OUTLOOK: Price Signal Summary - USDJPY Rally Exposes The Bull Trigger

- In FX, the trend in EURUSD remains bullish, however, a short-term corrective cycle is in play for now. A reversal signal on the daily chart highlights scope for a pullback - Tuesday’s candle pattern is a shooting star formation. Note that a correction would allow an overbought trend condition to unwind. The first important support lies at 1.1671, the 20-day EMA.

- A bull cycle in GBPUSD remains intact and for now, short-term weakness appears corrective. A fresh cycle high on Dec 16 reinforces the bull theme. Attention is on 1.3452 (pierced), 61.8% of the Sep 17 - Nov 4 bear leg. A clear breach of this hurdle would strengthen a bull theme and open 1.3527, the Oct 1 high. Initial firm support is 1.3297, the 50-day EMA. Clearance of this average would highlight a possible reversal.

- The trend structure in USDJPY remains bullish, highlighted by moving average studies that are in a bull-mode position. Furthermore, today’s strong gains reinforces a bullish theme with sights on 157.89, the Nov 20 high and a bull trigger. A break of this hurdle would confirm a resumption of the uptrend. Support to watch lies at 154.15, the 50-day EMA.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

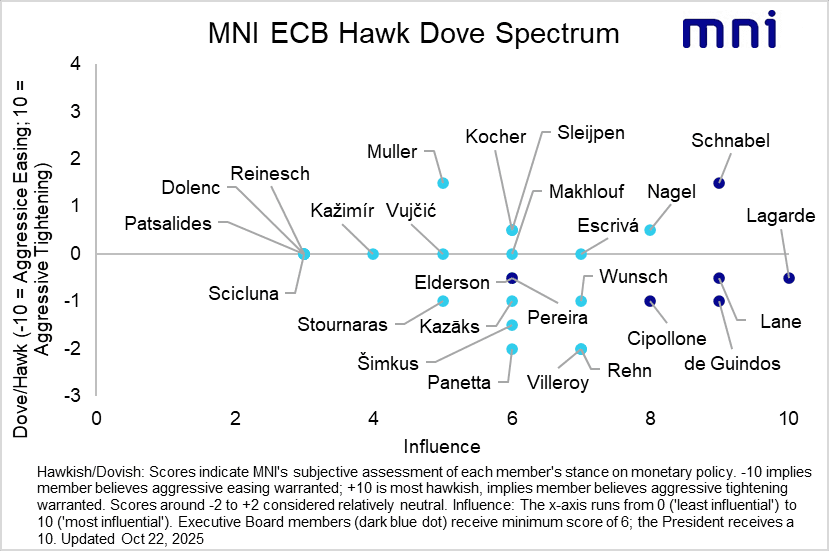

ECB: ECB Speak Wrap (Oct 31 – Nov 19) - A Few Tweaks To Hawk/Dove Matrix

The implied probability of another ECB cut this cycle has pulled back since the ECB’s October decision. OIS markets now price just 9bps of easing through September 2026 (vs ~12bps before the October decision). A combination of resilient growth signals and fairly cautious ECBspeak have factored into recent repricing, even with some Governing Council members still cognizant of downside inflation risks in the medium term.

The introduction of the EU’s ETS2 carbon pricing scheme is likely to be delayed by a year to 2028. This is expected to mechanically pull down the ECB’s 2027 inflation projection by ~0.3pp, deepening the expected undershoot of the 2% target, but policymakers have warned against relying too much on these dynamics for calibrating near-term policy.

Taking into account commentary since the October decision, we’ve made a few tweaks to our ECB hawk/dove matrix. See the full report for more

SONIA OPTIONS: Call Calendar Spread

SFIM6 96.70c vs SFIH6 96.55c, sold the June at 4.25 in 5k.

BONDS: German 5s/10s Flattener via Options

- RXZ5 129p, sold at 32 in 2k.

- OEZ5 118p, bought for 11 in 3.7k.