EM ASIA CREDIT: Q1 Results: MISC (MISCMK, Baa2/BBB/NR) - Weaker

"*MISC 1Q Net MYR705.7M Vs. Net MYR759.9M >3816.KU" - BBG

Q1 results marginally weaker, neutral for spreads

• MISC, the Malaysian majority State owned energy logistics company, has reported Q1 operating profits down 3% YoY to RM857m, the main driver being lower earnings from the Gas Assets & Solutions business (-16% YoY) and despite a rebound from the Offshore business (+78% YoY). Neutral for spreads.

• The Gas Assets & Solutions business suffered from a decline in top line on the back of contract expiries, vessel disposals and lower charter rates, while offshore had a one-time boost from a new FPSO contract. In terms of credit metrics, leverage was marginally higher with the LTM net debt to EBITDA at 1.90x versus 1.85x end FY24.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: In positive territory for the past 5 sessions

- While the Dollar was slightly in the red overnight against G10, the Greenback is closer to flat going into the European session, down 0.16% against the NOM (at typing), and up a tiny 0.07% versus the Kiwi.

- The short term picture and looking at the past 5 days, the Swissy and the Yen have been the biggest losers, down 2.35% and 1.91% respectively.

- Medium and longer term, 1 Month, 3 Months and YTD, the Dollar remains deep in the red on Tariffs and Growth concerns in the US.

- The SEK had a quick 6 big figures move (according to Bloomberg prices) following a big drop on the PPI reading, but this was quickly reversed, with the move mostly driven by the lack of liquidity.

EQUITY TECHS: E-MINI S&P: (M5) Monitoring Resistance At The 50-Day EMA

- RES 4: 5837.25 High Mar 25 and a bull trigger

- RES 3: 5773.25 High Apr 2

- RES 2: 5622.38 50-day EMA and a key resistance

- RES 1: 5562.25 High Apr 25

- PRICE: 5528.00 @ 07:24 BST Apr 26

- SUP 1: 5355.25/5127.25 Low Apr 24 / 21 and a key support

- SUP 2: 4996.43 76.4% retracement of the Apr 7 - 10 bounce

- SUP 3: 4832.00 Low Apr 7 and the bear trigger

- SUP 4: 4760.88 1.618 proj of the Feb 19 - Mar 13 - 25 price swing

The corrective bull cycle in S&P E-Minis that started on Apr 7, remains in play. The contract traded higher last week and breached a number of important short-term resistance points. Price has cleared the 20-day EMA and pierced 5528.75, the Apr 10 high. The next key resistance is 5622.38, the 50-day EMA. A clear breach of this EMA would strengthen a bull theme. Initial key support lies at 5127.25, the Apr 21 low. A break would be bearish.

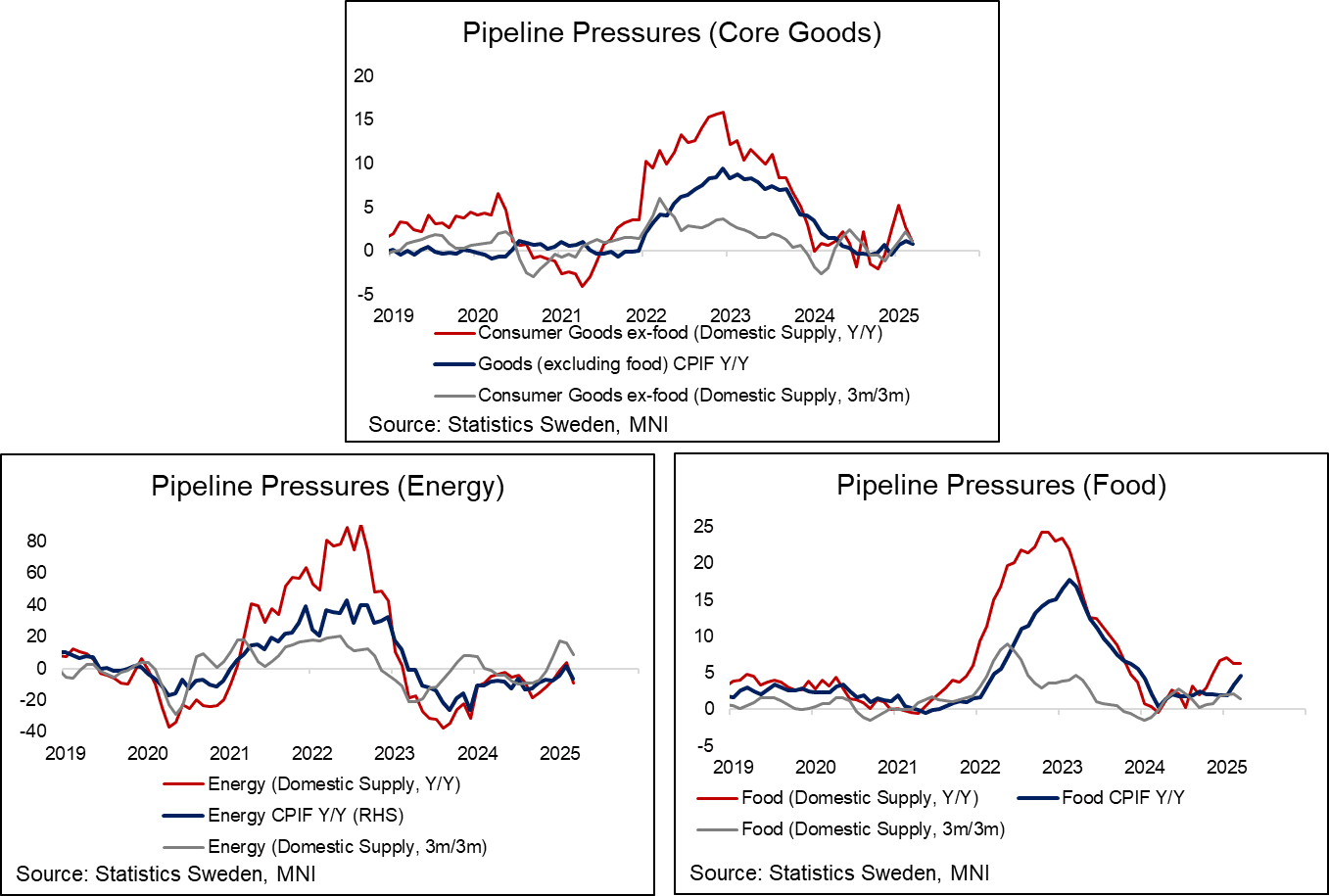

SWEDEN: Domestic Food Supply Inflation Lowest Since September

An electricity pullback and krona strength weighed on Swedish pipeline pressures in March, while a softening of food inflation will be encouraging for the Riksbank. Focus turns to tomorrow’s heavy data calendar, which includes hard data for activity at the end of Q1 and sentiment for April.

- Swedish producer prices fell 0.3% Y/Y in March (vs +3.4% prior), while the price index for domestic supply – which is a better reflection of CPI pipeline pressures – fell 0.4% (vs +2.8% prior). 3m/3m domestic supply inflation was 1.6% (vs 3.5% prior), while the ex-energy measure was 0.2% (vs 1.2% prior).

- Electricity prices were key in pulling down headline rates in March, with domestic energy supply inflation -10.9% M/M and -9.5% Y/Y (vs 4.0% prior).

- Food inflation saw the lowest monthly NSA rate since September 2024 at 0.1%, bringing the 3m/3m rate down to 1.4% (vs 2.2% prior). Food has been an important driver of higher consumer inflation this year, so this will be encouraging for the Riksbank.

- The krona effective exchange rate also strengthened 4% through March, which will have weighed on imported goods pipeline inflation.