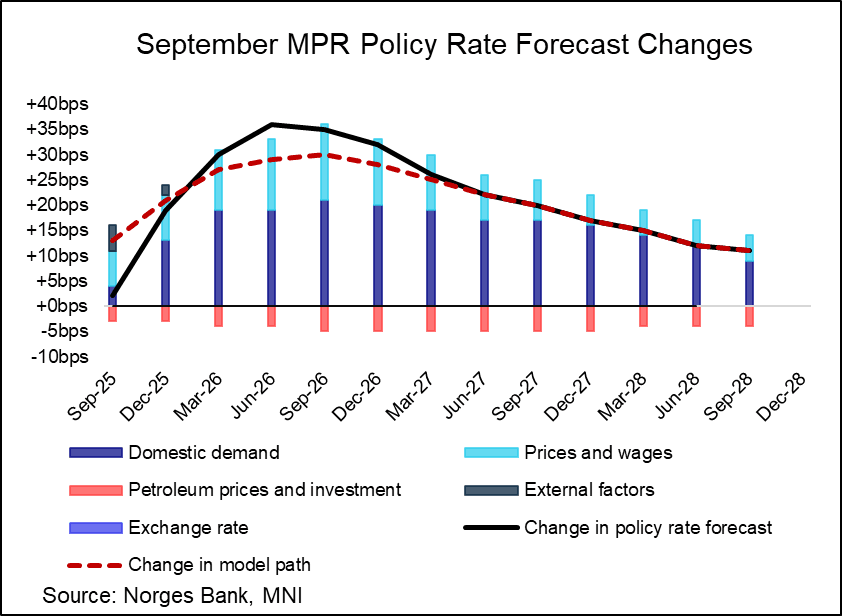

NORGES BANK: Prices and Wages And Domestic Demand Drive Rate Path Changes

As noted above, the September MPR rate path revisions were more hawkish than expected, peaking at +36bps in Q2 2026. Notably, the “judgement factor”, i.e. the difference between the model implied path and the actual MPR policy rate forecast was hawkish in 2026. Overall, the signals from the September decision feel consistent with the developments since June, even though rates were reduced. Ultimately, a cut in September and a hold in December is not really that different to the economy than a hold in September and a cut in December.

- The model implied path had called for a +13bps upward revision to the Q3 2025 rate path point, but this was tempered by the judgement factor to a +2bps revision to be consistent with today’s rate cut.

- Across components, developments were broadly as expected, with upward revisions from domestic demand and prices and wages offset a little by a downward revision to petroleum prices and investment.

- The MPR notes that “CPI-ATE inflation has been as projected in the June Report, despite the contribution to lower inflation from the reduction in daycare prices. Underlying inflationary pressure is therefore assumed to be slightly higher than envisaged in June”.

- We had thought that the impact of the child daycare policy would have been enough to tilt the Committee in favour of a hold in September, but instead this hawkish impetus was reserved for the rate path.

- Additionally, Norges Bank has revised up its wage growth projections to 4.7% in 2025 (vs 4.5% in June) and 4.2% in 2026 (vs 4.1% in June). Alongside ethe high wage outturns in H1 2025, the MPR states that “In the model, the upward revision of wage growth is explained by the upward revision of underlying productivity and a slightly higher output gap than in the June Report.”

- The MPR also notes that “Projected capacity utilisation in the Norwegian economy has been revised up slightly in the coming period” – this development is unsurprising following the solid Q2 mainland GDP report and the Q3 Regional Network Survey.

- Given productivity was revised higher in the September MPR, it implies a little less sensitivity of the rate path to a strengthening in aggregate demand going forward. In some sense, that makes the magnitude of the domestic demand revision contribution in September even more notable (i.e more hawkish than might have been assumed given productivity was revised higher).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Bund outright Call Buyer

RXX5 132c, bought for 15 in 1.2k.

FOREX: FX OPTION EXPIRY

Of note:

EURUSD 1.98bn at 1.1625 and 1.32bn at 1.1700.

USDCAD ~1bn at 1.3800 (wed).

EURUSD 1.57bn at 1.1700 (thu).

USDJPY 1.42bn at 147.90 (fri).

- EURUSD: 1.1600 (731mln), 1.1620 (411mln), 1.1625 (1.98bn), 1.1630 (219mln), 1.1665 (292mln), 1.1700 (1.32bn).

- AUDUSD: 0.6515 (745mln).

- AUDNZD: 1.0950 (302mln).

OAT: Large OAT Basis trade

OATU5 ~7.9k at 122.24.