EU REAL ESTATE: Property: Week in Review

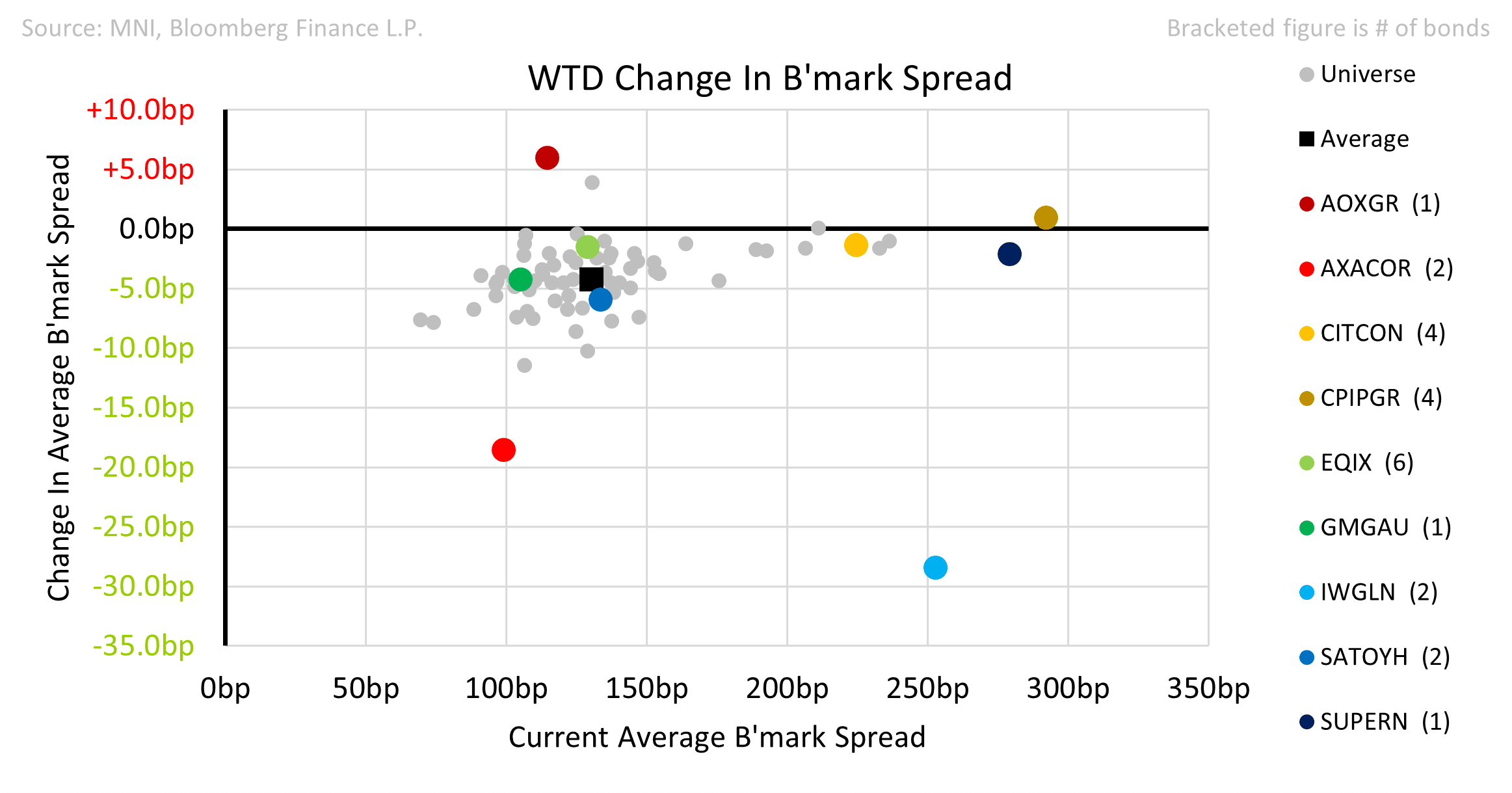

• IWG PLC hit new year-to-date highs in equity this week. The credit rallied 28bps. The company is now reporting in US$ and has migrated to US GAAP to better account for its Lease liabilities and Rental expenses. The company has been under activist pressure last year to relist completely in the US given that 50%+ of its earnings are North American.

• Equinix is likely to be a sizeable issuer of debt for the next few years: $2+bn per year. The company has brought forward CapEx plans and cut earnings forecasts during the investment period. The company has ample headroom from the agencies given its relatively low leverage vs peers. Bonds closed -1bps wtd though the overall sector was -4bps.

• Goodman announced a A$4.1bn Hong Kong data centre JV. The company has already raised $4.4bn in equity this year and in any case only owns 20% of the new JV which is largely already built. Bonds were in line at -4bps on the week.

• Sato Oyj acquired 1,000 tenanted apartments from an OP Bank fund. We assume that the GAV was <€200m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Gilt/Bunds Back Below 210bp

The 10-Year gilt/Bund spread is back below 210bp, with gilts outperforming Bunds as Tsys rally in the wake of the ADP employment data and Trump’s latest critique of Fed Chair Powell.

- The spread failed to test the April closing highs (218.8bp) in recent weeks, although the short-term fundamental and technical outlooks suggest there is a risk of further widening.

- The short-term technical outlook for Bund futures is a little more constructive than that for gilts.

- 10-Year gilt yields remain stuck in the wedge drawn off the longer-term uptrend (beginning at the December ’21 lows) and the short run downtrend drawn off the ’25 high. The benchmark last trades at 4.63%, with the boundaries of the wedge located at 4.500% & 4.788% today.

- Ongoing fiscal fragility in the UK keeps focus on the upper end of the recent range, although some speculation surrounding (a modest degree of) fiscal tightening has prevented 10-Year gilt yields from moving towards year-to-date highs (4.921%).

- Meanwhile, the market seems more at ease with the idea of fiscal loosening in Germany than it did around the time of the “whatever it takes” declaration made in early March. Two factors seem to be at play here, some believe that the size of the loosening will comfortably undershoot initial estimates & related debt issuance has not been immediate, giving the market some breathing room.

- Note that the relatively elevated gilt beta to moves in U.S. Tsys (compared to Bunds) and the complex macro environment evident at present add further layers of complexity to the outlook for the spread.

Fig. 1: UK 10-Year Gilt Yield (%)

Source: MNI - Market News/Bloomberg

CANADA DATA: Services PMI Broadly Improves In May, Though Still Contractionary

Some highlights from the S&P Global report on Canada Services PMI (link), which showed a broad improvement vs April (45.6 vs 41.5 prior):

- "Canada’s service sector contracted again during May in line with ongoing uncertainty related to tariffs and the broader macroeconomic environment."

- "Both activity and new business fell markedly, albeit at reduced rates as confidence showed some improvement compared to earlier in the year. "

- "Marginal jobs growth was also registered, which helped explain a further contraction in backlogs of work. "

- "Latest data indicated an acceleration in input price inflation and the biggest rise in output charges for a year. Tariffs remained a source of price pressures, according to service providers. "

- "Tariffs also had a noticeable effect on international sales, with new export business declining sharply again in May (albeit to the weakest degree since January)."

- "Confidence amongst service providers improved during May to its highest level since January. There were hopes that the business environment will be more stable in a year’s time and will lead to some organic business growth."

EQUITY TECHS: E-MINI S&P: (M5) Bulls Remain In The Driver's Seat

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6008.00 High May 29

- PRICE: 5985.75 @ 14:19 BST Jun 4

- SUP 1: 5850.75/5765.62 20- and 50-day EMA values

- SUP 2: 5596.00 Low May 7

- SUP 3: 5455.50 Low Apr 30

- SUP 4: 5355.25 Low Apr 24

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract is trading just ahead of its recent high. A print above 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. An extension would open 6057.00 next, the Mar 3 high. Key support lies at 5765.62, the 50-day EMA.