US DATA: PPI Input Cost Pressures Fade After Inventory Build

May-15 13:29

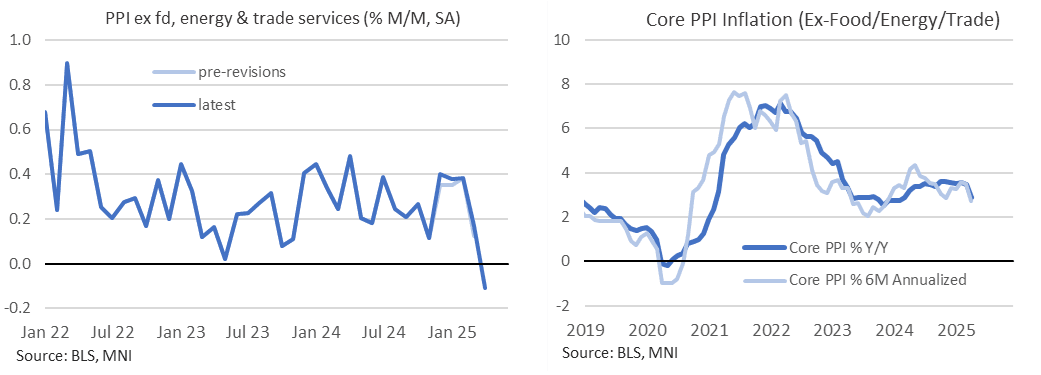

- Core PPI (ex food, energy & trade services) inflation was surprisingly soft at 0.11% M/M (cons 0.3) after only a slightly upward revised 0.17% (initial 0.12) in March.

- Rather than showing input costs kicking higher with the implementation of reciprocal tariffs in April, the pattern of recent weakness in March and April after some strength through Dec-Feb (when it averaged 0.39% M/M) suggests tariff front-running was more inflationary.

- One important caveat here is the strong inventory build seen over this period, which delays the need for immediate price increases (especially with anecdotal stories of increased use of bonded warehouses to delay tariff charges).

- Nevertheless, for now at least, input cost inflation momentum has slowed to 1.8% annualized over three months for its slowest rate since Jun 2023, as is the Y/Y of 2.87%.

- Note that we prefer this series to the alternate core of just ex food & energy as trade services is an extremely volatile imputed series and one that is prone to large revisions (it printed -1.6% M/M in Apr after March was revised from -0.7% to +1.4%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: US Cash Opening calls

Apr-15 13:24

SPX: 5,412.8 (+0.1%); DJIA: 40,526 (+0.0%/+2pts); NDX: 18,838.3 (+0.2%).

FED FUNDS FUTURES: BLOCK: Large Apr'25 FF Buy

Apr-15 13:24

- +20,000 FFJ5 95.6725, post time offer at 0919:12ET, the April serial contract trades 95.6725 last (-.0025)

US TSY FUTURES: BLOCK: Jun'25 10Y Ultra Bond Buy

Apr-15 13:22

- +5,458 UXYM5 112-29.5, buy through 112-26 post time offer at 0905:00ET, DV01 $480,000. The 10Y ultra contract trades 112-30 last (-4).