OUTLOOK: Price Signal Summary - Bear Threat In Oil Futures Still Present

Jan-08 11:57

* On the commodity front, the trend structure in Gold is unchanged, it remains bullish and a sharp...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: /SWAPS: ING Remain Remain Of Further EUR Steepening

Dec-09 11:48

ING remain wary of the risks of a further extension higher in EUR long end yields and swap rates, noting that “whilst the move up in rates happened sooner than we anticipated, we do think higher rates are justified from a structural perspective”.

- They flag that “the growth outlook for 2026 looks decent, whilst from a supply perspective we should also get more upward pressure. Germany’s funding announcement is likely next week and in January we expect plenty of frontloading of funding plans, both placing supply in focus for the coming weeks. In between, around EUR600bn of Dutch pension fund assets will transition to a new system, drastically reducing the amount of longer-dated swaps and bonds needed”.

- ING continue to argue that “the front end has little room to go higher for now, given more inflation data is needed before seriously contemplating a rate hike. The 10-Year swap rate, however, could still move higher as term premium builds. 2s10s is still relatively flat compared to the average of 80bp since 2000. One could also look at long-term nominal growth expectations as an anchor for longer rates. In that case, having the 10-Year swap rate settle around 3.0-3.5% would be considered fair value”.

OPTIONS: Expiries for Dec09 NY cut 1000ET (Source DTCC)

Dec-09 11:47

- EUR/USD: $1.1585-90(E1.7bln), $1.1600(E755mln), $1.1675(E784mln), $1.1760(E1.3bln)

- EUR/GBP: Gbp0.8785-92(E530mln)

- AUD/USD: $0.6330-35(A$1.2bln)

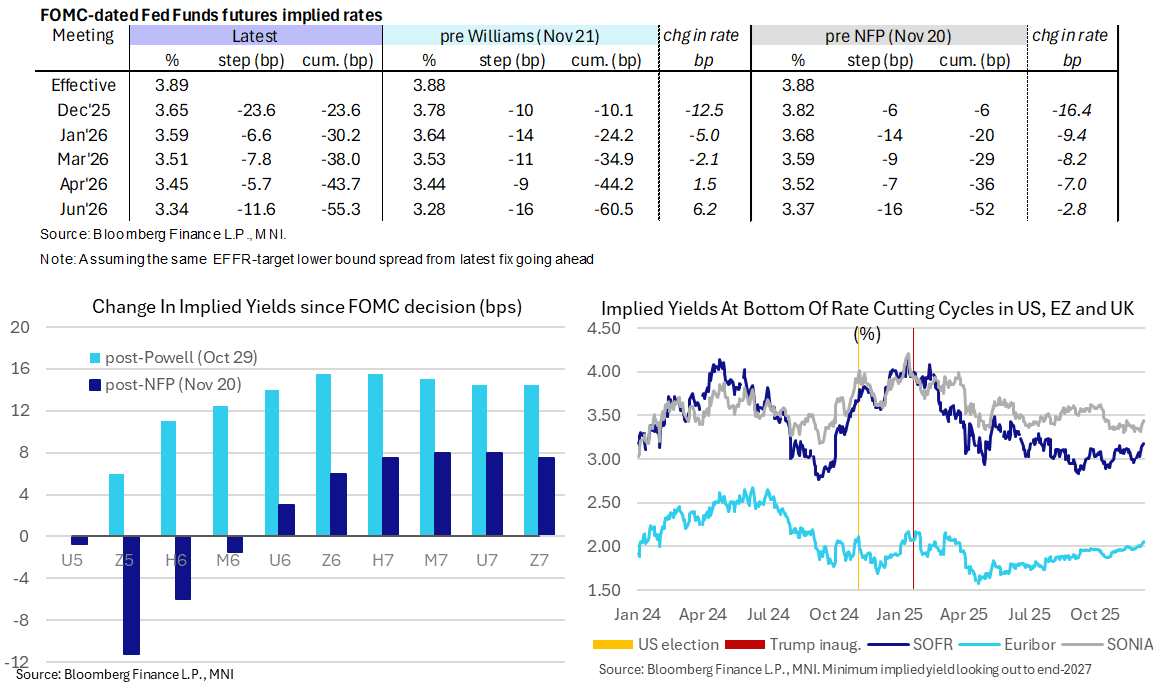

STIR: Terminal Fed Yield Highest Since July Day Out From FOMC Decision

Dec-09 11:46

- Fed Funds implied rates are unchanged on the day, broadly set up for a hawkish Fed cut tomorrow with 23.5bp of cuts priced but then a next fully priced cut not seen until June.

- Today labor data in focus, with the return of weekly ADP tracking after the full monthly report last week before two months of JOLTS data later.

- Cumulative cuts from 3.89% effective: 23.5bp Dec, 30bp Jan, 38bp Mar, 43.5bp Apr and 55.5bp Jun.

- SOFR futures have pared earlier losses and are mostly 0.5-1 tick firmer today looking out to end-2027. It consolidates a sizeable hawkish shift further out the curve in the past three working days, with the implied terminal yield at 3.175% (H7) after yesterday’s 3.18% was the highest close since July.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Dec2025_With_Analysts_4d5a318a2b.pdf