ZAR: Rand Appreciates, Market Weighs CPI Data

Spot USD/ZAR is around 450 pips softer on the session, last changes hands at 17.3657. The rand's rally from Aug-Sep has stalled, with bulls trying to force a break above the 50-EMA (17.4391) in a bid to set the stage for a firmer rebound. Meanwhile, a sell-off past Oct 9 low of 17.0683 and Sep 30, 2024 low of 17.0356 would revive bearish hope for a breach of the 17.0 handle.

- Consumer prices in South Africa rose by 3.4% in September, picking up from +3.3% in August and moving away from the SARB's implicit +3.0% target. The SARB holds its next monetary policy meeting on November 20. The 3-month JIBAR/1x4 FRA spread now sits at 13bp.

- SAGB yields have crept higher across the curve. South Africa's 5-year breakeven inflation rate sits at 3.55%, while the 10-year rate has edged higher to 4.27%, extending its move away from multi-year lows printed on Monday.

- Bloomberg Commodity Index is up by 1.3% and the precious metals subindex has added 1.6%. Gold trades ~$12.8/oz. above neutral levels after a recent correction from all-time highs reached at the turn of the week.

- The SARB will release its bi-annual Monetary Policy Review this evening.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

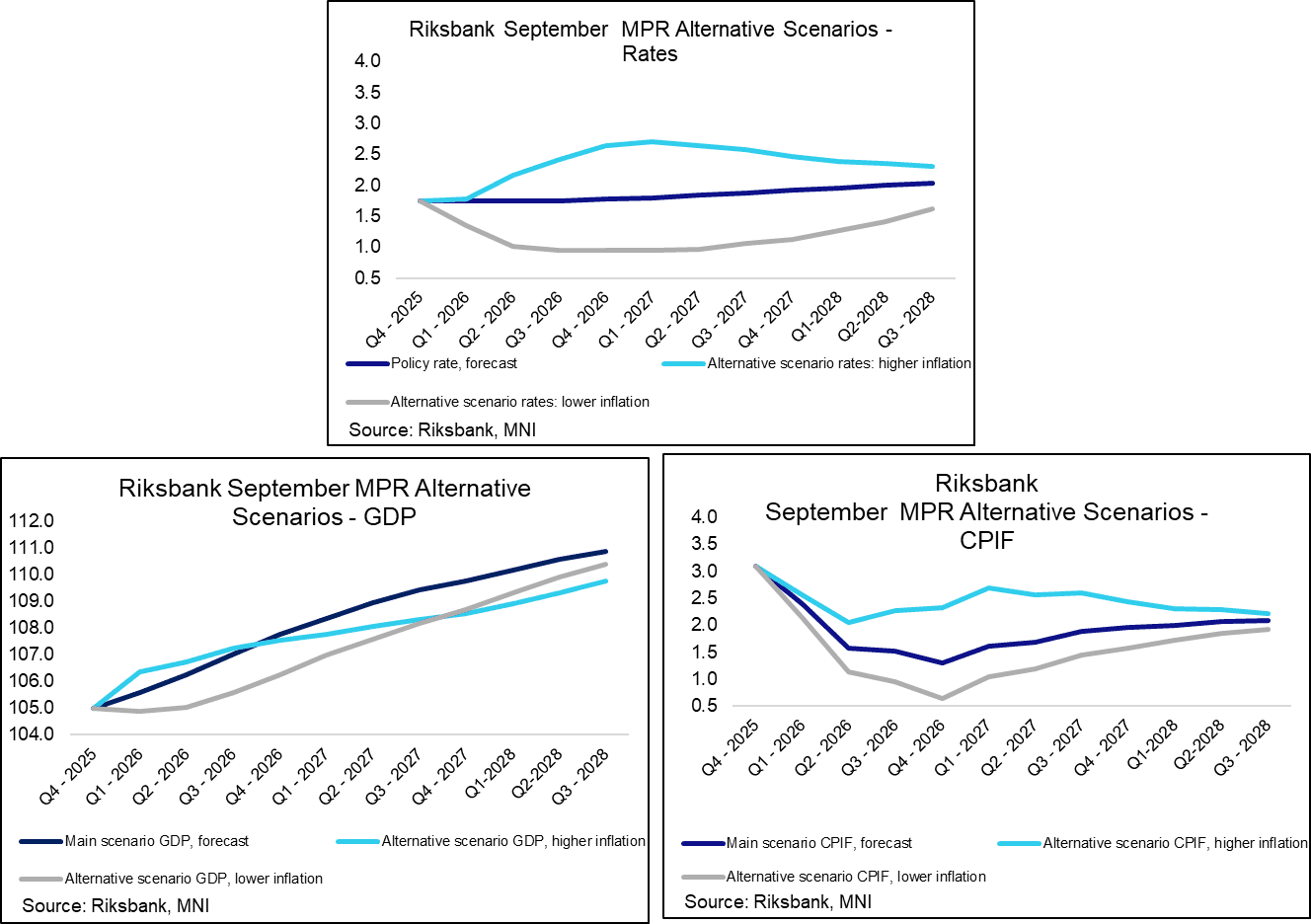

RIKSBANK: Alternative Scenarios Illustrate Potential Reaction Functions

As always, the Riksbank MPR contains alternative scenarios for the policy rate, CPIF and GDP. These shouldn't be considered "guidance", but more an illustration of what risks the Board is thinking about, and the possible reaction function the Board would ex ante employ to respond to them.

Scenario 1: Domestic consumption grows faster than expected, but global supply shocks increase

- Consumption rises partly a result of the government’s announced fiscal policy, but a deterioration in global politics “will begin to negatively affect the global economy in the form of various supply shocks, including supply chain disruptions”

- “These shocks will also affect Sweden, and GDP growth will slow down after having recovered more quickly towards the end of 2025 than in the Riksbank’s forecast. The combination of higher domestic demand and global supply shocks will cause inflation to rise and be higher than in the main scenario”

- This interesting scenario describes a positive demand shock eventually being overpowered by a negative supply shock – both push up inflation but the demand-driven growth impulse eventually fades.

- It highlights that the Riksbank will respond hawkishly even if growth falls in a negative supply shock scenario.

Scenario 2: Stock market decline causes lower confidence in Sweden

- The Riksbank notes that “the stock market decline will lead to lower confidence in economic developments among Swedish households and companies. Unlike the most recent decline in household confidence, this one will be more prolonged.”

- Interestingly, the Riksbank does not assume that the SEK would be a shock absorber in such a scenario, “which makes the fall in GDP and inflation even greater”

- The scenario envisages a persistent dovish response from the Riksbank.

UK DATA: PMI data disappoint and prices continue to rise

Disappointing UK flash September PMI with services 1.6 points below forecast, falling 2.3 points to 51.9 (but that's pretty much back to July levels of 51.8 so it shouldn't be overinterpreted). Manufacturing 0.9 points below consensus at 46.2 while composite at 51.0 if 2.0 points below consensus. The most concerning part of this for the MPC will be regarding the "solid rise in prices changed in September." That won't sound very appealing to the swing members on the committee ahead of the Q4 decisions. Recall that we will hear from both Breeden and Ramsden in speeches in the first half of next week.

- "Subdued demand and pressure on margins from sharply rising input costs contributed to another reduction in private sector employment numbers."

- "The latest decline in manufacturing output was the fastest since March, with survey respondents mostly citing weak order books from both domestic and export markets. There were also some specific mentions of lower manufacturing output across the automotive supply chain as a result of plant stoppages at Jaguar Land Rover."

- "The rate of input price inflation edged down from August's three-month high, but remained well above the pre-pandemic average. Service providers again recorded a particularly steep rise in their operating expenses, which was attributed to elevated wage pressures and efforts by suppliers to pass on higher payroll costs. There were also reports of rising energy bills, food prices and technology costs."

- "Service sector firms recorded a solid rise in their prices charged in September, with the rate of inflation only slightly lower than seen on average in the year-to-date. In contrast, manufacturers recorded a marked slowdown in factory gate price inflation to its softest since December 2024, which survey respondents linked to intense competitive pressures."

GBP: Cable losses 20 pips post UK PMIs Data

- Cable drops 20 pips following the UK Data miss.

- For now it seems to be finding some demand at 1.3500, but further downside continuation will open to 1.3453 Low Sep 22.