EM LATAM CREDIT: Raizen: Notice to the Market

Feb-06 20:59

(RAIZBZ; Ba1*-/BBB-neg/BBB-*-) "following consultation with its controlling shareholders, it was in...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Midweek Data Dump Sees Treasury Futures Rebound, Curves Bull Flatten

Jan-07 20:44

- Treasuries look to finish stronger, upper half of a relatively volatile session range on heavier volumes (TYH6 over 1.8M) after the bell, curves bull flattening: 2s10s -3.941 at 66.838, 5s30s -2.641 at 112.372.

- Midweek data dump kicked off with monthly ADP - Treasury futures extend gains after ADP employment data came out lower than expected (prior drop up-revised slightly). Futures paring gains after stronger than expected ISM services, new orders and employ print, prices paid declines slightly; JOLTS openings & layoffs retreat while quits levels rise.

- Job openings ended November much lower than expected at 7146k (cons 7648k) after a downward revised 7449k in Oct (initial 7670k) and 7658k in Sep. It’s the lowest level of openings since Sep 2024 and before that Dec 2020.

- December's ISM Services report was meaningfully stronger than expected, with the headline PMI index surprisingly jumping to a 14-month high 54.4 (52.2 consensus, 52.6 prior). This was a strong report across the board, with all four major subindices in expansionary territory (Business Activity, New Orders, Employment, Supplier Deliveries) for the first time since February 2025, and a further downtick in price pressures.

- Some posts from Pres Trump rattled equities somewhat, at least housing and defense stocks after he pushed to ban large institutions from buying single-family homes, and warned defense contractors and the industry as a whole that executives should be prevented from making more than $5M annually, while the sector should be barred from allowing dividends and share buybacks.

- FX markets have been lacking conviction to start the year, potentially in anticipation of this Friday’s US employment report.

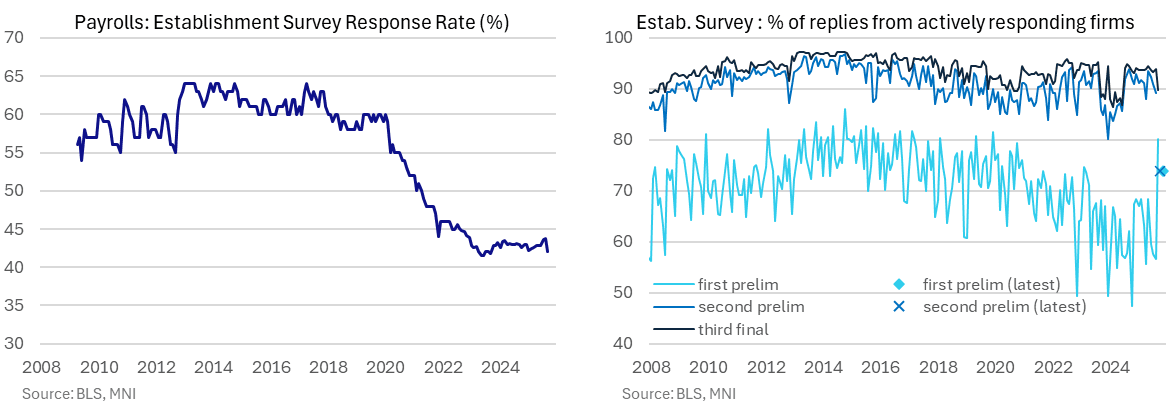

US LABOR MARKET: Mixed Revision Implications For December Payrolls Report

Jan-07 20:41

- Data quality continues to be top-of-mind in key US data releases, with the establishment survey of the payrolls report not seeing the same drop off in response rates as the CPI survey has under the second Trump administration but having started from a low base.

- Last month’s combined Oct-Nov payrolls release saw some mixed results for the share of responses of actively reporting sample units, owing to longer collection periods whilst keeping the standard reference period that includes the 12th day of the month.

- The first preliminary rate of 73.8% in November was again high compared to recent years even if it dipped from the 80.2% in the September report that had been particularly delayed by the government shutdown (initial response rates averaged 62% in the first eight months of 2025).

- On its own that would imply smaller than usual scope for upcoming two-month revisions but the October rate at least somewhat goes against that at 73.9%, at least if comparing with typical second response rates closer to 90%. That said, the BLS clearly describes this as an “initial” estimate and it being “higher than usual as a result of the extended collection periods” despite including enough detail that would typically only have been available with the second update. We crudely show it as a second response rate in the below charts.

- The third and final response rate of 89.8% (again, of actively responding units) fell from 93.9% for its lowest since Jun 2024, which if replicated or improved upon this time would leave a lot of ‘new’ information to be received since that October update.

- The overall response rate meanwhile drifted lower still from 43.8% to 42.1% for its lowest since Sep 2023 and one of its lowest on record.

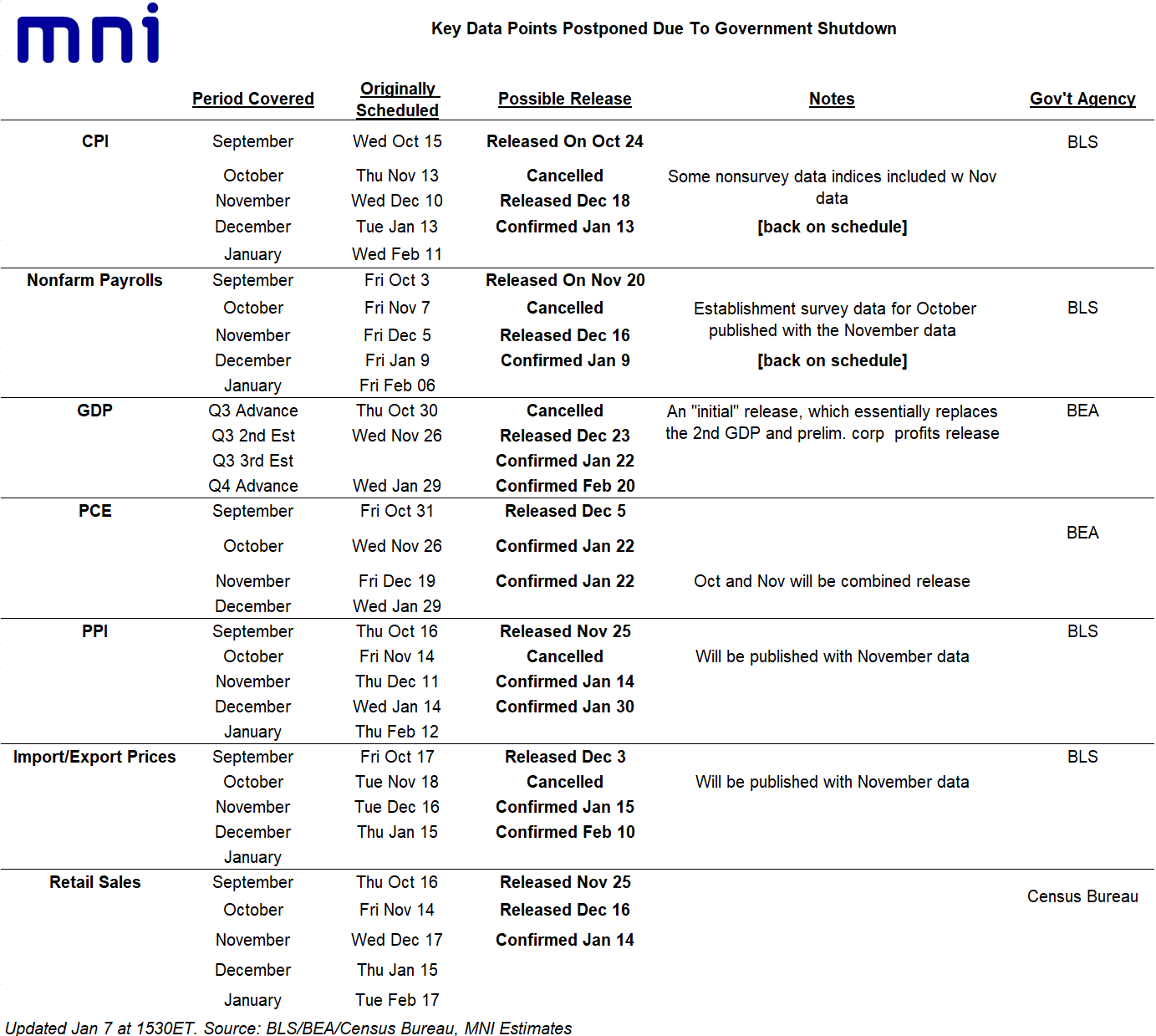

US DATA: Oct/Nov PCE Releases To Be Combined, Out Before Jan FOMC Meeting

Jan-07 20:36

The US BEA has announced a few rescheduled key reports in the coming weeks:

- There will be a combined October and November PCE report out on January 22, at 10am ET - in time for the Fed's meeting the following week. These had been due out on Nov 26 / Dec 19, respectively.

- It's unclear how the October release will be compiled given a lack of CPI data for the month.

- Additionally the BEA rescheduled the advance estimate of Q4 GDP for Feb 20, alongside the December PCE report. These releases had originally been due out on Jan 29.

- Indeed the January PCE report and second Q4 GDP estimate had originally been scheduled for Feb 26 - but at least the BEA is evidently catching up to the shutdown-related backlog.

- Below is a list of major releases