NORGES BANK: Rate Path Revisions Push Back On Significant Easing Expectations

Dec-18 09:17

The desk is having issues downloading Norges Bank’s detailed projections excel. In lieu of that, looking at annual average policy rate projections from the MPR itself, it looks like the 2026 average policy rate level is unchanged at 3.9%, while the 2027 and 2028 levels have been downwardly revised by a tenth each to 3.4% and 3.2% respectively.

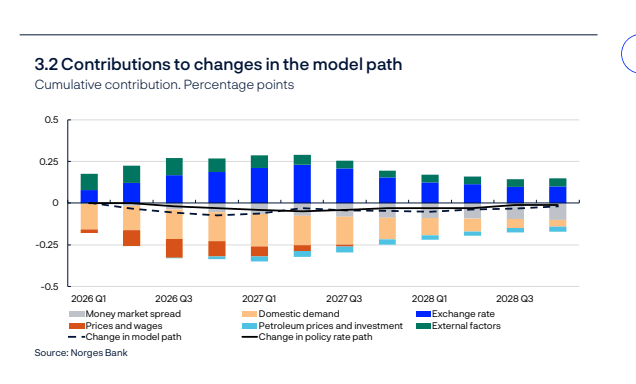

- In the MPR, the changes to the December MPR rate path relatively to September look qualitatively small (see chart, possibly less than 10bps across the horizon). Although the implied probability of 2x25bp cuts next year has increased, Norges Bank retains a preference for a cautious easing cycle due to sticky inflation and only gradually slowing mainland activity.

- That looks to have contributed to modest NOK strength and upside in NOK rates since the decision was published.

- We note that the judgement factor (i.e. the difference between the actual rate path and the model implied path) was a hawkish contributor at the front of the path, seemingly an explicit decision from the Board to push back on easing expectations.

- Summarising the component contributions to the December MPR path revisions:

- Significant hawkish role from the exchange rate – Moreso than we expected: “The krone exchange rate is weaker than assumed in the September Report and a weaker krone is also projected ahead”…. “The exchange rate therefore pushes up the model-based path”

- Small downward contribution from prices and wages (as expected); “Underlying inflation has been broadly as projected in the September Report, and the projections for 2026 are little changed…. On the whole, prices and wages pull down the model-based path in the first half of the forecast horizon”

- Domestic demand the main downward contributor (as expected): “The output gap projection has been revised down, partly owing to developments in the labour market and in the capacity utilisation indicators reported by the Regional Network that were weaker than previously assumed.”…” Domestic demand pulls down the model path”

- Money market spread a dovish contributor as expected.

- Limited impact from petroleum prices and investment – we had expected a dovish impact.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: Call Condor

Nov-18 09:15

SFIZ5 96.25/96.30/96.35/96.40c condor, bought for 2.5 in 4.5k.

FRANCE: OATs Widening Alongside Peers, But Domestic Political Risks Increasing

Nov-18 09:14

The 10-year OAT/Bund spread is back at 75bps, 1bp wider on the day alongside EGB peers. While continued weakness in equity benchmarks looks to be the main driver of recent EGB spread widening, domestic political developments remain a risk to monitor.

- This morning, Le Parisien reported that members of the centre and right “agreed” that they would note vote in favour of the revenue section of the 2026 budget, if it were to be put to a vote in its current form. Link here

- Sources suggest this would be “due to the insincerity of some of the measures adopted”.

- However, the report does not contain information on whether ministers would abstain from a vote, or vote against the motion.

- Ultimately, it underscores the difficult balancing act PM Lecornu is facing. Amendments to the budget to date have already pushed the expected 2026 deficit towards (or above) 5%, versus a target of 4.7%.

- Meanwhile, the Senate starts reviewing the Social Security section of the budget tomorrow. Actions around the 2023 pension reform suspension are in focus.

EU-BOND SYNDICATION: 2.50% Oct-30 EU-bond tap: Spread set

Nov-18 09:04

- Spread set MS + 12bps (guidance was MS + 15bps area)

- Tap Size: E5bln (WNG) (MNI expected E5-6bln)

- Books in excess of E83bln (inc E6.75bln JLM interest)

- Settlement: 25 Nov 2025 (T+5)

- Maturity: 14 October 2030

- ISIN: EU000A4EG021 (immediately fungible)

- JLMs: GSBE SE / HSBC / J.P. Morgan (DM/B&D) / Natixis / UBS

- Timing: Books to close at 9:30GMT / 10:30CET

From market source