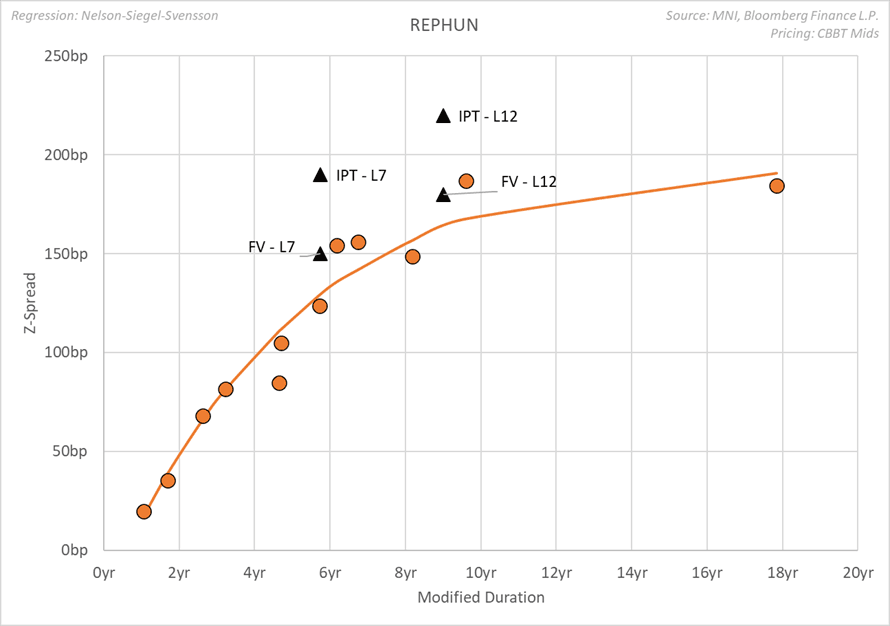

EM CEEMEA CREDIT: Rep of Hungary (REPHUN) : € BMK L7Y and L12Y - FV

Rep of Hungary: € BMK L7Y and L12Y

(REPHUN; Baa2neg/BBB-neg/BBBneg)

L7Y L12Y

IPT 190bp 220bp

FV 150bp 180bp

Republic of Hungary issuing a L7Y and L12Y bonds. For the 7Y we look at the following:

- 4.25% JUN31 bonds are around z-spread of 108bps

- 1.625% APR32 bonds are around z-spread of 125bps

- 5.375% SEP33 bonds are around z-spread of 155bps

We estimate a FV on the new L7Y bonds at MS+150bp

For the L12Y we look at the following bonds:

- 4.5% JUN34 bonds are round z+165bp

- 1.75% JUN35 bonds are around z+155bp

- 4.875% MAR40 bonds are around z+191bp

- We estimate a FV on the new L12Y bond at MS+180bp

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Outperformance Vs. Bunds Stalls Around 165bp

Gilt outperformance vs. Bunds stalled around the 165bp level last week, after the spread tightened by ~25bp since November 12.

- The speed of the tightening, coupled with ongoing medium-term UK fiscal fisks, have been cited as limiting factors by some.

- Fresh extension through 165bp would target the September ’24 closing low (162.01bp).

- Meanwhile, gilt bears will want to force the spread back above the November closing low (172.94bp) to start turning the tide back in their favour.

- Note that Goldman Sachs remain constructive on gilts and maintain their long vs. Bunds and long 10-Year swap spread recommendations.

- Goldman write “gilt risk premia continue to compress, with our measure of country risk premia embedded in 10-Year yields 20bp lower since the budget. We think this reflects the outsized risk premia priced in before, as there was relatively little news on the day, but with ongoing uncertainty in upcoming labour market data and into a likely December BoE cut, we expect this to continue. Gilts have been relatively resilient to bearish impulses from other markets, and the potential for dovish spillovers from upcoming U.S. data could reinforce a move lower in UK yields”.

EURIBOR OPTIONS: Ratio Put Spread seller

0RF6 98.12/98.00ps 1x2, sold the 1 at -6.5 down to -7.5 in 5k.

EGBS: Unwind Off Lows in EGBs as Markets Retrace Small Part of Recent Weakness

- Markets see an unwind off the lows in EGBs and especially in German markets, but not too surprising given Bunds have fallen 176 ticks over the past 6 sessions.

- The heavier volumes are going through in Bobls, although this is composed of a combination of swap related trades and option hedges. Initial resistance in Bunds would be seen further out, up to 128.40.

- Near term risks remain to the downside, meaning market focus will be on yields across core EGB markets.

For the German 10yr Yield, reference 127.93:

- 2.85% = 127.61.

- 2.90% = 127.12.

- 2.94% = 126.73 (2025 high and highest Yield since Oct 2023).