EM CEEMEA CREDIT: PRICED: Halkbank $300m PNC5 AT1

"PRICED: Halkbank $300m PerpNC5 Reg S AT1 at Par to Yield 8.9%" - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD TECHS: Monitoring Support At The 50-Day EMA

- RES 4: $4404.9 - 3.500 proj of the May 15 - Jun 16 - 30 price swing

- RES 3: $4400.0 - Round number resistance

- RES 2: $4161.4/4381.5 - High Oct 22 / High Oct 20 and bull trigger

- RES 1: $4046.2 - High Oct 31

- PRICE: $3966.0 @ 07:28 GMT Nov 5

- SUP 1: $3886.6 - Low Oct 28

- SUP 2: $3867.3 - 50-day EMA

- SUP 3: $3800.00 Round number support

- SUP 4: $3751.3 - 50.0% retracement of the May 15 - Oct 20 bull leg

A fresh cycle low last week in Gold highlights an extension of the bear cycle that started Oct 20. The retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3867.3. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

BRENT TECHS: (F6) Corrective Phase Intact

- RES 4: $71.45 - 76.4% retracement of the Jun 23 - Oct 20 bear leg

- RES 3: $70.69 - High Jul 30

- RES 2: $69.29 - High Sep 26 and a key resistance

- RES 1: $65.98 - High Oct 9

- PRICE: $64.37 @ 07:15 GMT Nov 5

- SUP 1: $63.37/59.97 - Low Oct 24 / 20 and the bear trigger

- SUP 2: $58.72 - Low May 5

- SUP 3: $57.99 - Low Apr 9 and a key support

- SUP 4: $56.05 - 2.00 proj of the Jul 30 - Aug 13 - Sep 26 price swing

Brent futures are in consolidation mode. A short-term corrective bull cycle appears intact for now. Price has recently traded through the 50-day EMA, at $64.08. Clearance of this hurdle signals scope for a stronger recovery. The next hurdle to monitor is $65.98, the Oct 9 high. A clear breach of this level would expose a key resistance at $69.29, the Sep 26 high. Key support and the bear trigger lies at $59.97, the Oct 20 low.

GERMAN DATA: Factory Orders Recover A Little In September

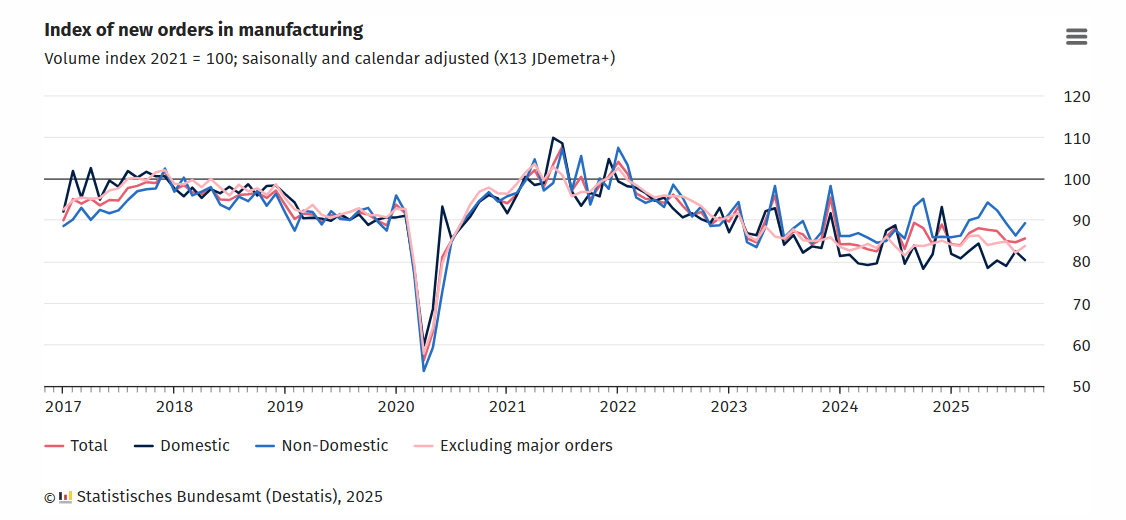

- German factory orders were a little stronger than expected in September, at 1.1% M/M amid an August upward revision to -0.4% (-0.8% unrevised). By itself, September represents some recovery in the series but not a material one considering index levels continue to print not far off cycle lows.

- "When large-scale orders are excluded, new orders were 1.9% higher than in the previous month. The less volatile three-month on three-month comparison showed that new orders were 3.0% lower in the 3rd quarter of 2025 than in the 2nd quarter; when large-scale orders are excluded, new orders were down 1.5%", Destatis comments.

- "Month-on-month increases seen in the automotive industry (+3.2%) and the manufacture of electrical equipment (+9.5%). The growth in new orders for the manufacture of other transport equipment (aircraft, ships, trains, military vehicles; +7.5%) also had a positive effect. By contrast, the decline in new orders for the manufacture of fabricated metal products (-19.0%) dragged" on drivers.

- Real turnover in manufacturing (released simultaneously with factory orders) would imply downside for tomorrow's IP vs the 3.0% M/M rebound expected (which would follow a very weak -4.3% in August partially on the back of some temporary summer factory closures). The relationship between the two prints has sometimes been a bix mixed in recent months, however.