US DATA: PPI Price Pressures Pick Up Strongly Across Board In July

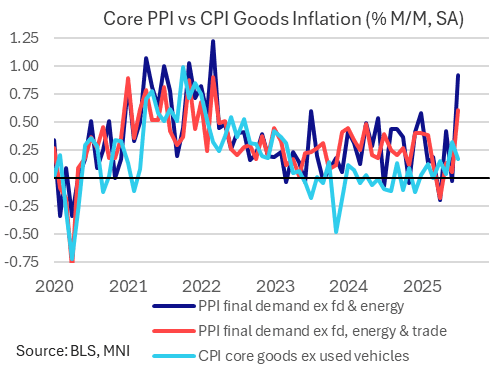

July's Producer Price Index report was one of the strongest in years on a month-to-month basis in the major core aggregates. In contrast to this week's more benign core goods CPI reading than was expected, this will reignite concerns that tariffs will increasingly feed through to consumer prices in the months ahead.

- The headline PPI reading of 0.9% M/M greatly exceeded expectations (0.2%), with ex-food/energy (0.9% vs 0.2%) and "core" ex-food/energy/trade (0.6% vs 0.2%) likewise well to the upside. All had been flat M/M in June, though among revisions, June's core figure was nudged up 0.1pp to mark a positive reading (+0.05% M/M unrounded). For all three categories, this was the highest M/M PPI reading in 40 months.

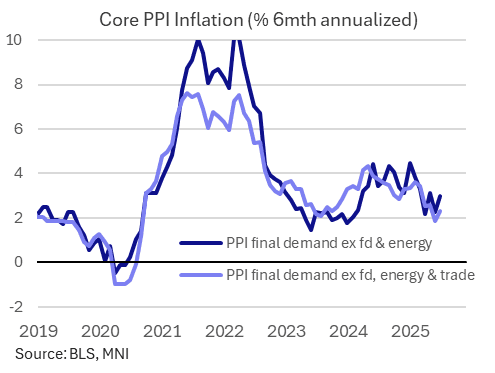

- While all three had seen slowing momentum over the last several months, this print has singlehandedly started to reverse the trend: the 6-month annualized moving average core PPI rose to 2.3% from 1.9% (which had been a 57-month low), with the 3-month measure up to 3.2% from 0.0%. To be sure these are still relatively behaved (Y/Y was 2.8%), but another month close to this in August will see the tide turn decisively.

- The potentially tariff-related details are worrisome depending on where you look, but overall both services and goods saw outsized price rises.

- Final demand services prices rose 1.1% M/M (-0.1% prior), the fastest since March 2022. The report notes that more than 30% of the rise in prices for final demand services was due to margins for machinery and equipment wholesaling (+3.8%), with trade services +2.0% overall (highest since March 2022) though some of the notorious imputed volatile services prices such as portfolio management/investment advice also played a part (though only added around 0.1-0.2pp to total PPI), and furniture retailing prices fell.

- And in final demand goods, one-quarter of the 0.7% M/M rise (fastest since January, and vs 0.3% prior) was due to higher vegetable prices. The core (ex-food/energy) reading of 0.4% was an advance from 0.2% prior and the fastest since January 2023.

- PPI finished goods rose a fairly non-descript 0.5%, but PPI finished services - which has at times correlated well to "supercore" inflation - rose 1.0%, easily the fastest since March 2022. This may be seen as a sign that wholesale price inflation is close to spilling over into consumer price categories, though again overall momentum doesn't appear to be worrisome unless confirmed by another hot/warm print in August.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Fed Pricing A Little More Dovish After CPI Took Edge Off Bessent's Comment

Fed pricing sees a modest dovish reaction to the CPI data, although the readings provided little differentiation vs. headline BBG survey expectations on net (but did include a 0.1ppt downside surprise for unrounded M/M core CPI & a 0.1ppt upside surprise for unrounded headline CPI).

- Unrounded supercore was pretty close to the average of a limited survey sample, with our macro team noting that it was core services that limited inflation, while core goods provided a slightly hawkish surprise (see previous bullets for greater details on the release)

- A reminder that hawkish adjustments were seen ahead of the data, after Treasury secretary Bessent’s left some feeling that there may have been a more hawkish surprise in the offing.

- We suggested that he may have just been referring to a roughly in-line print given consensus expectations for a move higher across the major CPI metrics vs. May levels. This seems to have been proven true.

- FOMC-dated OIS shows 1bp of easing for this month’s decision, 16bp through September, 31bp through October and 47bp through year-end.

- That compares to 1bp, 15bp, 29bp and 46bp ahead of the data and 1bp, 17bp, 31bp and 49bp before Bessent spoke.

- SOFR-implied terminal rate pricing at 3.22% vs. 3.25% ahead of the data and 3.23% pre-Bessent (corrected from 3.33% when previously published).

STIR: Fed Pricing A Little More Dovish After CPI Took Edge Off Bessent's Comment

Fed pricing sees a modest dovish reaction to the CPI data, although the readings provided little differentiation vs. headline BBG survey expectations on net (but did include a 0.1ppt downside surprise for unrounded M/M core CPI & a 0.1ppt upside surprise for unrounded headline CPI).

- Unrounded supercore was pretty close to the average of a limited survey sample, with our macro team noting that it was core services that limited inflation, while core goods provided a slightly hawkish surprise (see previous bullets for greater details on the release)

- A reminder that hawkish adjustments were seen ahead of the data, after Treasury secretary Bessent’s left some feeling that there may have been a more hawkish surprise in the offing.

- We suggested that he may have just been referring to a roughly in-line print given consensus expectations for a move higher across the major CPI metrics vs. May levels. This seems to have been proven true.

- FOMC-dated OIS shows 1bp of easing for this month’s decision, 16bp through September, 31bp through October and 47bp through year-end.

- That compares to 1bp, 15bp, 29bp and 46bp ahead of the data and 1bp, 17bp, 31bp and 49bp before Bessent spoke.

- SOFR-implied terminal rate pricing at 3.22% vs. 3.25% ahead of the data and 3.23% pre-Bessent (corrected from 3.33% when previously published).

SOFR OPTIONS: BLOCK: Dec'25 SOFR Call Condor

- 10,000 SFRZ5 96.25/96.50/96.75/97.00 call condors, 4.0 net ref 96.125 at 0857:04ET