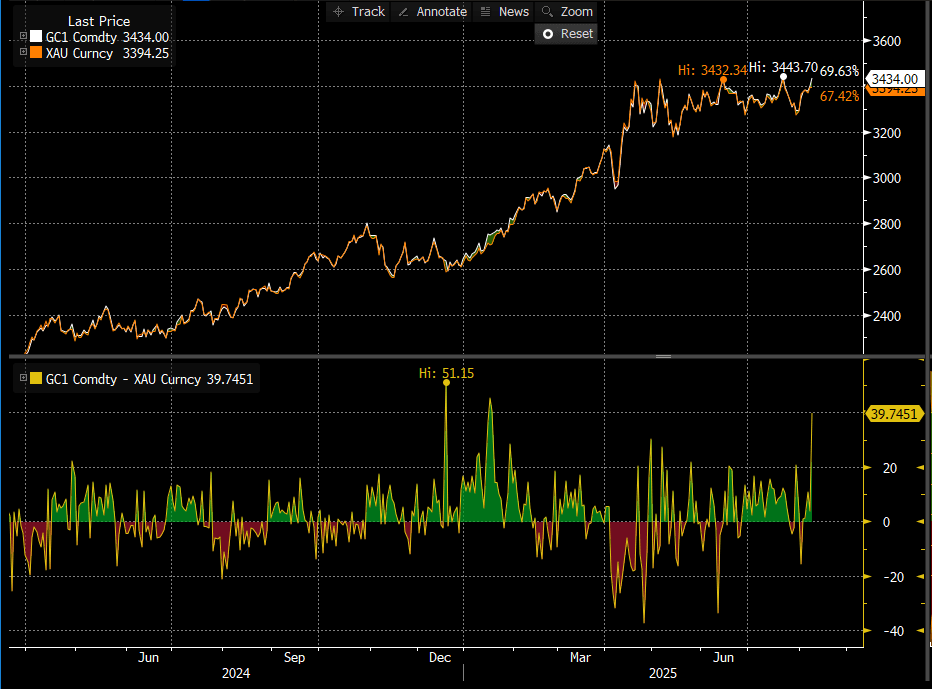

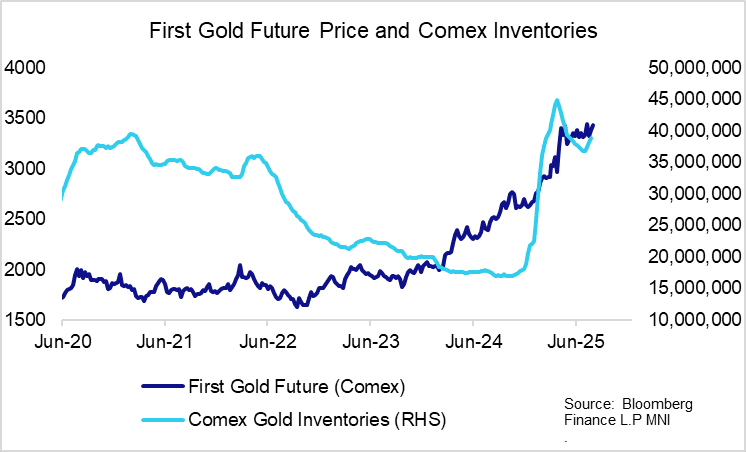

GOLD: Premium Of Front Gold Future Over Spot At Highest Since Jan

The premium of the first COMEX Gold future over London spot prices has risen to $40, the highest since January. The move comes after an FT report signalling US imports of gold bars from Switzerland would be subject to the recently announced 39% tariffs, potentially hampering the supply of physical gold into the US. The front gold future is up 1% today, with USD/oz spot prices down 0.1% at ~$3,390/oz. Exporters and market participants had expected gold to be exempt from the Swiss tariffs, particularly after metals were excluded from the original US reciprocal tariff list back in April.

- The COMEX/Spot premium reached a high of $51 in December, with participants attempting to front-run anticipated tariffs by moving Gold from London into New York, via Switzerland. This was reflected in a sharp rise in COMEX gold inventories through Q1. However, this premium evaporated and COMEX inventories fell back after metals were exempted from the initial April tariff list.

- With 39% tariffs on Swiss exports now in force, it seems unlikely that the latest widening of the COMEX/Spot premium will be matched by an uptick in Comex Gold inventories to the extent seen in Q4/Q1.

- Gold continues to benefit from the soft NFP print last Friday and broad USD weakness across the week. This has returned spot prices toward the top-end of the recent range and narrows the gap to support at $3,439 (Jul 23 high). Technically, the bull cycle that started on June 30 remains intact.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Westpac See Merit in Sticking with Core AUD Longs

- AUDUSD has been holding onto a portion of the post RBA advance on Tuesday, consolidating around current spot levels of 0.6535 as we approach the NY crossover and maintaining the bullish trend set-up for the pair. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend, and scope is still seen for a climb towards 0.6603 next, the Nov 11 high.

- AUDJPY has broken above resistance at 95.75 and strength overnight saw the cross trade up to 96.22, potentially signalling scope for a stronger rally towards the February highs at 97.33. Uncertainty regarding a US/Japan trade deal and a market that remains long JPY could strengthen a short-term extension of the rally.

- Westpac see merit in sticking patiently with core AUD/USD longs, looking for an eventual sustained break beyond 0.6590 resistance. Renewed tariff risks admittedly triggered an uncomfortable reset on 7 July, but overall, the pair is still in good shape and Westpac moderately upgrade their 1m target to 0.6625 (vs 0.6600).

- In similar vein, Westpac would not stand in the way of a bullish wave enveloping cross/JPY. AUDJPY downside over the next month is likely limited to the 94.80 area with potential upside extending as far the 97.50-98.00 area. There is next to no chance for any BoJ rate hikes while Japan tariff risks (25% starting 1 Aug) remain in place, while upcoming Upper House elections (20 July) make it politically challenging to settle on a deal that gives the US concessions.

OUTLOOK: Price Signal Summary - EUROSTOXX50 Futures Approach The Bull Trigger

- In the equity space, the trend condition in S&P E-Minis remains bullish and the contract is holding on to the bulk of its recent gains. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This was followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a 1.236 projection of the May 23 - Jun 11 - 23 price swing. Key support is at the 50-day EMA, at 6021.70.

- EUROSTOXX 50 futures are trading higher today as the contract extends the recovery that started Jun 23. This strengthens a bullish condition and exposes key resistance and the bull trigger at 5486.00, the May 20 high. Clearance of this level would confirm a resumption of the medium-term bull cycle that began Apr 7. A break would open the 5500 handle. On the downside key support has been defined at 5194.00, the Jun 23 low.

US TSY FUTURES: Mix Of Short Setting & Long Cover Seen On Tuesday

OI data points to a mix of net short setting and long cover during Tuesday’s downtick in futures, with the most meaningful net positioning swings coming via net short setting in TU futures and net long cover in FV futures.

| 08-Jul-25 | 07-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,354,026 | 4,285,962 | +68,064 | +2,590,500 |

FV | 7,007,587 | 7,034,656 | -27,069 | -1,166,321 |

TY | 4,920,369 | 4,933,087 | -12,718 | -837,542 |

UXY | 2,416,310 | 2,420,925 | -4,615 | -401,207 |

US | 1,830,260 | 1,835,915 | -5,655 | -777,081 |

WN | 1,960,908 | 1,957,874 | +3,034 | +551,120 |

|

| Total | +21,041 | -40,530 |