JAPAN DATA: Q2 GDP Beats, Aided By Strong Capex, Consumption Slightly Firmer

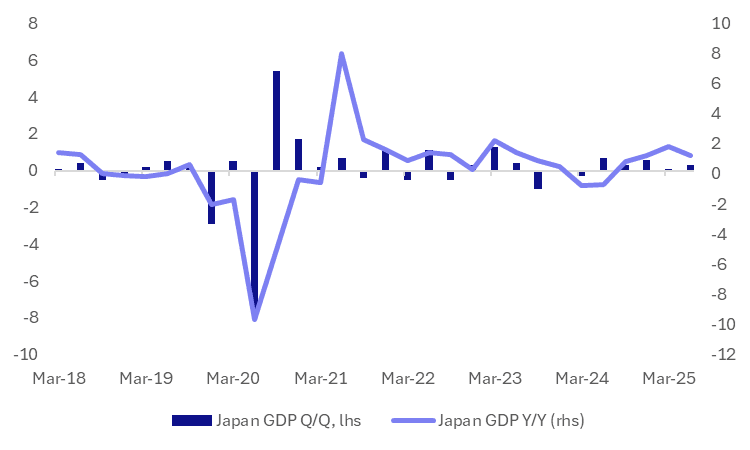

Japan Q2 GDP was better than market expectations. Q/Q growth rose 0.3%, against a 0.1% forecast, while the Q1 outcome was revised up a touch to 0.1% from the original flat estimate. In terms of the detail, private consumption rose 0.2% q/q, versus 0.1% forecast, while Q1 was revised up to 0.2% (originally reported as 0.1%). Capex was up 1.3%, versus 0.7% expected (Q1 was revised down 0.1% to a 1.0% gain). Net exports contributed 0.3% to growth (0.1% was forecast), while inventories took 0.3% off growth, in line with forecasts. Nominal GDP rose 1.3%q/q, a touch below market forecasts of 1.4%.

- The chart below plots the q/q and y/y profile for Japan GDP. Whilst not a surging picture, there were some concerns over H1 growth, particularly after Q1 printed negative in q/q terms (on an annualized basis).

- There will be caution around the H2 outlook given tariff levels, but Japan's deal with the US was seen as avoiding a worse case scenario outcome (per a recent Rtrs survey).

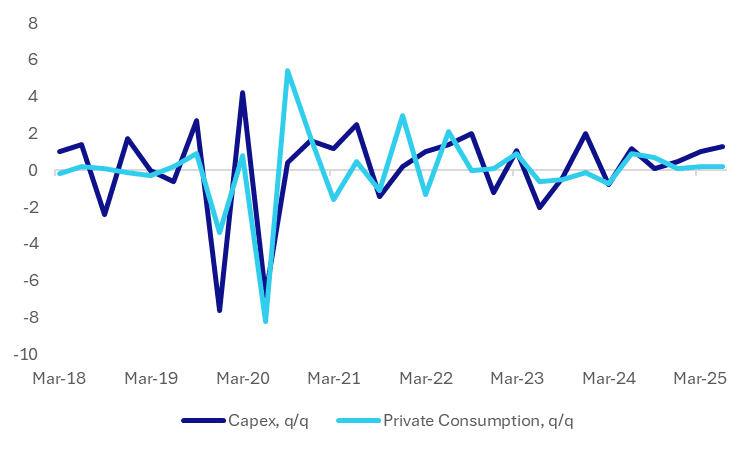

- The same survey noted the deal outcome didn't impact the capex outlook, which remains a firm source of growth for Japan, see the second chart below.

- Whilst consumption has been slightly stronger than forecast the authorities will be aiming for improving trends via continued wage gains over the next 12 months.

Fig 1: Japan GDP - Q/Q and Y/Y

Source: Bloomberg Finance L.P./MNI

Fig 2: Japan Capex And Private Consumption

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open

TYU5 is trading 110-08+, down 0-00+ from its close.

- The US 2-year yield opens around 3.945%, up 0.01 from its close.

- The US 10-year yield opens around 4.49%, up 0.1 from its close.

- (Bloomberg Economics) -- June’s CPI report showed clear signs of tariff pass-through, and Bloomberg Economics expects something similar in the month’s PPI print. Additionally, the PPI components that feed into the PCE deflator — due out July 31 — point to a much firmer reading for the Fed’s preferred inflation gauge.

- Fejau on X: “Core goods are meaningfully accelerating as of today's CPI print. Reason CPI came in within expectations was lagged core services (namely shelter) doing some heavy lifting and markets knew there's little juice left to squeeze from that. This is why the bond market sold off imo.”

- Nick Timiraos on X: “from @fcastofthemonth: "The big news in my view is that core goods prices excluding autos jumped by 0.55% in June, the largest monthly increase since November 2021."

- The 10-year yield has broken above 4.45% in response to the CPI Data, this implies price is likely to now turn its focus back to 4.65% and could see further paring back of longs. Support is now back towards the 4.35/40% area which has been the pivot in the larger 4.10% - 4.65% range.

- Data/Events: MBA Mortgage Applications, PPI, Industrial Production, Manufacturing Production

AUSSIE BONDS: AUCTION PREVIEW: ACGB Mar-36 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$800mn of the 4.25% 21 March 2036 bond. The line was last sold on 30 May 2025 for A$1200mn. The sale drew an average yield of 4.3306%, a high yield of 4.3325% and was covered 2.5792x. This new line was sold by syndication on 5 February 2025 for A$15.0bn.

- This week's ACGB supply is at the top end of the recent average weekly issuance of $1500-2000mn, with A$300mn of the 4.75% 21 June 2054 bond issued yesterday and A$1100mn of the 1.00% 21 November 2031 bond on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.

US: Trump - Bessent An Option For Fed Role, More Tariffs Likely By End July

US President Trump spoke to reporters earlier, giving wide ranging remarks on the Fed role, tariffs and aid to Ukraine.

- On the Fed Chair role, Trump stated that Tsy Secretary Bessent is an option for the post, but isn't necessarily the top option, as Trump likes the role he is doing at Tsy at the moment (per BBG).

- Trump again repeated his criticism of Fed Chair Powell, while noting: "*TRUMP SAYS POWELL RENOVATIONS 'SORT OF IS' A FIREABLE OFFENSE" - BBG.

- On trade, Trump said that the administration is working on 5-6 trade deals, with 2 or 3 probably done before Aug 1 (per BBG). Tariff payments will start on Aug 1 Trump reiterated.

- Pharmaceutical tariffs will likely start at the end of this month, and will start out low Trump said. He added that chip tariffs are on a similar timeline to pharmaceuticals.

- Trump indicated he would veer from stated tariffs in letters to countries on occasion, while smaller economies would likely receive a tariff rate a little over 10%. this would be a blanket rate.

- Trump said military aid (patriot missiles from Germany) was already flowing to Ukraine and that the EU would be paying. He added he hasn't spoken to Russian President Putin since he gave the country a 50 day deadline (before fresh sanctions are put in place) to reach a peace deal with Ukraine.

- Finally, Trump said Iran is keen to talk but that he is in no rush to do so.