NORWAY: Q4 RNS Dovish On Net, But Oil Services Role May Temper Mkt Reaction

Dec-11 09:47

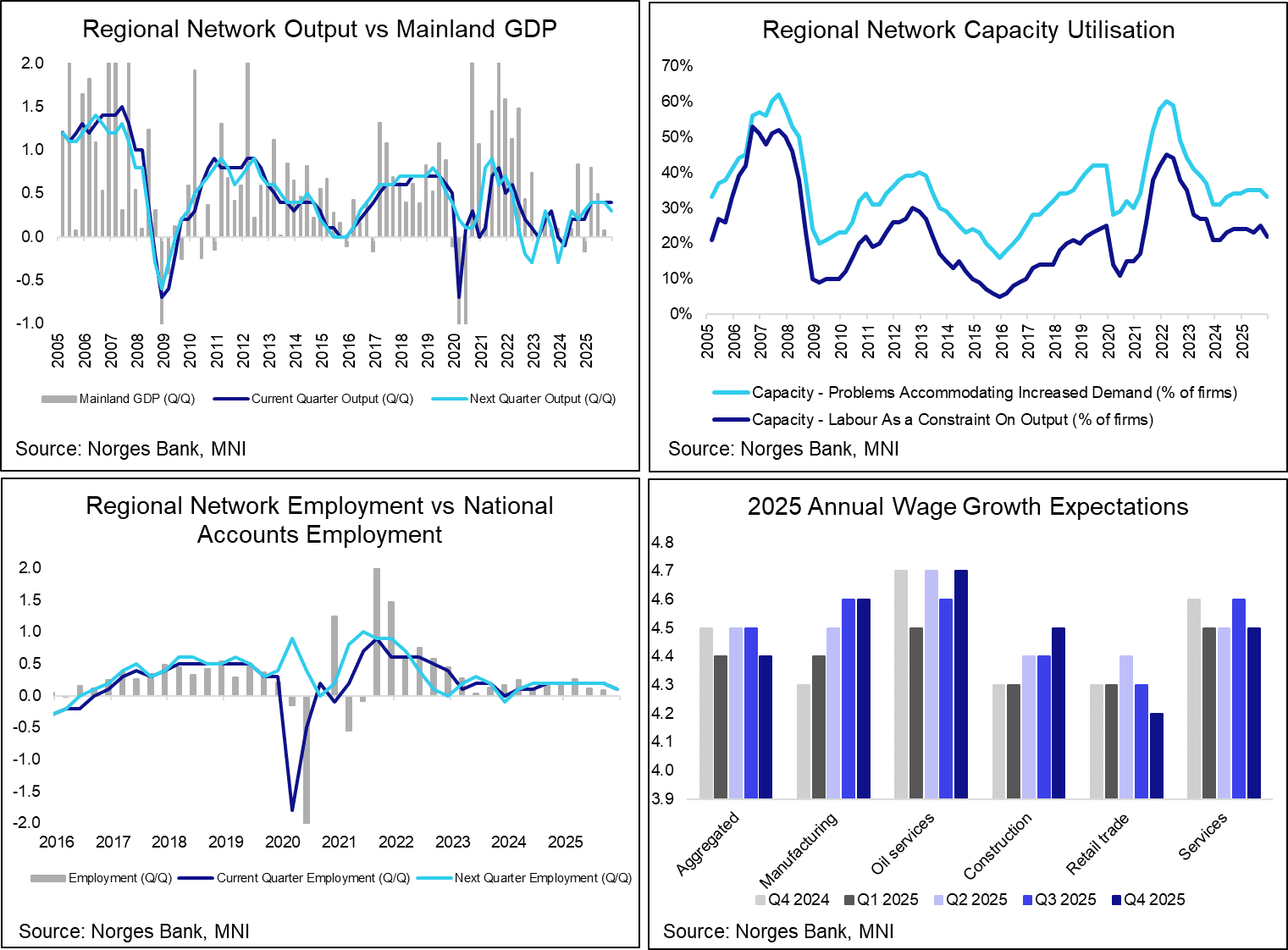

Overall, the Q4 Regional Network Survey (RNS) should have a net dovish impact on Norges Bank’s December MPR rate path. This is being reflected in NOK rates markets, with the Sep26 – Dec26 FRA contract down 4bps on the session. Bloomberg’s MIPR function suggests there are around 30bps of easing priced over the next year. The dovish reaction may be being tempered a little by the outsized role oil services played in downward revisions for many components.

- Norges Bank’s September rate path was consistent with one rate cut in each of the next three years, but recent developments suggest this outlook may be a little too hawkish. That said, we aren’t expecting material revisions, with the December path unlikely to endorse more than 2x25bp cuts next year.

- The capacity utilisation components of the RNS are the most important parts of the survey, in our view. The proportion of firms citing labour as a constraint on output fell to 22%, the lowest since Q1 2024 and 3pp below last quarter’s reading. The share of firms reporting problems accommodating an increase in demand also fell to 33% (vs 35% prior).

- One offsetting detail is that oil services (alongside the rate-sensitive construction sector) saw the largest downward revisions. The retail saw notable increases in capacity utilisation.

- Although there was a one-tenth upward revision to 2026 wage growth expectations, the 4.1% reading remains below Norges Bank’s 4.2% projection.

- On the output side, current quarter output of 0.4% Q/Q is in line with Norges Bank projections, while next quarter’s output is seen at 0.3% Q/Q. Downward output revisions were seen in oil services, manufacturing and construction, offset by upward revisions/steady growth in retail trade and services.

- Employment expectations were revised down to 0.1% Q/Q in the current and following quarter. Sectoral changes were consistent with the output responses.

- Investment expectations provided a more positive growth signal. For 2026 (3.3% Y/Y vs 1.6% in the Q3 survey), this was driven by the services and manufacturing sectors.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Nov11 NY cut 1000ET (Source DTCC)

Nov-11 09:47

- AUD/USD: $0.6450(A$644mln)

--------------------------------------------------------

Larger FX Option Pipeline

- EUR/USD: Nov12 $1.1500-05(E1.1bln), $1.1688-90(E1.3bln); Nov13 $1.1590(E1.5bln)

- USD/JPY: Nov13 Y147.00($1.6bln), Y152.96-00($1.1bln), Y155.00($1.1bln)

- GBP/USD: Nov12 $1.3100(Gbp1.9bln), $1.3225-30(Gbp1.3bln)

- AUD/USD: Nov12 $0.6500(A$1.2bln), $0.6530-50(A$1.2bln); Nov14 $0.6750(A$2.2bln)

- USD/CAD: Nov14 C$1.4025-35($1.2bln)

SPAIN T-BILL AUCTION RESULTS: 3/9-month letras

Nov-11 09:42

| Type | 3-month letras | 9-month letras |

| Maturity | Feb 6, 2026 | Aug 7, 2026 |

| Amount | E706mln | E1.612bln |

| Target | E2.0-3.0bln | Shared |

| Previous | E885mln | E1.35bln |

| Avg yield | 1.908% | 1.965% |

| Previous | 1.918% | 1.960% |

| Bid-to-cover | 2.86x | 2.15x |

| Previous | 2.27x | 2.19x |

| Previous date | Oct 14, 2025 | Oct 14, 2025 |

SONIA OPTIONS: Latest Option trades

Nov-11 09:27

- SFIG6 96.65/96.75/96.85c fly, bought for half in 2k.

- SFIU6 97.00/97.25cs bought for 4 in 2k vs SFIU6 96.50/96.35ps, sold at 5 in 1k.