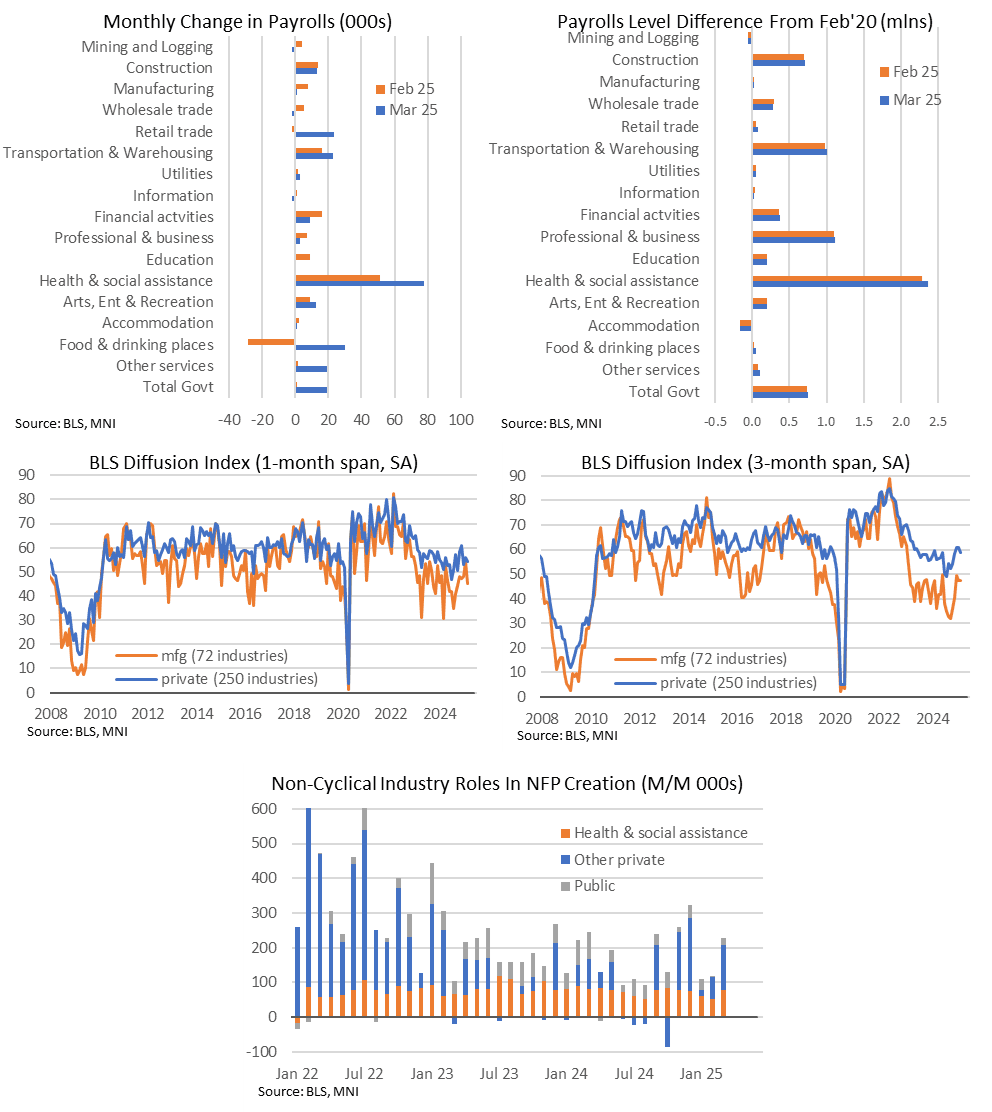

US DATA: Reasonable Breadth To Private Job Gains, Signs Of Weather Boost [2/2]

Apr-04 13:34

- The main driver of the acceleration in private sector payrolls growth was “food & drinking places” as it swung to adding 30k after two monthly declines of -27k/-28k.

- It’s loose evidence of what was perceived to have been a weather drag in Jan and Feb before better weather in March (and indeed, the 87k reporting not at work due to bad weather in the separate household survey nudged below the 2022 value for its lowest March since 2000).

- Elsewhere, the health & social assistance sector remains a major contributor, adding a net 78k jobs in March, its most since Nov, after 51k in Feb.

- In terms of the most tariff-sensitive industries, manufacturing payrolls only increased by 1k in March after 8k in Feb, although that increase was somewhat of a rarity having averaged -9k per month in the prior twelve months to Jan.

- The private sector one-month diffusion index dipped to 54.2% (i.e. more than half of the 250 industries reported net job gains) from a downward revised 56% although this is still reasonable having averaged 54% in 2024 and 58% in 2023.

- The manufacturing diffusion index saw a more abrupt decline as it pulled back to 45% after a solid bounce to 54% in Feb after 48% in Jan. Again though, this isn’t wildly different to recent years, with 44% in 2024 and 47% in 2023.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: ADP Misses Along With Recent Downward Revisions

Mar-05 13:33

- ADP employment growth surprised lower in February with 77k (cons 140k).

- It followed a marginally upward revised 186k (initial 183k) in January but some more notable downward revisions before that including 161k in Dec (from 176k), 169k in Nov (from 204k) and 193k in Oct (from 221k).

- See the revisions in the charts below, with jobs growth generally revised higher in 1H24 before lower 2H24.

- As ever though, note the wide differences with private payrolls. In latest vintages for both release, ADP overshot private payrolls by 75k in Jan after undershooting by 112k in Dec and 75k in Nov.

- That important caveat aside, ADP Chief Economist Richardson writes: “Policy uncertainty and a slowdown in consumer spending might have led to layoffs or a slowdown in hiring last month. Our data, combined with other recent indicators, suggests a hiring hesitancy among employers as they assess the economic climate ahead.”

- Within the details, small businesses appear to be under pressure, with a 17k decline in jobs for those with 1-19 employees. It’s the first decline since Dec 2023 and by its most since Mar 2022.

MNI: CANADA Q4 LABOR PRODUCTIVITY +0.6% QOQ

Mar-05 13:30

- MNI: CANADA Q4 LABOR PRODUCTIVITY +0.6% QOQ

- CANADA Q4 HOURLY COMPENSATION +0.8% QOQ

PIPELINE: Corporate Bond Roundup: Mars 8-Tranche Jumbo on Tap

Mar-05 13:26

As expected, Mars Inc, a family-owned, global leader in pet care, snacking and food, is looking to issue as much as $30B over 8 tranches today. The "jumbo" issuance is expected to help finance it's purchase of Kellanova, also a snacking/food related company for "$83.50 per share in cash, for a total consideration of $35.9B" back in August 2024. Estimates vary from $25B to $30B which would put it comfortably in the top ten largest corporate debt issuance on record.

- Date $MM Issuer (Priced *, Launch #)

- 03/05 $Benchmark Mars 2Y +75a, 3Y +85a, 5Y +100a, 7Y +110a, 10Y +120a, 20Y +135a, 30Y +145a, 40Y +155a

- 03/05 $1B KommuneKredit WNG 5Y SOFR+47a

- $7.8B Priced Tuesday, $36.1B/wk

- 03/04 $3B *KFW +3Y SOFR+29

- 03/04 $2.1B *Meiji Yasuda 30.25NC10.25 6.1%

- 03/04 $1.1B *3M $550M 5Y +80, $550M 10Y +95

- 03/04 $600M *OneMain Finance 7NC3 6.75%

- 03/04 $500M *First Horizon 6NC5 +153

- 03/04 $500M *VeriSign +7Y +125

Trending Top

Jan-30 21:43

Jan-30 21:11