INDIA: RBI Release Minutes From December Rate-Setting Meeting

Dec-19 11:37

Highlights from the RBI's latest minutes release:

- Malhotra: I am in favour of retaining the neutral stance which gives the requisite flexibility to remain data-dependent and act according to the evolving macroeconomic conditions and outlook.

- Gupta: One may ask whether the current rate cut, resulting in a cumulative rate cut of 125 bps, could lead to overheating in the economy. However, not just headline and core inflation, but most other nominal indicators of the economy are prevailing at levels that indicate that the economy at this point is not showing any signs of overheating. Instead, one could interpret the data as indicating that there is slack in the economy.

- Kumar: Too low an inflation rate is not healthy for a developing country like India, suggesting a demand deficit. Against that backdrop, I would like to vote for a 25-bps cut in the repo rate to support the growth momentum, while keeping a status quo on the stance.

- Saugata Bhattacharya: I believe that the cumulative policy rate cuts and liquidity infusions will now have moved the orientation of monetary policy from mildly restrictive to balanced. Pending incoming data, I believe the policy interest rate is now consistent with macroeconomic stability.

- Singh: Given the uncertainty on the external front, it seems prudent to go for only a 25-basis-point cut at this point. Additionally, in view of the dormancy in the price momentum underlying headline CPI and CPI core, and the case for supporting growth momentum, the rate cut should be accompanied by a change in stance to “accommodative”.

- Indranil Bhattacharyya: I also support retaining the neutral stance as it preserves the flexibility to respond judiciously to the evolving situation by remaining data dependent while avoiding the pitfalls of precommitment in an uncertain environment.

Click here to see the full release.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Option Expiries

Nov-19 11:37

Equity Option expiry for Friday in Notional Term:

US:

- SPX: $1.47T vs $1.36T (Monday).

- NDX; $86.64bn vs $77.92bn.

- Amazon: $18.70bn vs $16.93bn.

- Apple: $19.19bn vs $16.97bn.

- NVIDIA: $47.03bn (new update).

EU:

- SX5E: €139.90bn vs €138.74bn.

- SX7E: €4.31bn vs €4.43bn.

- Dax: €14.71bn vs €14.05bn.

- FTSE: £14.50bn vs £14.30bn.

LOOK AHEAD: Wednesday Data Calendar: Trade Balance, Imp/Exp, Fed Speak, 20Y Bond

Nov-19 11:34

- US Data/Speaker Calendar (prior, estimate)

- 11/19 0700 MBA Mortgage Applications

- 11/19 0830 Trade Balance (-$78.3B, -$60.4B)

- 11/19 0830 Imports/Exports MoM

- 11/19 1000 Fed Gov Miran on bank regs

- 11/19 1130 US Tsy $69B 17W bill auction

- 11/19 1200 Pres Trump remarks at Saudi Investment Forum

- 11/19 1245 Richmond Fed Barkin economic outlook

- 11/19 1300 US Tsy $16B 20Y Bond auction (912810UQ9)

- 11/19 1400 NY Fed Williams welcome remarks

- 11/19 1400 FOMC Meeting Minutes

- Source: Bloomberg Finance L.P. / MNI

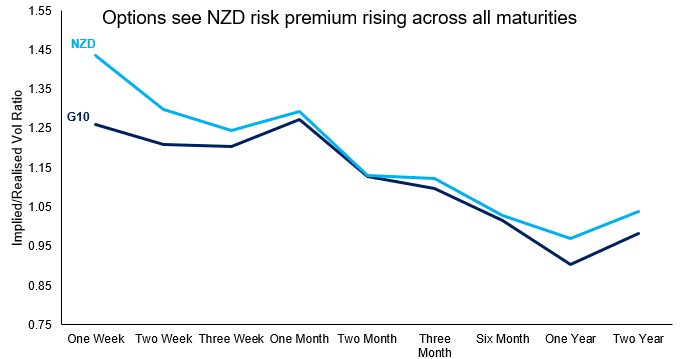

OPTIONS: One-Week G10 Vols See Support as UK Budget, RBNZ Decision Draw Closer

Nov-19 11:29

Vol markets are highly active early Wednesday, with the front-end of the curve capturing key risk events including the UK Budget and the RBNZ rate decision.

- The GBPUSD vol premium over EURUSD has only traded wider on two occasions since the Truss/Kwarteng budget in 2022: January 2025's GBP sell-off, and the BoE's 50bps rate hike in June 2023. This signals broad currency risk into Reeves' Budget - despite more settled expectations of the tax-and-spend measures.

- In anticipation of Wednesday's RBNZ rate decision and expected final cut in the cycle to 2.25%, AUDNZD one-week vols have rallied sharply, topping 8 points for only the third time in three years - the highest since Trump's Liberation Day tariff announcement in April. A signal for further easing seems unlikely - former senior officials told MNI in October that fresh cuts in 2026 would "require a significant deterioration in the labour market and broader activity".

- The RBNZ-tied risk premium is clear to see in the implied/realised vol curve: the one-week maturity now prints the largest premium over the average across G10 FX - including GBPUSD (see below).