FED: Powell Restores FOMC's December Decision Optionality Amid Divisions (1/2)

The Fed’s October 29 policy decisions were more or less as expected, with the Fed funds rate range cut by 25bp for a 2nd consecutive meeting to 3.75-4.00%, and an announcement that quantitative tightening would end imminently.

- However, there was a significant surprise as Chair Powell began the post-meeting press conference by highlighting the FOMC’s divisions on the way forward: "in the Committee's discussions at this meeting, there were strongly differing views about how to proceed in December. A further reduction in the policy rate at the December meeting is not a foregone conclusion, far from it. Policy is not on a preset course."

- With markets having come into the meeting expecting a follow-up cut in December as nearly a done deal, this led to a sharp hawkish reaction across rates and FX. There are now roughly 16bp of cuts priced for December vs 22.5bp (nearly a foregone conclusion) pre-meeting.

- The reaction was only reinforced by Powell’s reiteration of the theme of FOMC division over prospects for a December cut: “there's a growing chorus now of feeling like maybe this is where we should at least wait a cycle, something like that”, highlighting that the meeting minutes release in 3 weeks would offer some more color on the internal debate.

- “We had 19 participants on the committee…And at a time when we have tension between our two goals, we have strong views across the Committee. And as I mentioned, they were strongly different views today. And the takeaway from that is that we haven't made a decision about December, and you know, we're going to be looking at the data that we have, how that affects the outlook and the balance of risks. And I'll just say that…I always say that it's a fact that we don't make decisions in advance, but I'm saying something in addition here - is that it's not to be seen as a foregone conclusion. In fact, far from it."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

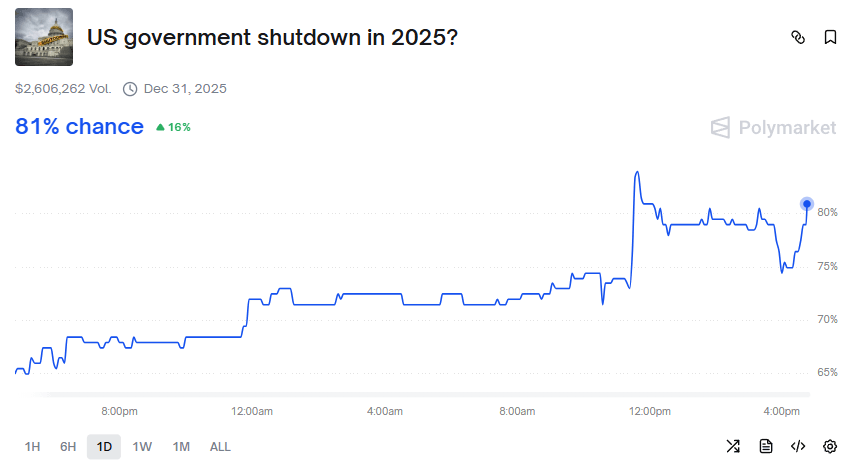

US: VP Vance: Think We're Headed To A Government Shutdown

The Democratic congressional leadership's meeting with the White House has concluded, some headlines that suggest only limited if any progress has been made toward avoiding a federal government shutdown on Oct 1. Limited financial market reaction (equity futures dip slightly) but prediction markets' implied probabilities of a shutdown are beginning to pick up (Polymarket back over 80%). Some selected Bloomberg headlines:

- "*SCHUMER: WE MET WITH TRUMP, WE HAVE LARGE DIFFERENCES"

- "*VANCE: I THINK WE'RE HEADED TO A GOVERNMENT SHUTDOWN"

- "*JOHNSON: IF DEMOCRATS DECIDE TO SHUT DOWN GOV, IMPACT'S ON THEM"

FED: Deputy SOMA Manager Eyes Signals Of Reserve Regime Shift

Deputy SOMA Manager Remache of the NY Fed commented today at an annual meeting with primary dealers that system reserves appear to be "still abundant".

- "Our indicators currently suggest that reserves are still abundant. But we have observed some firming of repo rates recently, in part due to the increase in bill supply after the debt ceiling resolution, and continued pressures are likely over time given ongoing Fed balance sheet reduction. We have also started to see some movement in the distribution of federal funds transactions in response to higher repo rates—which is a healthy sign of market linkages, and exactly what we would expect. Most recently, this has translated to a one-basis-point increase in the EFFR relative to IORB."

- The Standing Repo Facility has been effective so far: "The SRF has been much less extensively used than the ON RRP to date, since reserves have been abundant over recent years. But as reserve levels fall this is shifting somewhat, with the SRF used at the recent June quarter end and at the mid-September tax date. On those occasions it worked consistent with its design, providing funds into the market when market rates rose above the SRF minimum bid rate. By doing so, the SRF can stem incipient rate pressure that, if left unaddressed, could threaten rate control."

- However: "Observing a more substantial shift in the EFFR relative to IORB, and changes in our set of reserve ampleness indicators, would be consistent with transitioning from abundant toward a more ample level of reserves. The Committee has indicated that it will consider stopping balance sheet runoff when we reach that point...When market conditions suggest reserves are ample, we will provide those liabilities by beginning to grow our balance sheet once again. At that point, the Committee would direct the Desk to resume purchases of Treasuries for the SOMA portfolio to maintain an ample level of reserves."

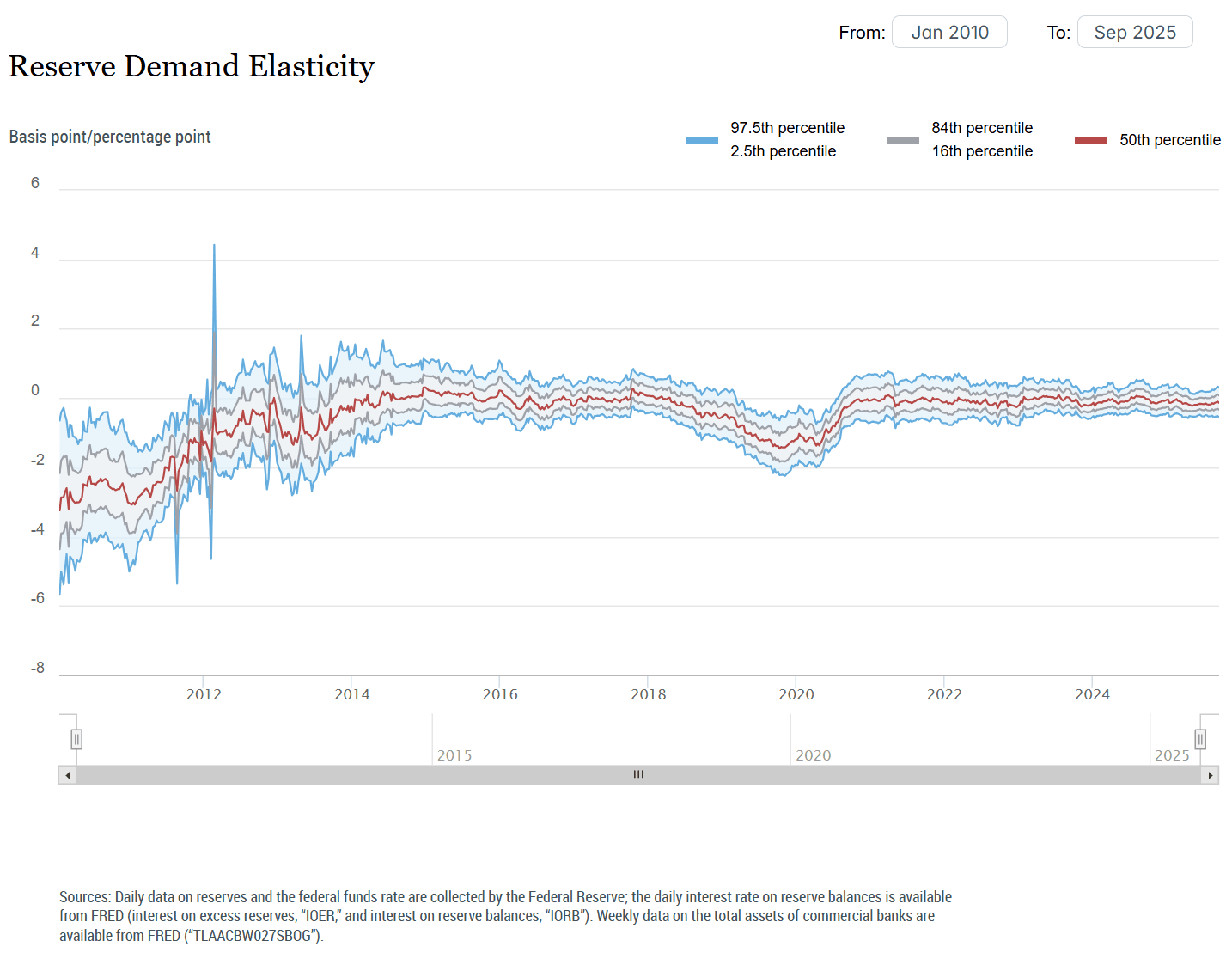

- The NY Fed's latest Reserve Demand Elasticity (RDE) indicator only goes through September 19 but suggests limited pressure through that period (the September update: "The elasticity of the federal funds rate to reserve changes is very small and statistically indistinguishable from zero. The estimate suggests that reserves remain abundant."

USDCAD TECHS: Northbound

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3968 High May 20

- RES 1: 1.3959 High Sep 26

- PRICE: 1.3920 @ 16:19 BST Sep 29

- SUP 1: 1.3885/3805 Low Sep 25 / 50-day EMA

- SUP 2: 1.3727 Low Aug 29 and a bear trigger

- SUP 3: 1.3689 Low Jul 28

- SUP 4: 1.3637 Low Jul 25

Last week’s rally in USDCAD cancels a recent bearish theme and instead strengthens a bullish outlook. The pair has breached a key resistance at 1.3925, the May 20 high and bull trigger. The breach confirms a resumption of the bull cycle that started Jun 16. This paves the way for a climb towards 1.4019, a Fibonacci retracement point. On the downside, first key support lies at 1.3805, the 50-day EMA.