US TSYS: Post-Manufacturing PMI React

Jan-02 14:50

- Little reaction in Treasury futures after S&P Global Mfg PMI final data - in-line with expectations.

- Currently, TYH6 trades 112-11 (-3) vs. 112-05 low / 112-14.5 high.

- The trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection.

- Curves steeper: 2s10s at 69.368 +.382, 5s30s +1.534 at 113.196.

- Bloomberg US$ index holds mildly firmer: BBDXY +.42 at 1203.98

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Post-S&P Global Services/Composite PMI React

Dec-03 14:49

- Little reaction in Treasuries after modest decline in S&P Global Services/Composite PMI data.

- Near early morning highs, TYH6 trades 113-03.5 (+7) vs. 113-07 high, still south of initial technical resistance at 113-11/22+ High Dec 1 / High Nov 25.

- Curves mildly steeper: 2s10s +.155 at 57.596, 5s30s +1.570 at 110.437.

- Next up: SM Services data at 1000ET.

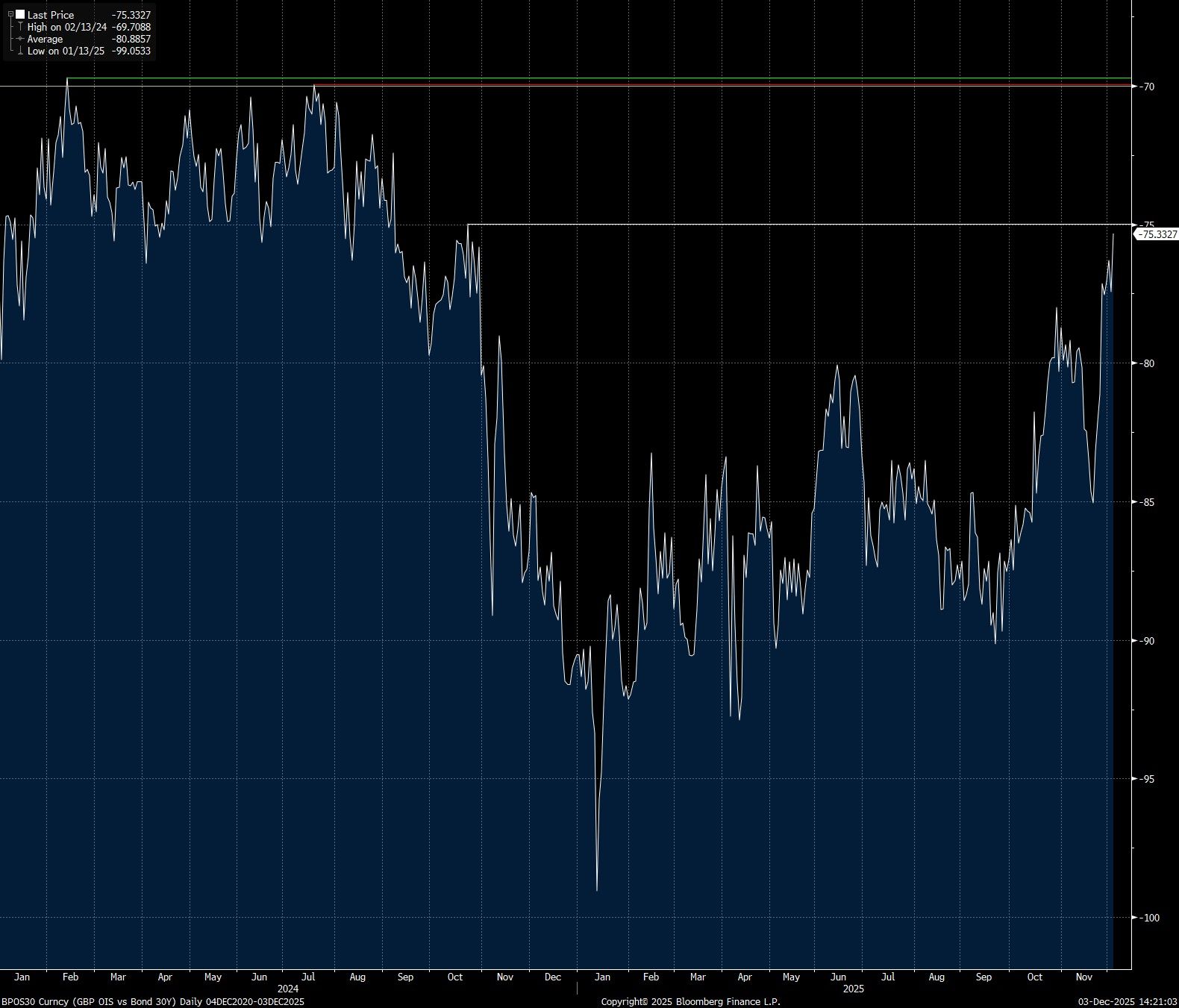

SWAPS: Long End Gilts Continue To Outperform Swaps

Dec-03 14:46

Long end UK swap spreads have widened further this week, even with 30-Year gilt yields little changed since the market close that followed the Budget.

- This points to a consistent post-Budget reduction in UK fiscal risk premium, with the 30-Year swap spread nearing the October ‘24 closing high (-74.99bp).

- While medium-term fiscal risks remain evident (with a particular focus on the backloaded nature of the fiscal tightening outlined in the Budget) the market has welcomed the (questionable) increase in fiscal headroom and ongoing WAM reduction in issuance, promoting swap spread widening.

- 30-Year swap spreads have rallied by ~10bp since the November 20 close, a break of the aforementioned October ’24 high would switch focus to the clustered resistance area at -70bp/-69.96bp and -69.71bp.

- It seems that a fresh gilt-negative catalyst is a pre-requisite for any fresh spread narrowing at this point e.g. slower-than-envisaged UK growth, political unrest or fresh questions surrounding the UK fiscal outlook.

Fig. 1: UK 30-Year Swap Spread (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

MNI: US NOV FINAL SERV PMI 54.1 (55.0 FLASH, 54.8 OCT)

Dec-03 14:45

- MNI: US NOV FINAL SERV PMI 54.1 (55.0 FLASH, 54.8 OCT)

- US NOV FINAL COMP PMI 54.2 (54.8 FLASH, 54.6 OCT)