FED: Powell Comfortable With Asset Runoff Pace (1/2)

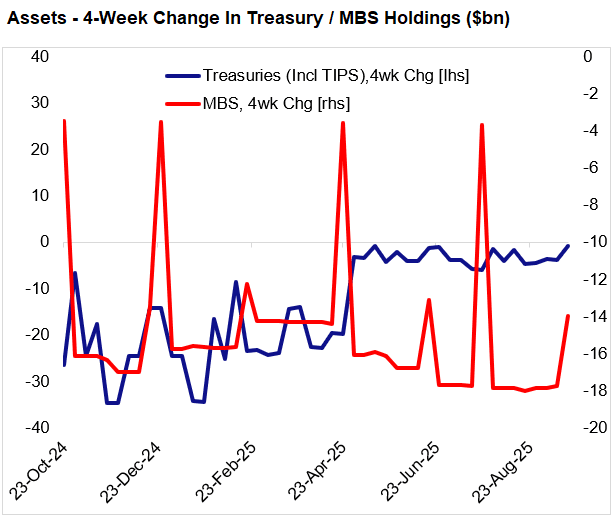

Fed asset holdings in the week to Wednesday Sept 17 were relatively steady, according to the Fed's latest weekly H.4.1 release.

- There was only a modest $2.6B increase in the latest week, with a $0.4B reduction in lending/liquidity facility takeup and $0.1B fall in MBS holdings offset by a $3.1B rise in "other" (this category is primarily unamortized premiums on securities and Treasury currency outstanding).

- The pullback in lending facility take up was entirely from the Pandemic 13-3 Program categories, of $0.5B, offset by a slight uptick in Discount Window usage ($0.2B to $5.5B). The latter is up $1.1B in the last month but still below July highs above $6B.

- There was no change to nominal Treasury holdings, with QT running at a slower-than-usual $16B clip over the last month ($1.8B Treasuries, $14B MBS), vs the average $20B ($5B Tsys cap, $15B MBS).

- Asked at the September FOMC press conference why the Fed is continuing to shrink its balance sheet even as it resumes its rate cut cycle (two policies which, we should note, are not incompatible), Chair Powell said: "we're cutting the size of our balance sheet quite marginally now. As you know, with the balance sheet, we're still in an abundant reserves condition. And we've said that we would stop somewhat above an ample reserves level. That's where we are. And we're ... getting closer to that. We're monitoring it very carefully. We don't think that that has at all significant macroeconomic effects. These are pretty small numbers moving around inside a giant economy. You know... the level of runoff is not very large. So I wouldn't attribute macroeconomic consequences to that, at this point."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

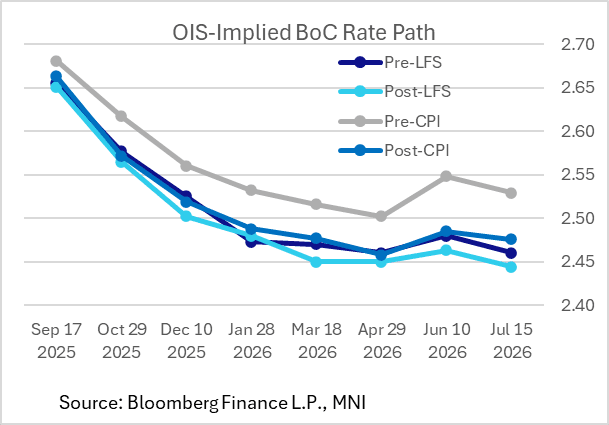

BOC: Implied Cuts Increase Post-CPI, But Still Some Data To Go Before September

The implied BOC rate path shifted lower following the July CPI data, with about 4bp in cuts added by year-end and improving the probability of a September rate cut to around 36% from 28%. The first full 25bp cut is cumulatively priced by January, vs (not quite) March as seen pre-CPI.

- The two key pieces of data since the July decision - the other was the July Labour Force Survey - have thus each received a dovish reaction, even if implied rates have ticked up between LFS and CPI.

- Current OIS implied cumulative rate cuts, vs the current 2.75% policy rate: Sep (9bp), Oct (17bp), Dec (24bp), Jan (28bp).

- There is another inflation report before the BOC's Sep 17th rate announcement (Sep 16), but most of Governing Council's deliberations will be complete by then so it's not clear it would have much impact on the decision.

- That leaves attention on other data: the next release of note is Friday's retail sales, though that's likely to be overshadowed by Federal Reserve Chair Powell's speech later that morning.

- Most attention for the rest of the month will be on June/Q2 GDP data out on August 29, with the August Labour Force Survey out a week later.

USDCAD TECHS: Redirects Focus Higher

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3920 High May 21

- RES 1: 1.3879 High Aug 1 and a bull trigger

- PRICE: 1.3855 @ 16:34 BST Aug 19

- SUP 1: 1.3763/22 20-day EMA / Low Aug 22

- SUP 2: 1.3576 Low Jul 23

- SUP 3: 1.3557/40 Low Jul 3 / Low Jun 16 and the bear trigger

- SUP 4: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

A bear threat in USDCAD remains present, despite today’s recovery. A break of 1.3879, the Aug 1 high, would cancel a bear threat and resume the recent bull cycle. Downside focus is on support around the 20-day EMA, at 1.3763. A clear break of this EMA would resume the correction off the early August high. This would expose 1.3576, the Jul 23 low. Key medium-term support and the bear trigger lies at 1.3540, the Jun 16 low.

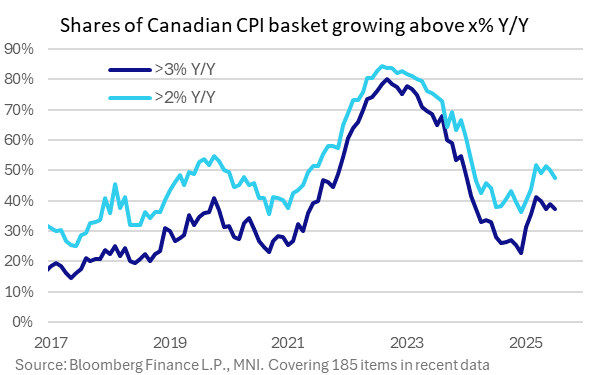

CANADA DATA: Inflation Breadth Narrows Slightly In July Report

MNI's estimates of inflationary "breadth" showed narrower price pressures in the July Canada CPI report.

- The percentage of CPI categories rising by more than 2% (looking at 185 CPI basket items) fell to 47.6% from 50.3% prior, for the narrowest since February.

- The % above 3% fell back to May's level, at 37.3%, from 38.9% prior. The proportion rising by more than 4% however remained unchanged at 30.3%.

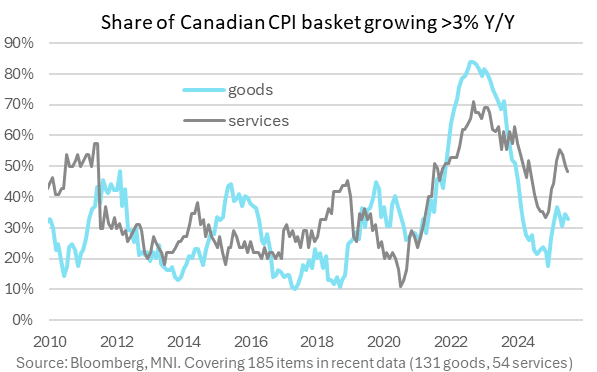

- Both goods and services breadth narrowed, with goods rising 2+% at 30.3% (31.4% prior, 3-month low) and services 17.3% (18.9% prior, 5-month low).

- Traditionally, the >3% breadth metric has been most closely tracked by the BOC in terms of gauging broad inflation pressures, and while this remains uncomfortably high it appears to be on the way down.