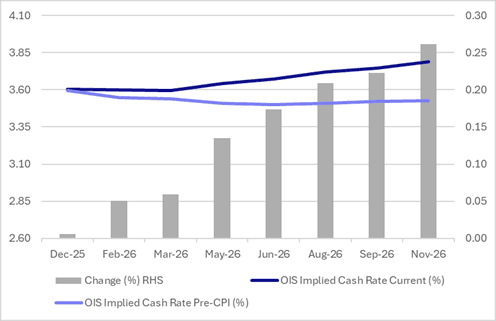

STIR: RBA-Dated OIS Pricing Shows 84% Chance Of Dec-26 Hike After Q3 GDP

RBA-dated OIS pricing is 1-6bps firmer for meetings beyond May after today’s Q3 GDP data. Pricing initially softened on the data but quickly reversed after details revealed underlying strength.

- Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details are a lot stronger than the headline, with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, the largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

- Currently, pricing shows zero probability of a 25bp rate cut in December.

- More notably, the market has shifted to assign an 84% probability of a 25bp hike by December 2026.

- Today’s move extends the recent firming in rate expectations, which began after the stronger-than-expected Monthly CPI on 26 November, to 5–26bps across the curve, led by December 2026.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

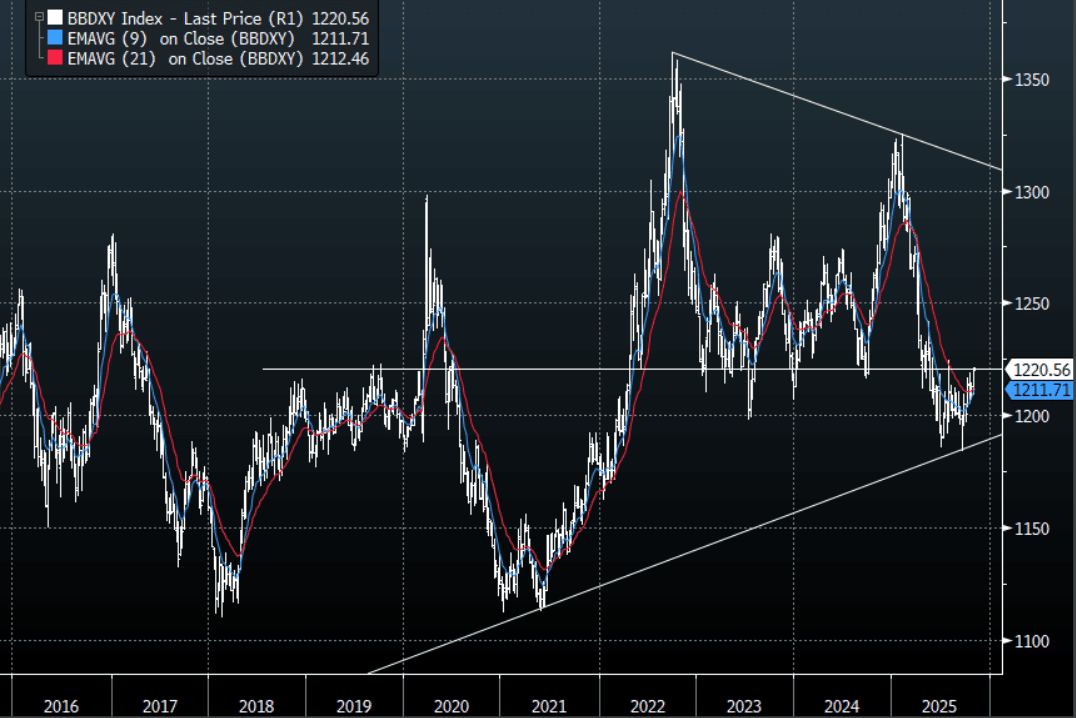

USD: BBDXY-Moving Into Pivotal 1220/1230 Resistance, Risk/Reward Favors a Fade

The BBDXY range Friday night was 1218.44 - 1221.43, Asia is currently trading around 1220, -0.01%. The USD built on its gains from last week into the month-end. The 1220-30 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made on the Daily chart through October. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

- Lance Roberts points out on X that: “There are still a lot of shorts on the dollar, which could fuel a further advance if they are forced to cover.”

- He also refers to a note put out by SocGen: "Over the past decade, the US has consistently outpaced the Eurozone in GDP growth, yields, and inflation — supporting an average EUR/USD near 1.12.”

- “After narrowing growth and rate gaps lifted the euro to 1.19 earlier this year, weaker Eurozone forecasts now point to limited upside, with EUR/USD likely reverting toward its long-term average around 1.12 in the next 18 months." - Societe Generale

Fig 1: BBDXY Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

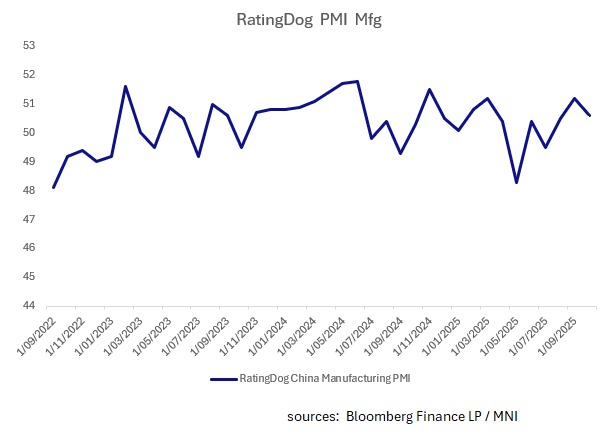

CHINA: Rating Dog Manufacturing PMI Moderates

- The September expansion of the RatingDog PMI manufacturing seemed to reflect a period of expansion ahead of the Xi Trump meeting.

- Whilst today's release for the October data will not capture the impact of the meeting, it is more reflective of the type of expansion that is occurring we think.

- Up +50.6 in October it is a significant decline from the +51.2 in September, but importantly is the third month in a row of expansion.

- Output declined to +50.8 from 52.0 and new orders declined from the month prior.

MNI: CHINA OCT RATINGDOG MANUFACTURING PMI 50.6 VS 51.2 IN SEP

- CHINA OCT RATINGDOG MANUFACTURING PMI 50.6 VS 51.2 IN SEP