OUTLOOK: Price Signal Summary - Doji Reversal Candle In EURUSD

Nov-28 10:48

- In FX, the trend structure in EURUSD remains bearish and this week’s recovery appears corrective. The pair has breached both the 20- and 50-day EMAs. Key short-term resistance to monitor is 1.1656, the Nov 13 high and a bull trigger. Clearance of this level would highlight a reversal. Note that yesterday’s candle pattern is a doji - a potential reversal signal. A resumption of weakness would open key support at 1.1469, the Nov 5 low.

- The trend theme in GBPUSD is bearish and short-term gains appear corrective. Price has breached the 20-day EMA and pierced the 50-day EMA, at 1.3260. A clear break of the 50-day average would highlight a stronger bull theme. Moving average studies are in a bear-mode condition, highlighting a dominant downtrend. 1.3010, the Nov 4 / 5 low, is the trigger for a resumption of the bear leg. Note that yesterday's pattern is a doji - a bear reversal signal.

- The trend set-up in USDJPY is bullish and the latest shallow pullback appears corrective. The pair has recently entered overbought territory and a deeper retracement, if seen, would allow this condition to unwind. Support to watch is 155.16, the 20-day EMA. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. A resumption of the trend would open 158.00.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

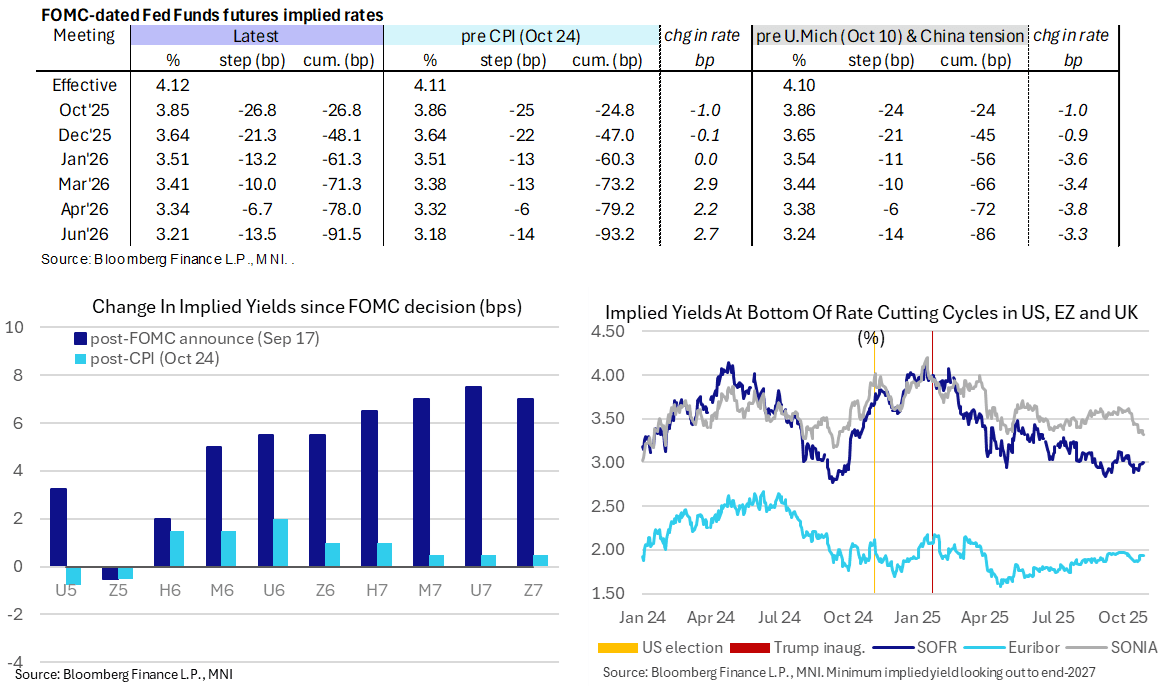

STIR: Fed Rates Marginally More Hawkish Again With FOMC Ahead

Oct-29 10:41

- Fed Funds implied rates have extended yesterday’s modest climb in London trading, where, aside from today’s expected 25bp cut, implied rates are 1.5-2.5bp higher on the day out to mid-2026.

- The moves could be a combination of pre-FOMC positioning and headlines on the Trump-Xi meeting going ahead mid-morning tomorrow, later suggested it could last for three hours.

- Cumulative cuts from 4.12% effective (after Monday’s latest push higher): 27bp Oct, 48bp Dec, 61.5bp Jan, 71.5bp Mar, 78bp Apr, 91.5bp Jun.

- SOFR futures are only 0.5-1 tick lower on the day when looking out to end-2027.

- It leaves the terminal implied yield unchanged at 2.995% after yesterday’s close nudged to a fresh high since Oct 9, i.e. prior to the increase in US-China trade tensions on Oct 10.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Oct2025_With_Analysts_2c9e326366.pdf

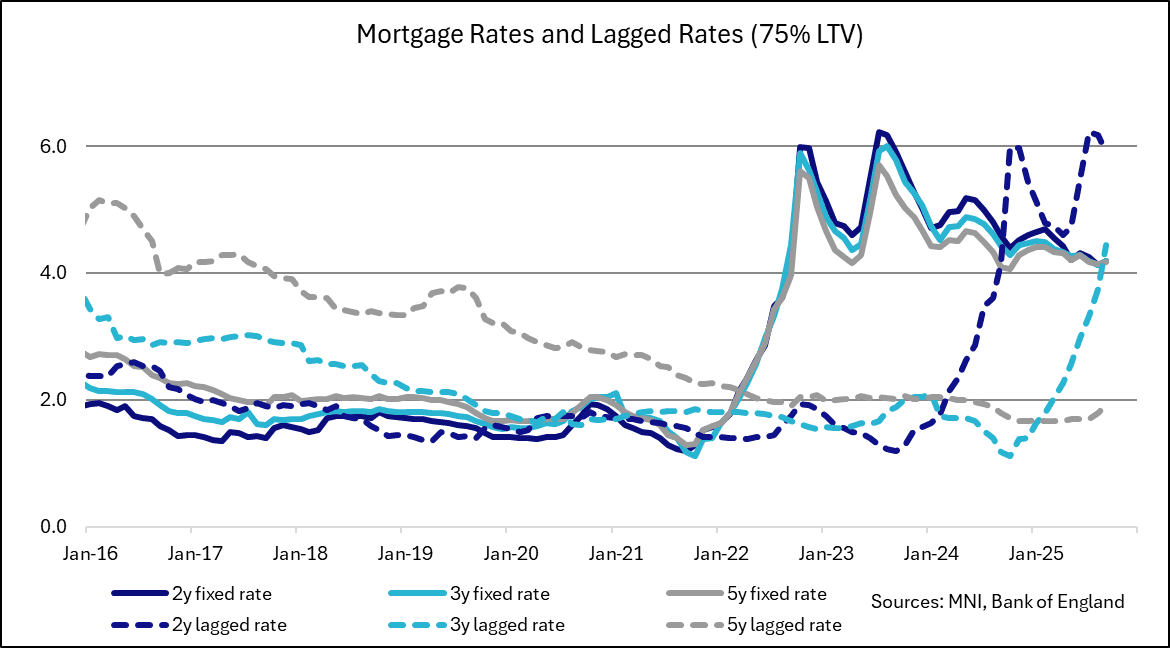

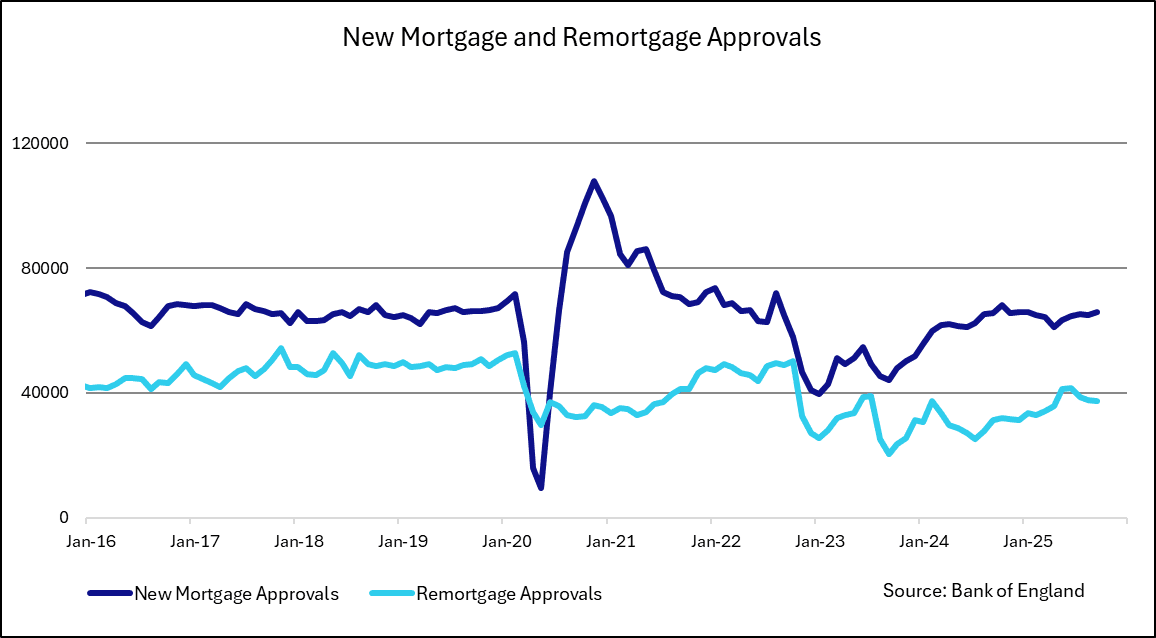

UK DATA: BOE Lending Data on the Stronger Side of Expectations

Oct-29 10:37

BOE money and credit data for September look on the stronger side of expectations and are broadly in line with previous post-COVID Septembers. Both mortgage approvals and secured lending came in higher than August. Also in the release, M4 money supply increased at a faster rate than in August.

- New mortgage approvals came in at 65.9k, above consensus of 64.0k and up from August's upwardly revised 65.0k. Readings broadly in line with this level have been seen for around a year (with the exception of the volatility around the stamp duty changes).

- Net lending on dwellings also increased, coming in at GBP5.49bln vs 4.31bln in August.

- The key takeaway on the mortgage rates is that those remortgaging from a 5-year rate will still see a big increase in payments, those remortgaging from a 2-year rate will see a fall and those remortgaging from a 3-year rate will see payments broadly in line with their previous terms.

- The average fixed rate on a 3-year (75% LTV) mortgage rose slightly to 4.19%, that it is now below the same rate 3 years ago (4.45%). This is the first time it has been below the 3-year lagged rate since early 2022 so those re-mortgaging from a 3-year rate on to another 3-year rate will see lower mortgage payments.

- Net consumer credit was almost exactly in line with consensus, at GBP1.49bln vs 1.5bln cons, though down from 1.69bln in August.

- Also in the release, M4 money supply growth rose to 0.6% M/M, 3.6% Y/Y (vs 0.4% M/M, 3.4% Y/Y August).

EQUITY OPTIONS: EU Bank Call Fly

Oct-29 10:33

SX7E (21st Nov) 237/242/247c fly, bought for 1.3 in 5k.