EM LATAM CREDIT: Raizen: Moody’s Downgrade – Negative

(RAIZBZ; Ba1*-/BBBneg/BBB-*-)

• Persistent negative free cash flow generation and high leverage that was expected to remain elevated above its 3x debt leverage threshold were cited as reasons for the downgrade. Moody’s cited commodity market volatility that Raizen is exposed to in its sugar ethanol business and large capex requirements as necessitating a more conservative capital structure. The rating agency acknowledged discussions of a capital increase and further asset sales which if completed would stabilize the rating in our view.

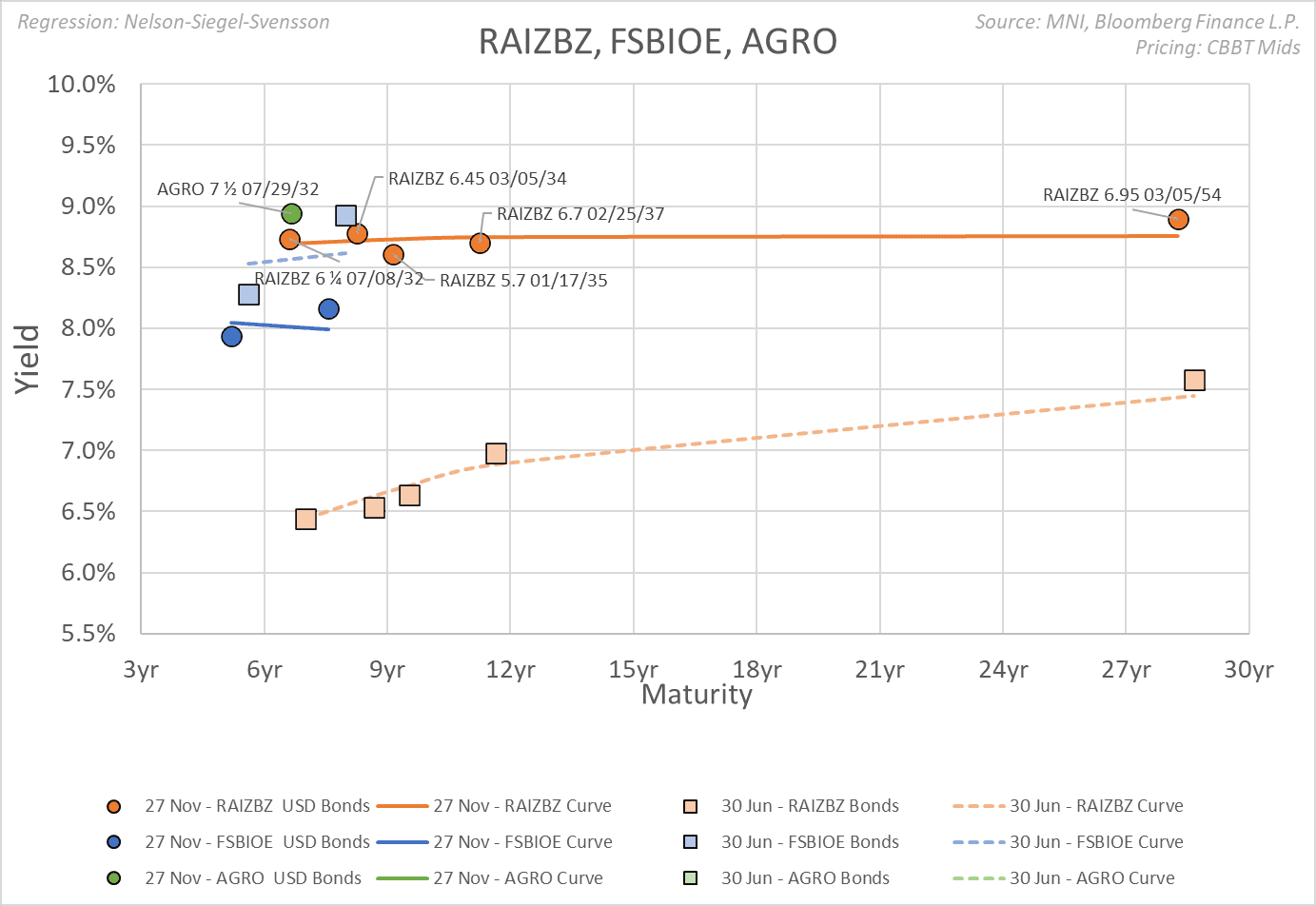

• RAIZBZ 32s were quoted at $88, or 8.67%, which was down .17 today. That compares to lower rated corn ethanol processor FS Bioenergia (FSBIOE; Ba3neg/NR/BB-) 33s at 8.1% and Brazil sugar ethanol producer Adecoagro (AGRO; Ba2*-/BB*-/NR) 32s at 8.73%.

• Moody’s cited gross leverage of 5.4x which ignores the BRL18.6bn (USD3.5bn) of cash on the balance sheet. Fitch projected net leverage of 4x in 2026 absent any further asset sales or capital raise. Fitch also views Raizen as having a larger scale and less commodity price risk than FS Bio so all things being equal would likely rate Raizen higher. We expect a sale of the Argentina refinery and gas station assets for proceeds of USD1.4bn but a capital increase would also be needed at this point to get to leverage targets.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: BOC Links - URLs will update at 0945ET

- Interest Rate Announcement: https://www.bankofcanada.ca/2025/10/fad-press-release-2025-10-29/

- Press Conference Opening Statement: https://www.bankofcanada.ca/2025/10/opening-statement-2025-10-29/

- Monetary Policy Report: https://www.bankofcanada.ca/publications/mpr/mpr-2025-10-29/

US: MNI POLITICAL RISK - Trump Xi Meeting Confirmed For Thursday

Download Full Report Here

- President Donald Trump is in South Korea for the final leg of his Asia trip. Trump said a trade with Seoul was "pretty much finalised.”

- Trump confirmed he will meet Chinese President Xi Jinping on the margins of APEC on Thursday. The meeting is likely to take place at 22:00 ET (Wednesday) 02:00 GMT 11:00 local. Trump predicted the meeting could go for three or four hours.

- The prevailing view among analysts is that the tariff and export control truce will be extended, but a more comprehensive trade deal is likely to remain elusive. Trump was bullish that a deal would be struck on Fentanyl, opening the door for a reduction in tariffs on Chinese exports. Trump also hinted at providing China access to Nvidia’s powerful Blackwell AI chip.

- Five Republican senators voted with Democrats to pass a messaging resolution blocking Trump’s Brazil tariffs, showing there is a workable anti-Trump coalition in the Senate.

- Senate Democrats blocked the House-passed Republican government funding bill for the 13th time. Bipartisan talks have “picked up” but there doesn’t appear to be an immediate offramp out of the shutdown.

- The Gaza ceasefire is facing a major test after Israeli strikes.

- A bipartisan coalition of governors urged Congress to pass legislation easing energy permitting rules.

- The US struck four more alleged drug vessels in the Eastern Pacific.

- Chart of the Day: 'Lopsided' US trade deals could push Southeast Asian nations closer to China.

Full Article: US DAILY BRIEF

SOFR OPTIONS: Call Spread vs Put Spread

0QM6 96.50/96.00ps vs 97.50/98.00cs, bought the cs for flat in 5k.