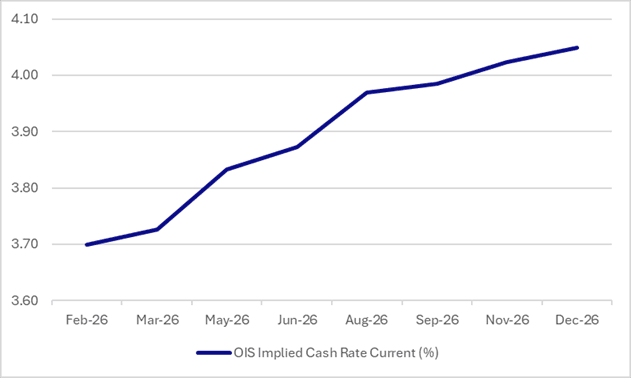

STIR: RBA Dated OIS Prices 45bps Of Tightening in 2026

RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 104% by June and 178% by December 2026.

- By the end of January, the market should have a clearer picture of whether they can expect interest rate hikes in 2026. Quarterly inflation data, due to be released on January 28, will confirm or allay RBA fears that upward price pressures are entrenched in the economy.

Figure 1: RBA-Dated OIS – Current

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

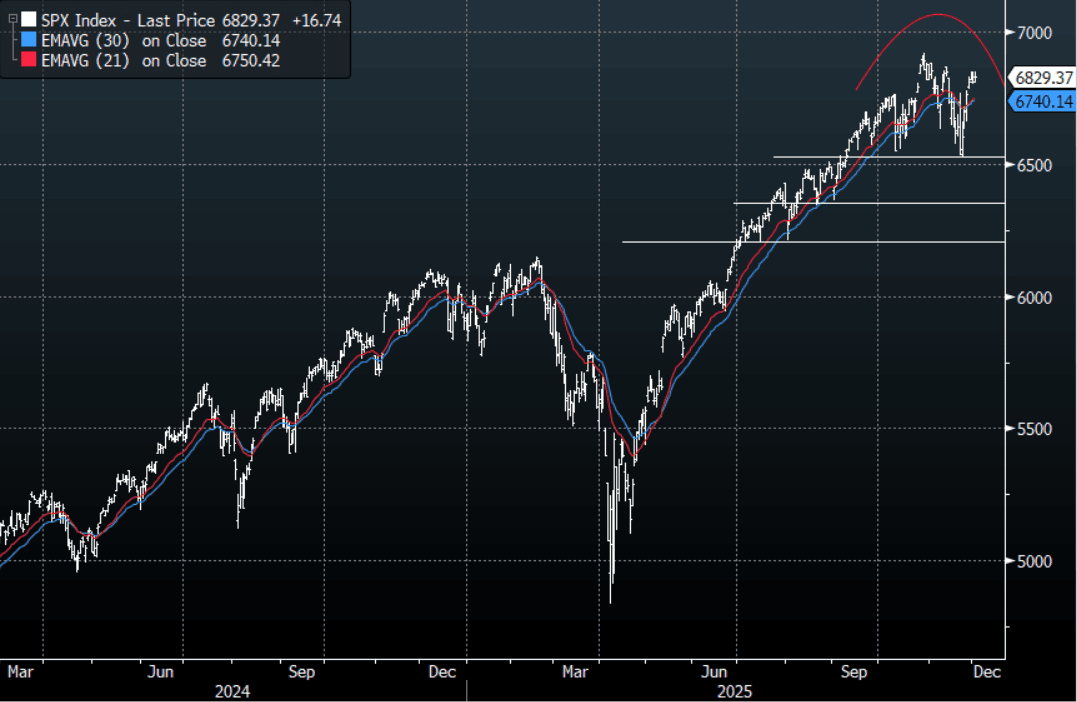

US STOCKS: S&P(ESZ5) - Consolidating Above 6800

The S&P(ESZ5) overnight range was 6812.25 - 6863.50, SPX closed +0.25%, Asia is currently trading around 6840. Risk and Crypto in particular has turned around what looked a fragile start to the week. The Bulls will be liking this price action as the market consolidates above 6800 before potentially having another run higher into year-end. I remain wary of getting bullish up here, but it's tough to argue with the price action. This morning the futures opened a little mixed, E-minis(S&P) +0.05%, NQZ5 -0.02%. On the day support should be back toward the 6750-6780 area as the market looks to potentially challenge 6900 again. Only a break back below 6700-6750 would potentially signal a deeper pullback.

- The S&P 500 Index Average True Range(ATR) for the last 10 Trading days: 80 Points

Fig 1: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: AUD/USD - Moves Lower On GDP Data

The AUD/USD has stalled again towards the 0.6580 area reacting to a lower GDP print. "AUSTRALIA 3Q GDP RISES 0.4% Q/Q; EST. 0.7%" - BBG (Q2 +0.7% & 2.0% - revised), AUSTRALIA 3Q GDP RISES 2.1% Y/Y; EST. 2.2%". The AUD/USD moved very quickly back to 0.6555 after trading around 0.6575 going into it. {AUDUSD Curncy}

AUSTRALIA DATA: Q3 GDP Below Consensus, In Line With RBA Projections

Q3 GDP printed at 0.4% q/q & 2.1% y/y, weaker than Bloomberg consensus expected. Q2 was revised up to 0.7% q/q & 2.0% y/y from 0.6% & 1.8%. Household consumption rose 0.5% q/q. ABS press release can be found here. More details to follow.