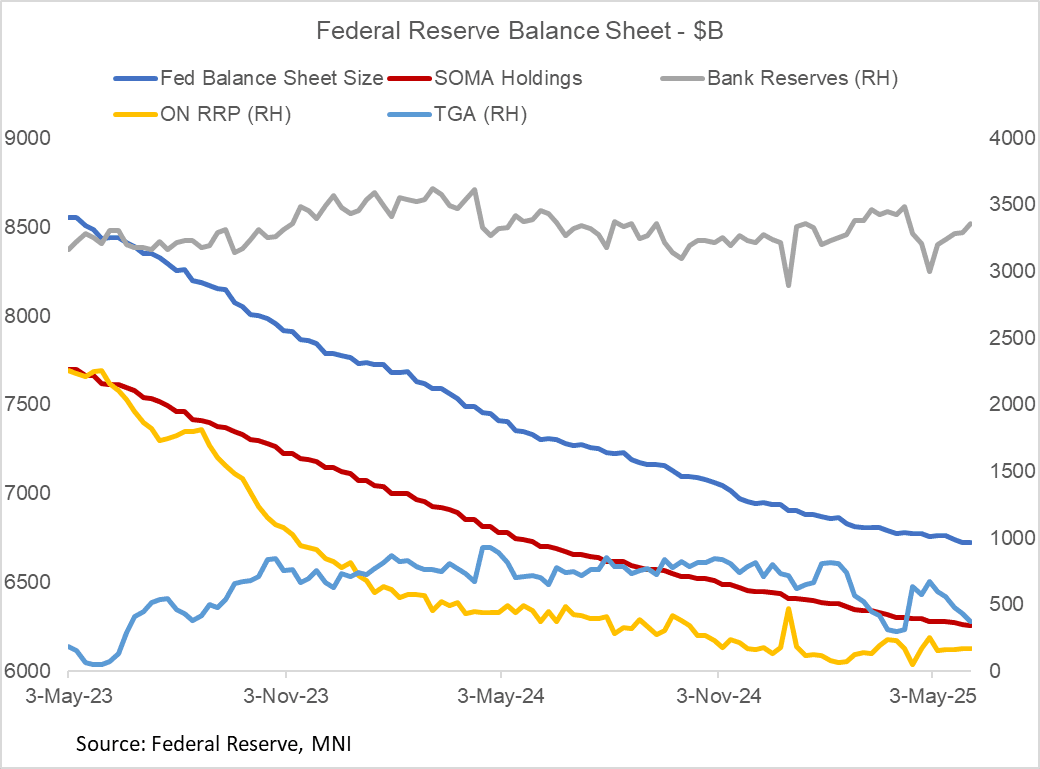

FED: Reserves At 8-Week High As Treasury Cash Dwindles (1/2)

Jun-05 20:44

Reserves rose for a 5th consecutive week in the week to Wednesday June 4, picking up $68B to $3.36T. That's a rise of $161B over the last 4 weeks to the highest since the week of April 9.

- This is the inverse to the Treasury General Account, which continues to drain after the large influx of tax cash in April. The TGA fell $61B to $376B, now down $220B over the last 4 weeks.

- Other categories of liabilities were little changed, with reverse repo takeup rising at month-end (Friday) but not recorded in the Wednesday levels.

- Reserves (which remain "abundant" by most accounts) probably don't have much further to run to the upside in the coming couple of weeks, with another key tax deadline coming in mid-June that will push up Treasury cash and lower reserves.

- However beyond that point attention will be increasingly paid to the dwindling Treasury cash pile into late summer, with a potential "x-date" approaching.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Southbound

May-06 20:00

- RES 4: 1.4415 High Apr 1

- RES 3: 1.4296 High Apr 7

- RES 2: 1.4066 50-day EMA

- RES 1: 1.3914 20-day EMA

- PRICE: 1.3781 @ 17:02 BST May 6

- SUP 1: 1.3760 Low May 2 and the bear trigger

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 2024

- SUP 4: 1.3643 Low Oct 9 ‘24

Bearish conditions in USDCAD remain intact. A fresh cycle low last Friday reinforces the bearish theme signalling scope for a continuation, near-term. Potential is seen for a move towards 1.3744, a Fibonacci retracement. Note that Moving average studies are in a bear mode position, highlighting a dominant downtrend. On the upside, first resistance to watch is 1.3914, the 20-day EMA.

US OUTLOOK/OPINION: Macro Since Last FOMC: Labor - Pessimistic Consumers [2/2]

May-06 19:44

- Some consumer expectations point to a particularly bleak outlook for the labor market over the next year. A question in the U.Mich survey for instance has shown two months now at its weakest since 2008/09.

- However, for now, initial jobless claims remain in a well-defined range and are still close to levels associated with a tight labor market. The nearest sign of potentially some softening in re-hiring activity was the latest increase in continuing claims to a fresh high since late 2021 but it’s just one week of data and should be interpreted carefully with potential Easter distortions.

- The next few months of data are likely to be more revealing.

US OUTLOOK/OPINION: Macro Since Last FOMC: Labor - Robust Payrolls Report [12]

May-06 19:42

- There have been two payrolls reports since the last FOMC meeting and both have been stronger than expected whilst also ruling out a material climb in the unemployment rate.

- Downward revisions have taken some of the gloss off payrolls growth in these March and April releases yet we’re left with a three-month average of 155k (177k in Apr, 185k in Mar and 102k in Feb). That’s comfortably firmer than long-run breakeven estimates closer to 100k, which should start to become more binding with tighter immigration policy under the second Trump administration.

- The breakdown of monthly payrolls growth in April shows one of general resilience, including strength in transportation & warehousing that shows no sign of adverse impacts from tariffs. Of course, this is still early for job losses to be showing up, especially with the pay period including April 12th being still close to the Apr 2 "Liberation Day" tariff announcements (before the partial backtracking on Apr 9) with companies still assessing how to respond under heightened uncertainty.

- However, accompanied with a further large increase in average weekly hours worked for transportation & warehousing, as well as retail and wholesale trade, it appears that prior tariff front-running and the surge in imports/build in inventories is helping boost jobs growth despite broader uncertainty.

- Similarly, the unemployment rate has only inched higher recently, from 4.14% in Feb to 4.15% in Mar and 4.19% in April, below a high of 4.23% back in November and versus a median FOMC forecast of 4.4% for 4Q25.