US TSYS/OVERNIGHT REPO: Rate Uptick Bolsters Case For QT End This Week

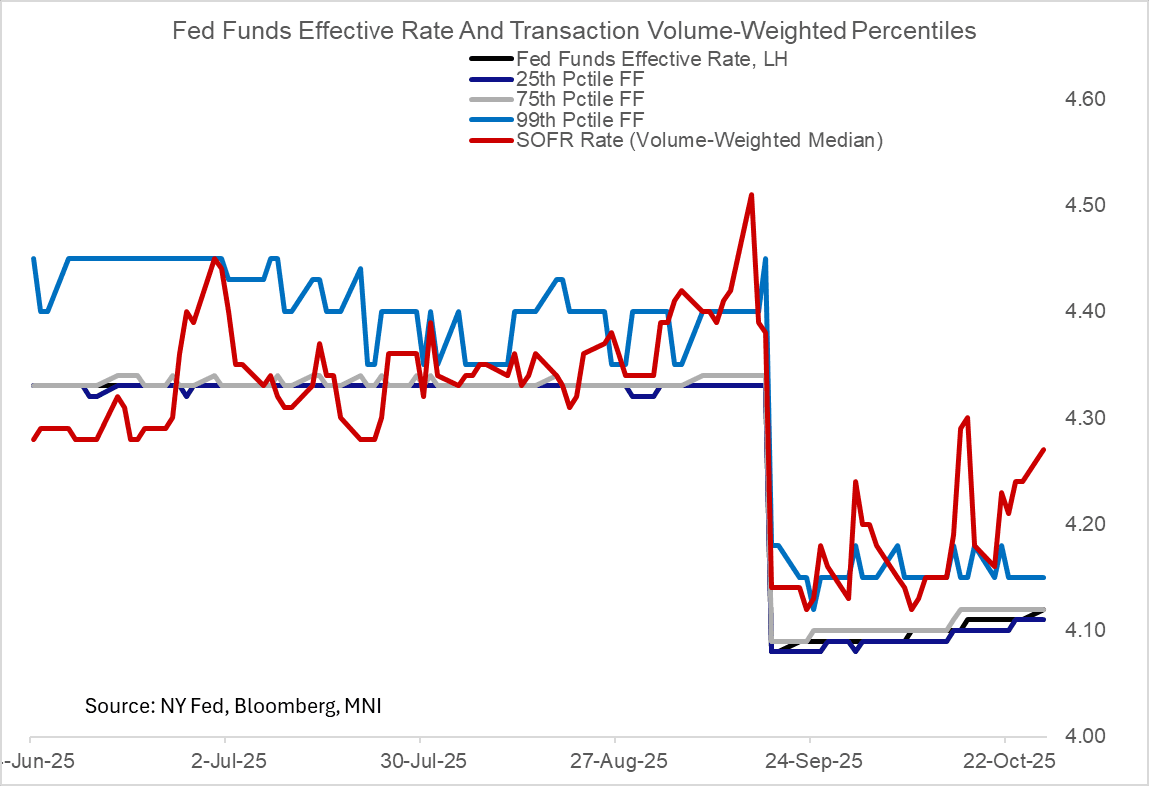

Money market / repo rates showed a notable uptick Monday, with the prints landing just as the FOMC sat down for its 2-day meeting to decide the next move on balance sheet runoff. SOFR, BGCR, and TGCR all rose 3bp, remaining stubbornly above the Fed's IORB rate suggesting that reserves are less ample than they had been.

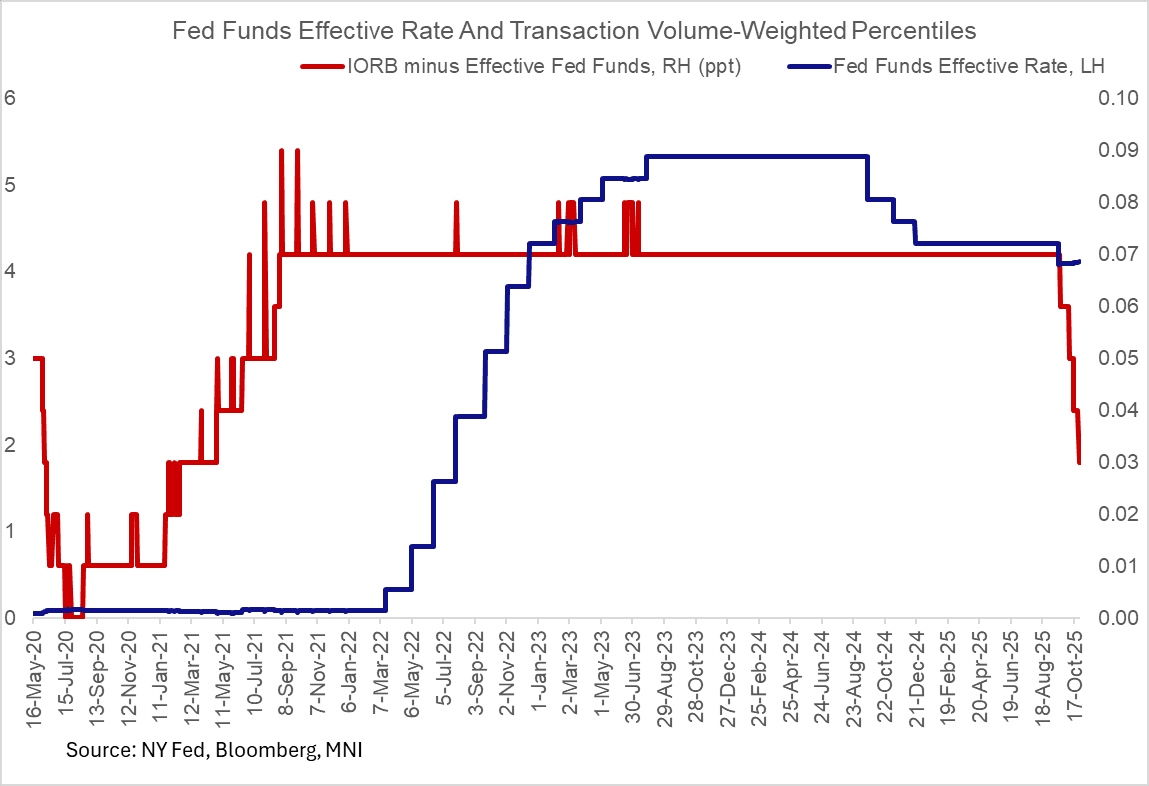

- A semi-surprise was the 4th increase in the Fed Funds effective rate since the September FOMC meeting, with a 1bp uptick to 4.12%. That's just 3bp below IORB after having been consistently 7bp below for most of the cycle. This move has been flagged as a risk for several sessions now, with the EFFR percentiles ticking higher (the published EFFR is a volume-weighted median of overnight fed funds transactions).

- As we noted in our Fed meeting preview, we expect the FOMC to end balance sheet runoff this week, as it assesses the reserve regime to have moved from "abundant" to at/near "ample" - the latest rate moves only reinforce the likelihood of a QT end.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.27%, 0.03%, $3019B

* Broad General Collateral Rate (BGCR): 4.24%, 0.03%, $1131B

* Tri-Party General Collateral Rate (TGCR): 4.24%, 0.03%, $1103B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.12%, 0.01%, volume: $88B

* Daily Overnight Bank Funding Rate: 4.11%, no change, volume: $176B

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MACRO ANALYSIS: MNI US Macro Weekly: FedSpeak Reaffirms Range Of Cut Views (2/2)

While we heard the monetary policy views of 6 of 12 current FOMC voters this week, there were no real surprises. We go through all of the relevant FOMC communications in full in our Macro Weekly PDF.

- Chair Powell reiterated that policy is not on a preset course; Gov Bowman and Gov Miran reiterated their more-dovish-than-median views; Musalem and Schmid suggested only limited scope for easing; and Goolsbee eyed neutral rates 100-125bp lower but was “uneasy” with too much front-loading.

- Virtually of the week’s FOMC speakers noted labor market risks had begun to surface, but had varying concerns about inflation. To sum up:

2025 FOMC Voters:

- Powell Reiterates "There Is No Risk-Free Path", Policy Not On Preset Course (Sep 23)

- Gov Bowman: Concerned Will Need Faster And Bigger Cuts (Sep 23)

- St Louis's Musalem: Limited Room For Easing, Policy May Be Close To Neutral (Sep 22)

- Chicago's Goolsbee Eyes Neutral Rates 100-125bp Lower (Sep 23), Uneasy With Too Much Cut Frontloading (Sep 25)

- Gov Miran: Appropriate Rates In 2.00-2.50% "Ballpark" (Sep 22)

- KC Fed's Schmid: Slightly Restrictive Policy The "Right Place To Be" (Sep 24)

Non-2025 Voters:

- Atlanta's Bostic Pencils In No More Cuts this Year, But Watching Data (Sep 22), Longer-Run Dot Suggests Limited Impetus To Cut Further (Sep 23)

- SF's Daly: Likely Further Cuts Will Be Needed To Support Labor Market (Sep 24)

- Cleveland's Hammack: Policy Very Mildly Restrictive, Concerns On More Cuts (Sep 22)

- Dallas's Logan: Time To Move From Fed Funds Policy Rate To Tri-Party Repo (Sep 25)

- Barkin: Jobs Shakier, Inflation Less Troubling (Sep 26)

MACRO ANALYSIS: MNI US Macro Weekly: Too Solid For Comfort (1/2)

We've just published our US Macro Weekly - Download Full Report Here

- The US economy now appears to be on more solid footing than it seemed a week ago. Versus 45bp in Fed rate reductions through the remainder of 2025 as of last Friday, futures markets now price 40bp. Half of that retracement came Thursday at 0830ET, when Q2 GDP data, initial jobless claims, durable goods orders, and goods trade data all pointed to stronger ongoing GDP growth than previously anticipated.

- Q2 GDP growth was revised up significantly in the 3rd and final reading, to 3.84% Q/Q SAAR from 3.29% in the 2nd reading (consensus had expected this to be unchanged in the 3rd).

- And while that’s in the past, the latest monthly data saw the Atlanta Fed's GDPNow estimate for Q3 jump to 3.9% from 3.3% last week.

- Friday’s PCE data suggested solid consumption dynamics through August (and no nasty surprises in the core inflation data).

- As such, the week’s data almost unambiguously portrayed a better domestic demand story through – and beyond – a volatile first half of the year related to tariff policy shifts.

- That poses something of a quandary for a Fed that has shifted its sights to labor market risks. GDP is not employment, but a case for rate cuts at a time when inflation is still pushing 3% is tougher to make when the economy is growing at close to a 4% real pace and equities remain at or near all-time highs.

- October's cut is no longer such a sure thing as it seemed after the September meeting, with a 25bp ease now priced at 21bp (~84% implied prob), versus closer to 23bp (90+%) at the end of the prior week.

US TSY OPTIONS: BLOCK: Large Nov'25 5Y Risk Reversal, Covered

- +30,000 FVX5 108.5/109.5 call over risk reversals, 0.5 net vs.

- -18,000 FVZ5 108-31.75 at 1536:10ET