ZAR: Rand Snaps Three-Day Losing Streak

Aug-28 08:11

USD/ZAR deals at 17.6679, a touch lower on the day, with market participants eyeing fresh cues. Familiar technical levels are in play, with bears looking for a sell-off towards 17.2711, the Nov 7 2024 low, while bulls keep an eye on the 50-EMA at 17.7755, followed by Aug 1 high of 18.3607.

- SAGB yields have eased off across the curve. South Africa's 5-year breakeven inflation rate sits at 3.66%, having moved sideways near cyclical lows over the past couple of months. The 10-year rate sits at 4.60% after printing cycle lows at the beginning of the month.

- The composite BBG Commodity Index is virtually unchanged on the day; the precious metals subindex has added 0.3%. Gold trades just shy of neutral levels.

- The National Energy Regulator of South Africa (NERSA) will allow Eskom to raise electricity prices by more than previously agreed on the back of a settlement of their legal dispute.

- Producer prices are expected to have increased by 1.4% Y/Y in July. Statistics SA will publish the data at 10:30BST/11:30SAST.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: Large Call Spread

Jul-29 08:06

SFIM6 97.40/97.50cs, bought for 0.75 in 10k.

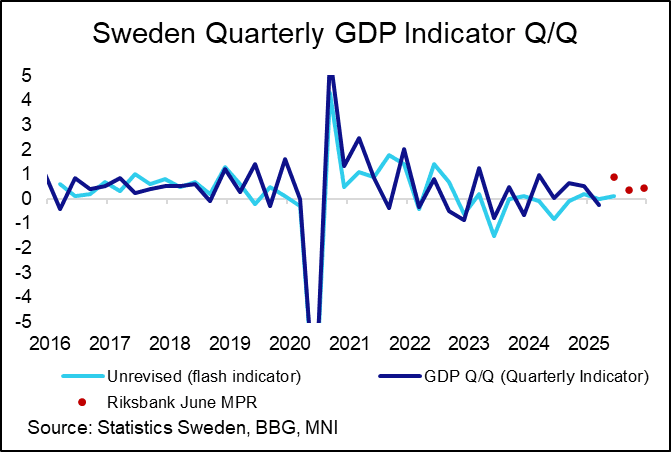

SWEDEN: Q2 Flash GDP Weaker Than Expected

Jul-29 08:00

The Swedish flash Q2 GDP indicator was weaker-than-expected at 0.1% Q/Q (vs 0.3% cons, -0.24% prior). As always, a generous pinch of salt should be taken with this indicator, it can be heavily revised and is often a poor predictor of actual GDP outcomes (Q2 due at the end of next month). The market reaction has been relatively limited for now.

- The 0.1% reading was significantly below the Riksbank’s June MPR projection of 0.9%. We suspect that the extremely weak May retail sales report, which also pulled down the May monthly GDP estimate, has had a large role to play here.

- June retail sales are due tomorrow, which will also reveal whether May’s -4.8% M/M is revised.

- June monthly GDP was 0.5% M/M (vs a downwardly revised -0.8% prior from -0.2% initial). However, no details are released today.

- Despite its caveats, the message from the GDP indicator is consistent with an economy that is still a little subdued despite 200bp of Riksbank cuts. It leans in favour of market expectations for one more cut this year. The July flash CPI report (due next Friday) may be important in determining whether an August cut is still on the cards.

- While trade policy uncertainty has reduced since the US-EU struck an agreement at the weekend, the terms of the deal would still exert a toll on Sweden’s export-sensitive economy.

MNI: ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.6%

Jul-29 08:00

- MNI: ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.6%

- MNI: ECB 3-YEAR CONSUMER INFLATION EXPECTATIONS 2.4%