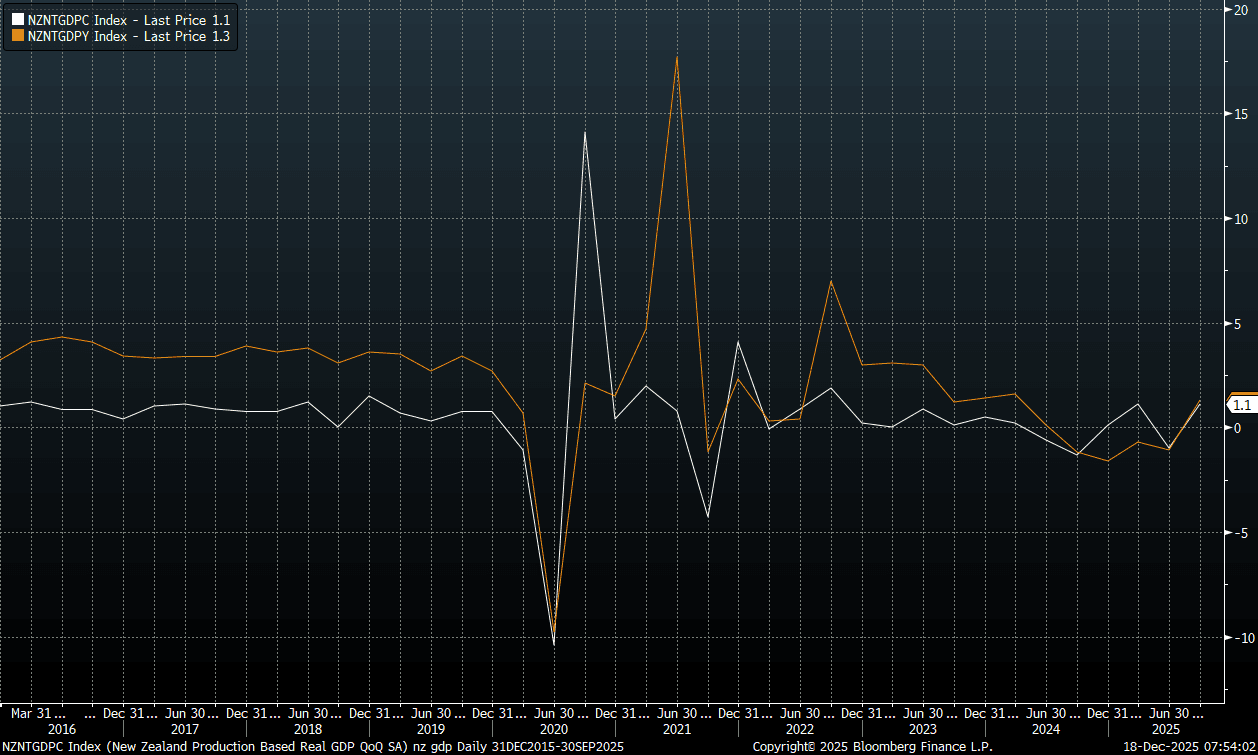

NEW ZEALAND: Q3 GDP Beats Mkt & RBNZ Forecasts, But Q2 Revised Lower

Q3 GDP rose 1.1%q/q, above the market consensus of 0.9% and well above the RBNZ forecast of 0.4%q/q. In y/y terms growth was also stronger at 1.3%, but this was in line with the consensus estimate. Q2 growth was revised lower though to a contraction of -1.0%q/q, versus the original estimate of -0.9%. The y/y outcome was revised to -1.1% from -0.6% originally reported for Q2. The lower base we are coming from is likely tempering market reaction to the Q3 GDP beat (NZD/USD couldn't sustain post data print gains above 0.5780). The chart below plots GDP growth trends in q/q (the white line) and y/y (orange line) terms.

- Stats NZ noted on the expenditure side: "Exports were up 3.3 percent, with increases in travel services, dairy, and other services, including insurance. Gross fixed capital formation, up 3.2 percent, also contributed to the rise in expenditure GDP. Household consumption expenditure rose 0.1 percent this quarter. Expenditure on durables rose 2.0 percent, while expenditure on services fell 0.1 percent and non-durables fell 0.2 percent."

- On the industry side, Stats NZ: "“The 1.1 percent rise in economic activity in the September 2025 quarter was broad-based, with increases in 14 out of 16 industries. This is in contrast to the June 2025 quarter, when GDP decreased in 10 industries.”

Fig 1: NZ GDP - Q/Q & Y/Y

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

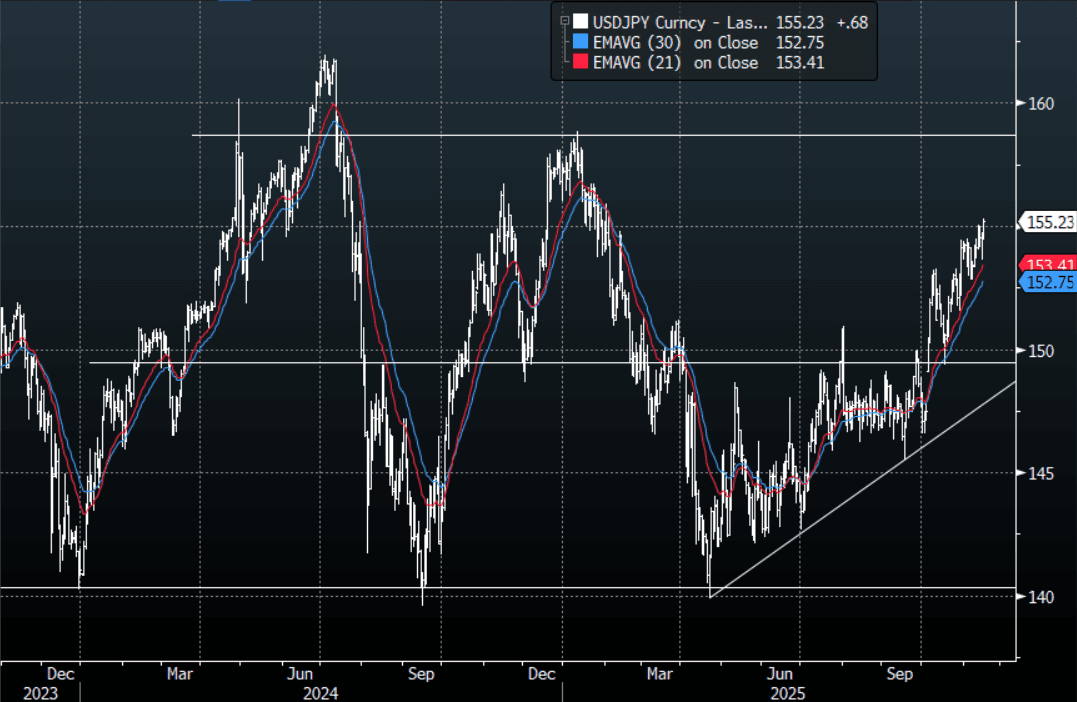

JPY: USD/JPY - Breaks Through 155.00, Can It Build On This ?

The overnight range was 154.63 - 155.30, Asia is currently trading around 155.25. The pair was quietly bid all day yesterday and then broke through 155.00 in the N/Y session. The move lower in risk did not bring the usual bout of Yen buying as its safe haven status is questioned. Usd/Jpy I suspect will remain well supported on dips as the market remains wary of the new leadership policies. I will be watching today to see if the pair can build on its move above 155.00 and regain its momentum higher, look for dips in the Asian session back toward 154.70-154.90 to be supported on dips initially.

- MNI POLICY: BOJ Prefers To Wait In Dec, Barring Yen Weakness. Sustained yen weakness toward JPY160 to the dollar would increase the likelihood that the Bank of Japan will raise rates at its final meeting this year, but much of the data Governor Kazuo Ueda wants in order to assess wage-growth momentum will not be available until at least the January meeting, MNI understands.

- MNI INTERVIEW: Fed Dec Pause Would Preserve Options - Sheets. The Federal Reserve should lean toward holding interest rates steady at its next meeting in December to continue to put downward pressure on inflation and keep its policy options open, the former director of the Division of International Finance at the Fed Board of Governors, Nathan Sheets, told MNI.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($527m). Upcoming Close Strikes : 155.00($1.34b Nov 20), 150.00{$1.3b Nov 20) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 99 Points

- Data/Event :

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA: Coming Up In Asian Markets On Tuesday

| 0300BST | 1100HKT | 1400AEDT | South Korea Q3 Household Credit |

| 0830BST | 1630HKT | 1930AEDT | Hong Kong Oct Unemployment Rate |

| China Oct FDI |

Source: Bloomberg Finance L.P./MNI

AUSTRALIA: RBA Minutes Later Today, Wages Wednesday

The key events this week are the December RBA minutes published Tuesday and Q3 WPI on Wednesday. Given the high degree of uncertainty around how restrictive policy currently is and how close the economy is to trend, any further details on the Board’s thinking are likely to be important.

- Bloomberg consensus is forecasting Q3 wages growth in line with Q2 rising 0.8% q/q and 3.4%. Public sector wage growth has been outpacing private this year.

- The Westpac leading index for October prints on Wednesday. It has been signalling growth around trend in early 2026.

- On Thursday, RBA Connolly, Head of Payments Policy Connolly participates in a panel at 1055 AEDT and Assistant Governor (Economic) Hunter participates in a fireside chat at 1300 AEDT.

- Preliminary November S&P Global PMIs are released on Friday. Services activity continues to grow while manufacturing retreated in October.