STIR: Repo Reference Rates

Jan-16 13:10

* Secured Overnight Financing Rate (SOFR): 3.66% (+0.02), volume: $3.201T * Broad General Collateral...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

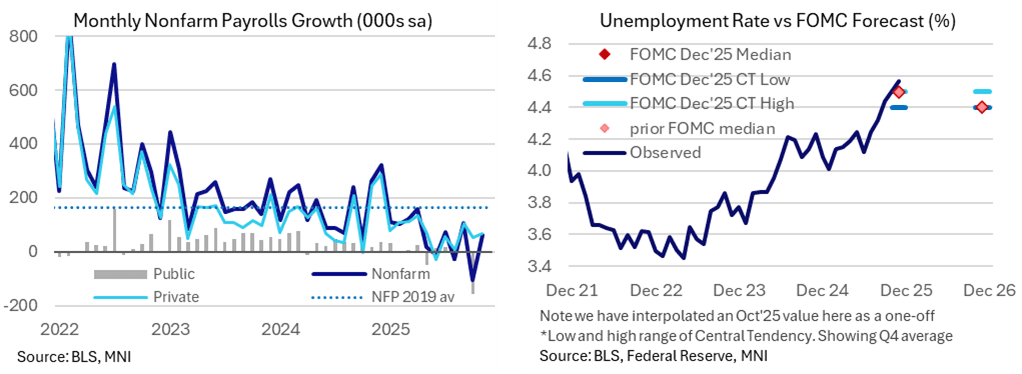

US LABOR MARKET: MNI US Employment Insight: Unemp Trends Higher, Caveats Abound

Dec-17 13:08

- We have published and e-mailed to subscribers the MNI US Employment Insight.

- Please find the full report including MNI analysis and analyst views: https://media.marketnews.com/US_Employment_Report_Dec2025_d56d8daa2e.pdf

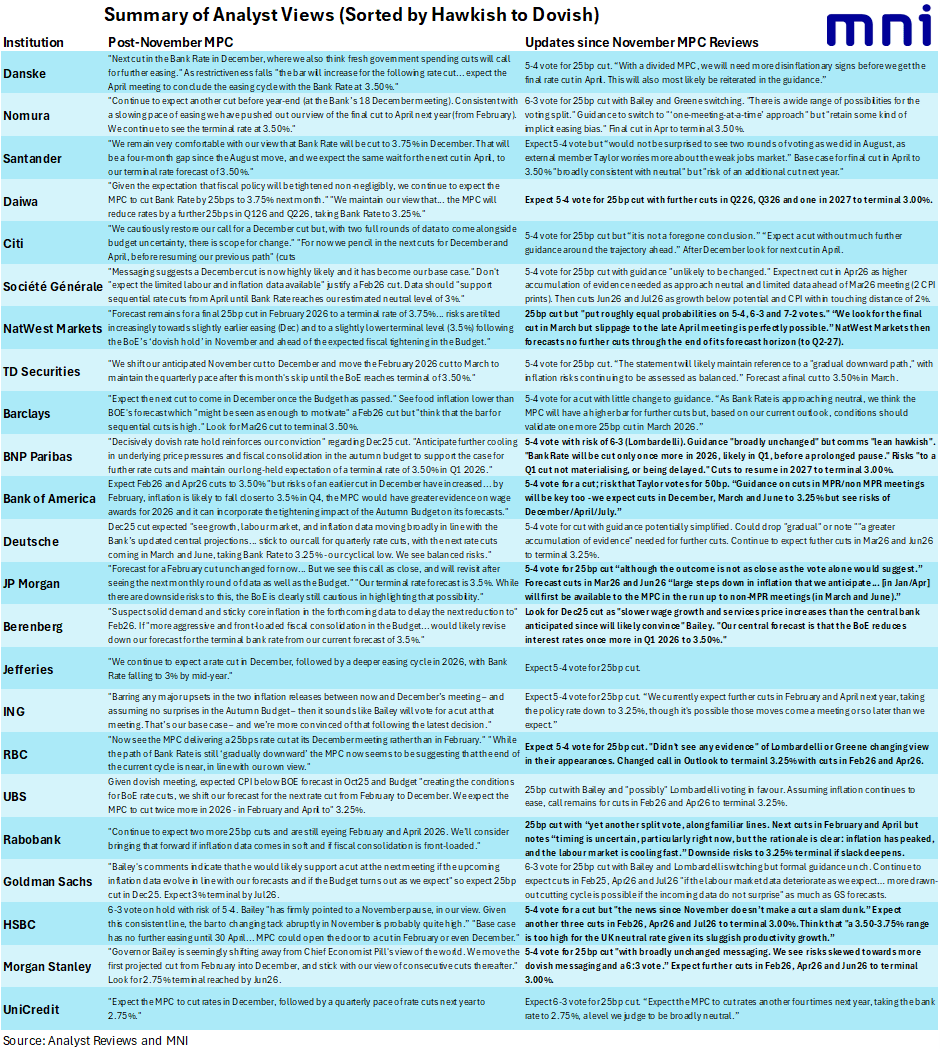

BOE: Summary of Analyst Views (2/2)

Dec-17 12:47

- Most expect guidance to remain unchanged from November. There are some arguing that “gradual” may be removed – most notably Deutsche Bank – but this is definitely not the consensus view.

- Analysts are divided as to the extent the individual paragraphs will guide either in favour of / against / keeping optionality for a February cut.

- This is largely down to the view for when the next cut following December will be. Of 22 analysts: 8/22 (36%) expect February, 1/22 Q1 (but month unspecified), 7/22 (32%) expect March, 5/22 (23%) expect April and 1/22 expects Q2 (but month unspecified).

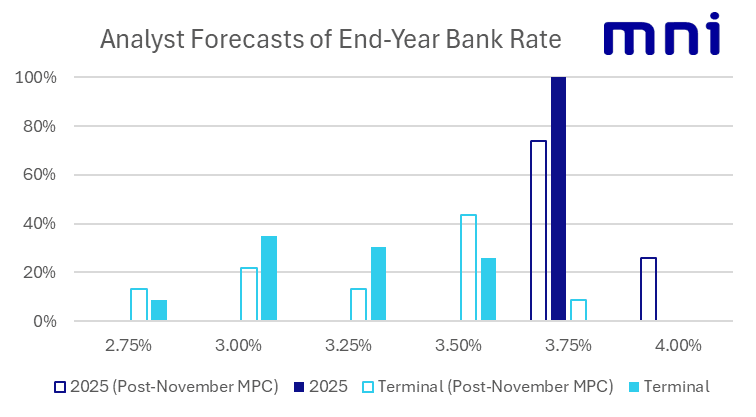

- Expectations for the terminal rate are equally spread. The modal expectation for 8/23 (35%) is 3.00%, the median expectation for 3.25% (7/23, 30%) while almost as many look for 3.50% (6/23, 26%). The remaining 2/23 (9%) look for 2.75%.

- The full MNI BOE Preview will be out a little later today.

BOE: Summary of Analyst Views (1/2)

Dec-17 12:43

- All 23 of the sellside previews that we have read look for a 25bp cut at this week’s meeting (6/23 have changed their call since immediately after the November meeting).

- A 5-4 vote split with Bailey joining the November dovish dissenters is the base case for the vast majority (16/21 analysts).

- 3/21 expect a 6-3 cut: Goldman Sachs (Lombardelli additionally), Nomura (Greene additionally) and UniCredit (unspecified). UBS look for Lombardelli to possibly join Bailey (either 6-3 or 5-4). NatWest Markets "put roughly equal probabilities on 5-4, 6-3 and 7-2 votes." Additionally Santander noted that they “would not be surprised” with a repeat of August’s 2-stage vote with Taylor favouring a 50bp cut in the first round.

- Note that these vote split expectations are all ahead of today’s data but we haven’t seen any explicit call changes here (although plenty noting risks of additional dissenters).